RBS 2006 Annual Report Download - page 161

Download and view the complete annual report

Please find page 161 of the 2006 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

|

|

RBS Group • Annual Report and Accounts 2006

160

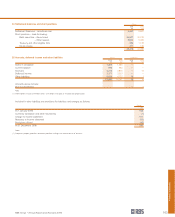

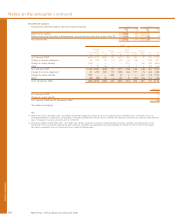

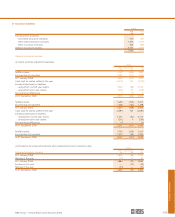

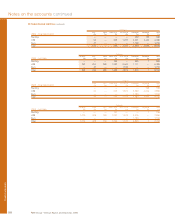

Notes on the accounts continued

Financial statements

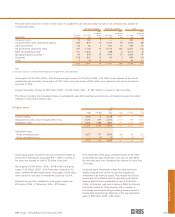

Companies in the Group enter into derivatives as principal

either as a trading activity or to manage balance sheet foreign

exchange, interest rate and credit risk. Derivatives include

swaps, forwards, futures and options. They may be traded on

an organised exchange (exchange-traded) or over-the-counter

(OTC). Holders of exchange traded derivatives are generally

required to provide margin daily in the form of cash or other

collateral.

Swaps include currency swaps, interest rate swaps, credit

default swaps, total return swaps and equity and equity index

swaps. A swap is an agreement to exchange cash flows in the

future in accordance with a pre-arranged formula. In currency

swap transactions, interest payment obligations are exchanged

on assets and liabilities denominated in different currencies;

the exchange of principal may be notional or actual. Interest

rate swap contracts generally involve exchange of fixed and

floating interest payment obligations without the exchange of

the underlying principal amounts.

Forwards include forward foreign exchange contracts and

forward rate agreements. A forward contract is a contract to

buy (or sell) a specified amount of a physical or financial

commodity, at an agreed price, on an agreed future date.

Forward foreign exchange contracts are contracts for the

delayed delivery of currency on a specified future date.

Forward rate agreements are contracts under which two

counterparties agree on the interest to be paid on a notional

deposit of a specified maturity at a specific future date; there

is no exchange of principal.

Futures are exchange-traded forward contracts to buy (or sell)

standardised amounts of underlying physical or financial

commodities. The Group buys and sells currency, interest rate

and equity futures.

Options include exchange-traded options on currencies,

interest rates and equities and equity indices and OTC

currency and equity options, interest rate caps and floors and

swaptions. They are contracts that give the holder the right but

not the obligation to buy (or sell) a specified amount of the

underlying physical or financial commodity at an agreed price

on an agreed date or over an agreed period.

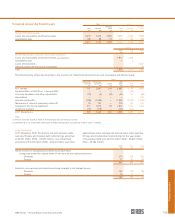

The Group enters into fair value and cash flow hedges and

hedges of net investments in foreign operations. Fair value

hedges principally involve interest rate swaps hedging the

interest rate risk in recognised financial assets and financial

liabilities. Similarly, the majority of the Group’s cash flow hedges

relate to exposure to variability in future interest payments and

receipts on forecast transactions and on recognised financial

assets and financial liabilities and hedged by interest rate swaps

for periods of up to 26 years. The Group hedges its net

investments in foreign operations with currency borrowings.

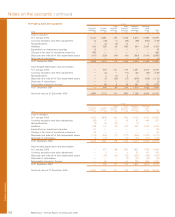

For cash flow hedge relationships of interest rate risk the hedged

items are actual and forecast variable interest rate cash flows

arising from financial assets and financial liabilities with interest

rates linked to LIBOR or the Bank of England Official Bank

Rate. The financial assets are customer loans and the financial

liabilities are customer deposits and LIBOR linked medium-

term notes and other issued securities.

For cash flow hedging relationships, the initial and ongoing

prospective effectiveness is assessed by comparing movements

in the fair value of the expected highly probable forecast

interest cash flows with movements in the fair value of the

expected changes in cash flows from the hedging interest rate

swap. Prospective effectiveness is measured on a cumulative

basis i.e. over the entire life of the hedge relationship. The

method of calculating hedge ineffectiveness is the hypothetical

derivative method. Retrospective effectiveness is assessed by

comparing the actual movements in the fair value of the cash

flows and actual movements in the fair value of the hedged

cash flows from the interest rate swap over the life to date of

the hedging relationship.

For fair value hedge relationships of interest rate risk the

hedged items are typically large corporate fixed-rate loans,

fixed-rate finance leases, fixed-rate medium-term notes or

preference shares classified as debt. The initial and ongoing

prospective effectiveness of fair value hedge relationships is

assessed on a cumulative basis by comparing movements in

the fair value of the hedged item attributable to the hedged

risk with changes in the fair value of the hedging interest rate

swap. Retrospective effectiveness is assessed by comparing

the actual movements in the fair value of the hedged items

attributable to the hedged risk with actual movements in the

fair value of the hedging derivative over the life to date of the

hedging relationship.

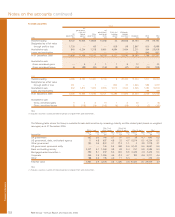

19 Derivatives