RBS 2006 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2006 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

|

|

RBS Group • Annual Report and Accounts 2006

82

Operating and financial review continued

Operating and financial review

Credit risk models

Credit risk models are used throughout the Group to support

the analytical elements of the credit risk management

framework, in particular the quantitative risk assessment part

of the credit approval process, ongoing credit monitoring as

well as portfolio level analysis and reporting.

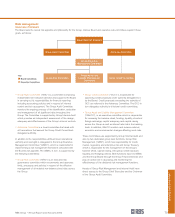

Credit risk modelling governance

The Group’s ‘Principles for Managing Credit Risk’ outline the

governance structure under which all credit risk models must

be developed, reviewed and approved. GRM is responsible for:

•Establishing high level standards to which all credit risk

models across the Group must adhere and thus ensuring a

consistency of approach to credit risk modelling across the

Group.

•Approving all credit risk models prior to implementation and

reviewing existing models on at least an annual basis.

Divisional credit risk departments own the particular models

and are responsible for:

•Developing credit risk models appropriate for the types of

borrower and facilities in their credit portfolios and obtaining

approval from GRM for their implementation.

•Validating the models and submitting documentation of

these validations to GRM with appropriate recommendations

on recalibration, where applicable.

•Obtaining approval from GRM for any new methodology or

parameter estimates used in existing credit risk models prior

to implementation.

Credit risk models used by the Group can be broadly grouped

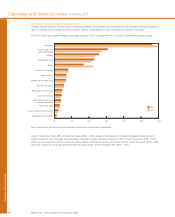

into four categories.

•Probability of default (“PD”)/customer credit grade – these

models assess the probability that the customer will fail to

make full and timely repayment of credit obligations over a

one year time horizon. Each customer is assigned an

internal credit grade which corresponds to probability of

default. There are a number of different credit grading

models in use across the Group, each of which considers

particular customer characteristics in that portfolio. The

credit grading models use a combination of quantitative

inputs, such as recent financial performance and customer

behaviour, and qualitative inputs, such as company

management performance or sector outlook.

Every customer credit grade across all grading scales in

the Group can be mapped to a Group level credit grade

(see page 83).

•Exposure at default (“EAD”) – these models estimate the

expected level of utilisation of a credit facility at the time of

a borrower’s default. The EAD will typically be higher than

the current utilisation (e.g. in the case where further

drawings are made on a revolving credit facility prior to

default) but will not typically exceed the total facility limit.

The methodologies used in EAD modelling recognise that

customers may make more use of their existing credit

facilities in the run up to a default.

•Loss given default (“LGD”) – these models estimate the

economic loss that may be suffered by the Group on a credit

facility in the event of default. The LGD of a facility represents

the amount of debt which cannot be recovered and is

typically expressed as a percentage of the EAD. The Group’s

LGD models take into account the type of borrower, facility

and any risk mitigation such as security or collateral held.

The LGD may also be affected by the industry sector of the

borrower, the legal jurisdiction in which the borrower operates

as well as general economic conditions which may impact the

value of any assets held as security.

•Credit risk exposure measurement – these models calculate

the credit risk exposure for products where the exposure is

not 100% of the gross nominal amount of the credit

obligation. These models are most commonly used for

derivative and other traded instruments where the amount of

credit risk exposure may be dependent on external variables

such as interest rates or foreign exchange rates.

Credit risk stress testing

Credit risk stress testing measures the potential vulnerability to

exceptional but plausible economic and geopolitical events,

and seeks to quantify the impact of an adverse change in

factors which drive the performance and profitability of a

portfolio. Stress testing is used within the Group’s CRMF to

estimate and manage potential loss in the portfolio and to

support the Board’s internal assessment of adequacy of

regulatory capital.

At the Group level, a series of stress events are monitored on a

regular basis to assess the potential impact on the Group’s

income statement, through the credit impairment charge. The

primary objective of this analysis is to support the Group’s

framework for managing industry and geographical sector

concentrations. This is done through the identification of

scenarios which are likely to affect groups of inter-related

sectors. These stress tests are discussed with senior divisional

management and are reported to GRC, GEMC and the GAC.

The Group manages to a trigger limit on the stressed

impairment charge for an individual scenario.

In addition, the Group calculates the potential impact of a

range of macroeconomic scenarios on both the Group’s

income statement and balance sheet. This analysis is

discussed by GEMC and reported to the Board.