RBS 2006 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2006 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

|

|

71

RBS Group • Annual Report and Accounts 2006

Operating and financial review

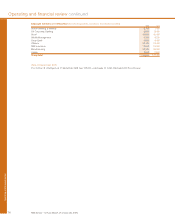

RBS Insurance

2006 2005

£m £m

Earned premiums 5,713 5,641

Reinsurers’ share (212) (246)

Insurance premium income 5,501 5,395

Net fees and commissions (486) (449)

Other income 664 543

Total income 5,679 5,489

Direct expenses

– staff costs 319 316

– other 426 411

745 727

Gross claims 4,030 3,903

Reinsurers’ share (60) (76)

Net claims 3,970 3,827

Contribution 964 935

Allocation of Manufacturing costs 214 207

Operating profit 750 728

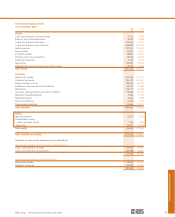

2006 2005

In-force policies (000’s)

– Core motor: UK 7,490 7,439

– Core motor: Continental Europe 2,114 1,862

– Core non-motor (including home, rescue, SMEs, pet, HR24): UK 4,920 4,799

– Partnerships (including motor, home, rescue, SMEs, pet, HR24) 7,267 7,559

General insurance reserves – total (£m) 8,068 7,776

RBS Insurance increased total income by 3% to £5,679 million,

with contribution also rising by 3% to £964 million and

operating profit by the same percentage to £750 million.

We achieved good overall policy growth of 3% in our core

businesses including excellent progress in our European

businesses. Our joint venture in Spain grew policy numbers by

14% to 1.34 million.

In the UK we have grown our core motor book by 1% whilst

focusing on more profitable customers acquired through our

direct brands, with good results achieved through the internet

channel, which accounted for half of all new own-brand motor

policies last year.

We implemented price rises in motor insurance in the second

half of the year, and average motor premium rates across the

market increased in the fourth quarter. Higher premium rates

will, however, take time to feed through into income, and

competition on prices remains strong.

Our core non-motor personal lines policies grew by 3%, with

particularly good progress in Tesco Personal Finance. SME

has also performed well with policies sold through our

intermediary business growing by 10%.

However, some of our partnership books continue to age and

we did not renew a number of other partnerships. As a result,

the number of partnership policies in force fell by 8% in motor

and by 9% in home.

Insurance premium income was up 2% to £5,501 million,

reflecting a modest overall increase in the total number of

in-force policies.

Net fees and commissions payable increased by 8% to

£486 million, whilst other income rose by 22% to £664 million,

reflecting increased investment income.

Total expenses rose by 3% to £959 million. Good cost

discipline held direct expenses to £745 million, up 2%. Staff

costs rose by 1%, reflecting improved efficiency despite

continued investment in service standards. A 4% rise in non-

staff costs included increased marketing expenditure to

support growth in continental Europe.

Net claims rose by 4% to £3,970 million. The environment for

home claims remained benign, whilst underlying increases in

average motor claims costs were partially offset by purchasing

efficiencies and improvements in risk management.

The UK combined operating ratio for 2006, including

Manufacturing costs, was 94.6%, compared with 93.4% in

2005, reflecting a higher loss ratio and the discontinuation

of some partnerships.