RBS 2006 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2006 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

|

|

RBS Group • Annual Report and Accounts 2006

94

Operating and financial review continued

Operating and financial review

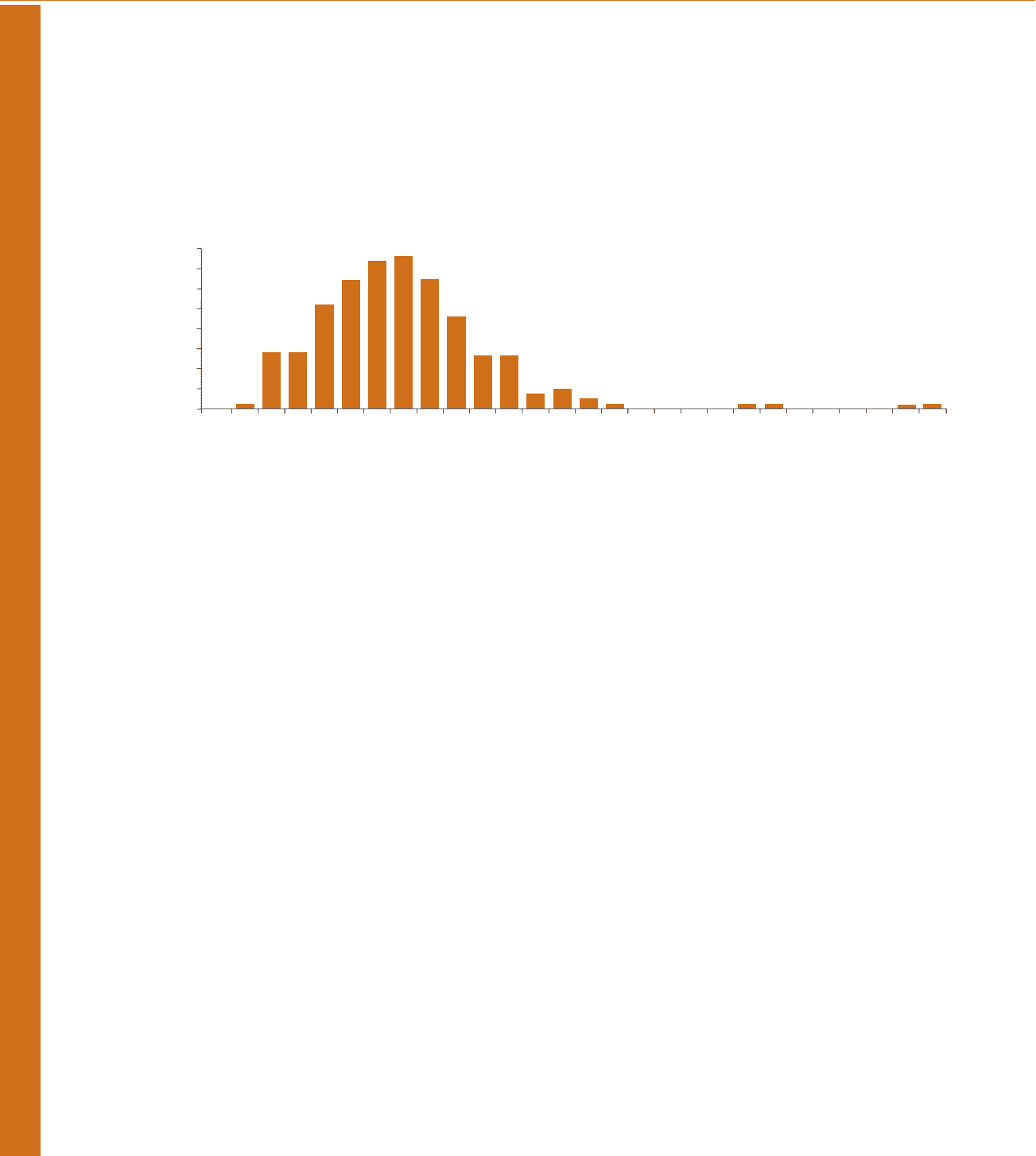

(ii) Stress testing

Stress testing measures the impact of abnormal changes in

market rates and prices on the fair value of the Group’s trading

portfolios. GEMC approves the high-level market risk stress test

limit for the Group.

The Group calculates a range of market risk stress tests each

day. The objective of stress testing is to identify the loss that

the Group’s current portfolio of trading book exposures would

generate in plausible but adverse market events. The Group

calculates historical stress tests and hypothetical stress tests.

Historical stress tests calculate the loss that would be

generated if the market movements that occurred during a

historical market event were to be repeated. Hypothetical

stress tests calculate the loss that would be generated if a

specific set of adverse market movements were to occur.

In addition to the Group-level consolidated market risk stress

tests, stress testing is also undertaken at key trading strategy

level. Additional stress tests are undertaken for those strategies

where the associated market risks are not adequately captured

by VaR.

Stress test exposures are discussed with senior management

and are reported to GRC, GEMC and the Board. Breaches in

the Group’s market risk stress testing limit are reported to GEMC.

(iii) Position risk and sensitivity analyses

In addition to the VaR and stress testing measures discussed

above, the Group calculates a wide range of sensitivity and

position risk measures, for example interest rate ladders or

option revaluation matrices. These measures provide valuable

additional controls, often at individual desk or strategy level.

0

5

10

15

20

25

30

35

40

< (4)

(4) > <(2)

(2) > <0

0 > <2

2 > <4

4 > <6

6 > < 8

8 > < 10

10 > < 12

12 > < 14

14 > < 16

16 > < 18

18 > < 20

20 > < 22

22 > < 24

24 > < 26

26 > < 28

28 > < 30

30 > < 32

32 > < 34

34 > < 36

36 > < 38

38 > < 40

40 > < 42

42 > < 44

44 > < 46

46 > < 48

> 48

Number of trading days

Trading income (£m)

Backtesting

The Group undertakes a programme of daily backtesting,

which compares the actual profit or loss realised in trading

activity to the VaR estimation. The results of the backtesting

process are one of the methods by which the Group monitors

the ongoing suitability of its VaR model. Backtesting

exceptions are those instances when a realised loss exceeds

the predicted VaR. At the 99% confidence level, no more than

one backtesting exception is expected every 100 trading

days. The Group experienced no backtesting exceptions

at legal entity level during 2006.

The Group’s trading activities are carried out principally by Global Banking & Markets. The chart below depicts the number of days

on which Global Banking & Markets’ trading income fell within stated ranges.