RBS 2006 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2006 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

|

|

65

RBS Group • Annual Report and Accounts 2006

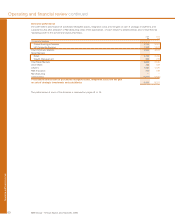

Operating and financial review

Retail Markets

Retail Markets was established in June 2005 to strengthen co-ordination and delivery of our multi-brand retail strategy across our

product range, and comprises Retail and Wealth Management.

2006 2005

£m £m

Net interest income 4,711 4,510

Non-interest income 3,926 3,746

Total income 8,637 8,256

Direct expenses

– staff costs 1,648 1,565

– other 793 829

2,441 2,394

Insurance net claims 488 486

Contribution before impairment losses 5,708 5,376

Impairment losses 1,344 1,185

Contribution 4,364 4,191

Allocation of Manufacturing costs 1,711 1,655

Operating profit 2,653 2,536

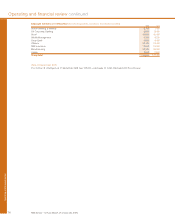

£bn £bn

Total banking assets 119.9 114.4

Loans and advances to customers – gross

– mortgages 69.8 64.6

– personal 21.0 21.5

– cards 9.1 9.6

– business 18.1 16.7

Customer deposits* 115.6 105.3

Investment management assets – excluding deposits 34.9 31.4

Risk-weighted assets 78.4 80.6

* customer deposits exclude bancassurance

Retail Markets achieved a good performance in 2006, with total

income rising by 5% to £8,637 million. Contribution before

impairment losses increased by 6% to £5,708 million,

contribution by 4% to £4,364 million and operating profit by 5%

to £2,653 million.

Responding to evolving demand from its customers, Retail

Markets has added to its capabilities in deposits and

investment products and has been rewarded by strong growth

in these areas. Lending growth has been centred on high

quality residential mortgages and small business loans, while

personal unsecured lending was flat, as we limited our activity

in the direct loans market and customer demand remained

subdued. We have used our full range of brands to address

markets flexibly, focusing on the most appropriate products

and channels in the light of prevailing market conditions.

Expenses have been kept under tight control, with additional

investment in our business offset by efficiency gains and the

benefits of combining Retail Banking and Direct Channels into

a unified business.

Customer recruitment has been centred on our branch

channels, where we have achieved good growth in savings

accounts and are joint market leader for personal current

accounts. Our commitment to customer service, through the

largest network of branches and ATMs in the UK, is reflected

in our industry-leading customer satisfaction ratings.

Average risk-weighted assets fell by 1%, reflecting a change in

business mix toward mortgage lending as well as careful

balance sheet management, including increased use of

securitisations.