RBS 2006 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2006 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

|

|

RBS Group • Annual Report and Accounts 2006

70

Operating and financial review continued

Operating and financial review

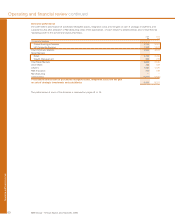

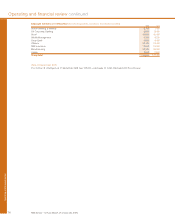

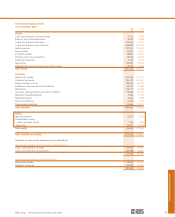

Citizens

2006 2005

£m £m

Net interest income 2,085 2,122

Non-interest income 1,232 1,142

Total income 3,317 3,264

Direct expenses

– staff costs 803 819

– other 751 739

1,554 1,558

Contribution before impairment losses 1,763 1,706

Impairment losses 181 131

Operating profit 1,582 1,575

US$bn US$bn

Total assets 162.2 158.8

Loans and advances to customers – gross

– mortgages 18.6 18.8

– home equity 34.5 31.8

– other consumer 23.2 24.8

– corporate and commercial 32.7 29.2

Customer deposits 106.8 106.3

Risk-weighted assets 113.1 106.4

Average exchange rate – US$/£ 1.844 1.820

Spot exchange rate – US$/£ 1.965 1.721

Citizens grew its total income by 3% to $6,115 million and its

operating profit by 2% to $2,917 million. In sterling terms,

Citizens total income increased by 2% to £3,317 million, while

its operating profit rose slightly to £1,582 million.

We have achieved good growth in lending volumes, with

average loans and advances to customers increasing by 10%.

In business lending, average loans excluding finance leases

increased by 15%, reflecting Citizens’ success in adding new

mid-corporate customers and increasing its total number of

business customers by 4% to 467,000. In personal lending,

Citizens increased average mortgage and home equity lending

by 14%, though the mortgage market slowed in the second

half. Average credit card receivables, while still relatively small,

increased by 19%.

We increased average customer deposits by 4%, although

spot balances at the end of 2006 were little changed from the

end of 2005. As interest rates rose further and the US yield

curve inverted, we saw migration from low-cost checking and

liquid savings to higher-cost term and time deposits. This

migration is a principal reason for the decline in Citizens’ net

interest margin to 2.72% in 2006, compared with 3.00% in

2005. The decline slowed over the course of the year, with net

interest margin in the second half 6 basis points lower than in

the first. Lower net interest margins more than offset the

benefit of higher average loans and deposits, leaving net

interest income marginally lower at $3,844 million.

Non-interest income rose by 9% to $2,271 million. Business

and corporate fees rose strongly, with good results especially

in foreign exchange, interest rate derivatives and cash

management benefiting from increased activity with Corporate

Markets. There was good progress in debit cards, where

issuance has been boosted by the launch in September of our

"Everyday Rewards" programme. Citizens has also become

the US’s leading issuer of Paypass™ contactless debit cards,

with 3.65 million cards issued. Our credit card customers

increased by 20%, whilst RBS Lynk, our merchant acquiring

business, also achieved significant growth, processing 40%

more transactions than it did in 2005 and expanding its

merchant base by 11%.

Tight cost control and a 5% reduction in headcount limited the

increase in total expenses to only 1%, despite continued

investment in growth opportunities such as mid-corporate

banking, contactless debit cards, merchant acquiring and

supermarket banking.

Citizens continued to expand its branch network. Our

partnership with Stop & Shop Supermarkets has helped us to

expand our supermarket banking franchise into New York,

while in October we announced the purchase of GreatBanc,

Inc., strengthening our position in the Chicago market and

making us the 4th largest bank in the Chicago area, based on

deposits. The acquisition was completed in February 2007.

Impairment losses totalled $333 million, representing just

0.31% of loans and advances to customers and illustrating the

prime quality of our portfolio. Underlying strong credit quality

remained unchanged as our portfolio grew, with risk elements

in lending and problem loans representing 0.32% of loans and

advances, the same level as in 2005. Our consumer lending is

to prime customers with average FICO scores on our portfolios,

including home equity lines of credit, in excess of 700, and

95% of lending is secured.