RBS 2006 Annual Report Download - page 218

Download and view the complete annual report

Please find page 218 of the 2006 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

|

|

RBS Group • Annual Report and Accounts 2006 217

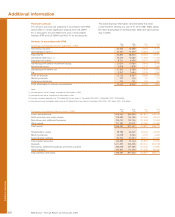

Financial statements

US GAAP

US GAAP requires the same treatment of purchased goodwill.

This was adopted by the Group from 1 July 2001. Prior to this

goodwill was recognised as an asset and amortised over

periods of up to 25 years. No amortisation was written back on

this change of policy.

For US GAAP purposes the Group recognised intangible

assets separately from goodwill from 1 July 2001. This has

resulted in the recognition of additional intangible assets and

consequently a higher amortisation charge under US GAAP.

(2) Implementation timing differences

This section sets out those adjustments that, although the applicable IFRS and US GAAP standards are substantially the same, arise

because their effective dates for the Group differ.

IFRS

Intangible assets

Purchased goodwill

Purchased goodwill is recorded at cost less any accumulated

impairment losses. Goodwill is tested annually (at 30 September)

for impairment or more frequently if events or changes in

circumstances indicate that it might be impaired.

Goodwill arising on acquisitions after 1 October 1998 was

capitalised and amortised over its estimated useful economic

life. Goodwill arising on acquisitions before 1 October 1998

was deducted from equity. The carrying amount of goodwill in

the Group's opening IFRS balance sheet was its carrying value

under UK GAAP as at 31 December 2003.

There was no restatement of previous acquisitions in 1998.

In 2004 no amortisation was written back.

Other intangibles

Until 2004 intangible assets acquired in a business

combination were recognised separately from goodwill only if

they were separable and reliably measurable. From 1 January

2004 intangible assets are recognised if they are separable or

arise from contractual or other legal rights. All intangible assets

are amortised over their useful economic lives.

(3) For 2004

As permitted by IFRS 1, in the preparation of the Group’s 2004 consolidated income statements and balance sheets, all IFRS have

been applied except those relating to financial instruments and insurance contracts where UK GAAP principles then current have

been applied.

IFRS or relevant UK GAAP

(a) Acquisition accounting

All integration costs relating to acquisitions are expensed as

post-acquisition expenses.

US GAAP

Certain restructuring and exit costs incurred in the acquired

business are treated as liabilities assumed on acquisition and

taken into account in the calculation of goodwill.

Other adjustments in the reconciliation of net income from IFRS to US GAAP for the year ended 31 December 2005 include refinements

to estimates arising from the implementation of IFRS.