RBS 2006 Annual Report Download - page 259

Download and view the complete annual report

Please find page 259 of the 2006 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262

|

|

RBS Group • Annual Report and Accounts 2006

258

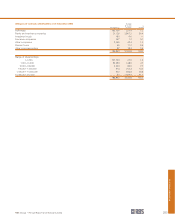

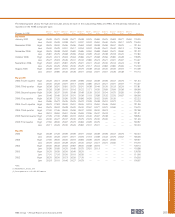

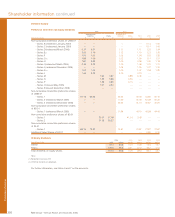

Shareholder information continued

Shareholder information

Taxation for US Holders (continued)

A non-cumulative dollar preference share or ADS beneficially

owned by an individual, whose domicile is determined to be

the United States for purposes of the Estate Tax Treaty and

who is not a national of the UK, will not be subject to UK

inheritance tax on the individual’s death or on a lifetime transfer

of the non-cumulative dollar preference share or ADS, except

in certain cases where the non-cumulative dollar preference

share or ADS (i) is comprised in a settlement (unless, at the

time of the settlement, the settlor was domiciled in the United

States and was not a national of the UK); (ii) is part of the

business property of a UK permanent establishment of an

enterprise; or (iii) pertains to a UK fixed base of an individual

used for the performance of independent personal services.

The Estate Tax Treaty generally provides a credit against US

federal estate or gift tax liability for the amount of any tax paid

in the UK in a case where the non-cumulative dollar preference

share or ADS is subject to both UK inheritance tax and US

federal estate or gift tax.

UK stamp duty and stamp duty reserve tax (“SDRT”)

The following is a summary of the UK stamp duty and SDRT

consequences of transferring an ADS or ADR in registered

form (otherwise than to the custodian on cancellation of the

ADS) or of transferring a non-cumulative dollar preference

share. A transfer of a registered ADS or ADR executed and

retained in the United States will not give rise to stamp duty and

an agreement to transfer a registered ADS or ADR will not give

rise to SDRT. Stamp duty or SDRT will normally be payable on

or in respect of transfers of non-cumulative dollar preference

shares and accordingly any holder who acquires or intends to

acquire non-cumulative dollar preference shares is advised to

consult its own tax advisers in relation to stamp duty and SDRT.

PROs

United States

Payments of interest on a PRO (including any UK withholding

tax, as to which see below) will constitute foreign source

dividend income for US federal income tax purposes to the

extent paid out of the current or accumulated earnings and

profits of the company, as determined for US federal income

tax purposes. Payments will not be eligible for the dividends-

received deduction allowed to corporate US Holders. A US

Holder who is entitled under the Treaty to a refund of UK tax,

if any, withheld on a payment will not be entitled to claim a

foreign tax credit with respect to such tax.

Subject to applicable limitations that may vary depending upon

a holder’s individual circumstances, dividends paid to certain

non-corporate US Holders in taxable years beginning before 1

January 2011 will be taxable at a maximum tax rate of 15%.

Non-corporate US Holders should consult their own tax

advisers to determine whether they are subject to any special

rules that limit their ability to be taxed at this favourable rate.

A US Holder will, upon the sale, exchange or redemption of a

PRO, generally recognise capital gain or loss for US federal

income tax purposes (assuming that in the case of a

redemption, such US Holder does not own, and is not deemed

to own, any ordinary shares of the company) in an amount

equal to the difference between the amount realised (excluding

any amount in respect of mandatory interest and any missed

payments which are to be satisfied on a missed payment

satisfaction date, which would be treated as ordinary income)

and the US Holder’s tax basis in the PRO.

A US Holder who is liable for both UK and US tax on gain

recognised on the disposal of PROs will generally be entitled,

subject to certain limitations, to credit the UK tax against its US

federal income tax liability in respect of such gain.

United Kingdom

Taxation of payments on the PROs

Payments on the PROs will constitute interest rather than

dividends for UK withholding tax purposes. However, the PROs

will constitute ‘quoted eurobonds’ within the meaning of section

349 of the Income and Corporation Taxes Act 1988 and therefore

payments of interest will not be subject to withholding or

deduction for or on account of UK taxation as long as the PROs

remain at all times listed on a ‘recognised stock exchange’ within

the meaning of section 841 of the Income and Corporation Taxes

Act 1988. In all other cases, an amount must be withheld on

account of UK income tax at the lower rate (currently 20%)

subject to any direction to the contrary by HM Revenue &

Customs under the Treaty and except that the withholding

obligation is disapplied in respect of payments to persons who

the company reasonably believes are within the charge to

corporation tax or fall within various categories enjoying a special

tax status (including charities and pension funds), or are

partnerships consisting of such persons (unless HM Revenue &

Customs directs otherwise). Where interest has been paid under

deduction of UK withholding tax, US Holders may be able to

recover the tax deducted under the Treaty.

Any paying agent or other person by or through whom interest

is paid to, or by whom interest is received on behalf of, an

individual, may be required to provide information in relation to

the payment and the individual concerned to HM Revenue &

Customs. HM Revenue & Customs may communicate this

information to the tax authorities of other jurisdictions.

HM Revenue & Customs confirmed at around the time of the

issue of the PROs that interest payments would not be treated

as distributions for UK tax purposes by reason of (i) the fact

that interest may be deferred under the terms of issue; or

(ii) the undated nature of the PROs, provided that at the time

an interest payment is made, the PROs are not held by a

company which is ‘associated’ with the company or by a

‘funded company’. A company will be associated with the

company if, broadly speaking, it is part of the same group as

the company. A company will be a ‘funded company’ for these

purposes if there are arrangements involving that company

being put in funds (directly or indirectly) by the company, or an

entity associated with the company. In this respect, HM

Revenue & Customs has confirmed that a company holding an

interest in the PROs which incidentally has banking facilities

with any company associated with the company will not be a

‘funded company’ by virtue of such facilities.