RBS 2006 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2006 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

|

|

81

RBS Group • Annual Report and Accounts 2006

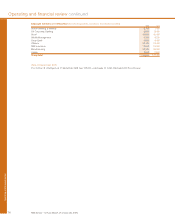

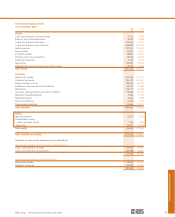

Operating and financial review

Credit risk

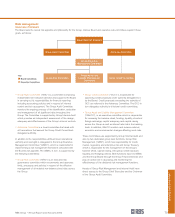

Key principles of credit risk management

The objective of credit risk management is to enable the Group

to achieve appropriate risk versus reward performance whilst

maintaining credit risk exposure in line with approved risk

appetite.

Group Risk Management is responsible for setting standards

for credit risk management throughout the Group. This is

achieved via a combination of governance structures, credit

risk policies, control processes and credit systems collectively

known as the Group’s Credit Risk Management Framework

(“CRMF”). The framework is defined in detail in the Group’s

‘Principles for Managing Credit Risk’.

The key principles for credit risk management as defined in the

CRMF are set out below.

•Approval of all credit exposure is granted prior to any

advance or extension of credit.

•An appropriate credit risk assessment of the customer and

credit facilities is undertaken prior to approval of credit

exposure. This includes a review of, amongst other things,

the purpose of the credit and sources of repayment,

compliance with affordability tests, repayment history,

capacity to repay, sensitivity to economic and market

developments and risk-adjusted return.

•The Board delegates authority to Advances Committee,

Group Credit Committee and divisional credit committees.

•Credit risk authority is specifically granted in writing to all

individuals involved in the granting of credit approval,

whether this is exercised personally or collectively as part of

a credit committee. In exercising credit authority, the

individuals act independently.

•Where credit authority is exercised personally, the individual

has no responsibility or accountability for related business

revenue generation.

•All credit exposures, once approved, are effectively

monitored and managed and reviewed periodically against

approved limits. Lower quality exposures are subject to a

greater frequency of analysis and assessment.

•Customers with emerging credit problems are identified early

and classified accordingly. Remedial actions are implemented

promptly to minimise the potential loss to the Group.

•Portfolio analysis and reporting is used to identify and manage

credit risk concentrations and credit risk quality migration.

Each Division has established its own CRMF consistent with

the Group CRMF. Divisional credit departments are responsible

for maintaining the CRMF and ensuring that asset quality is

within specified parameters. Divisional credit departments are

independent of business management and have no direct

responsibility or accountability for revenue generation. This

independence is supported by the divisional head of credit

having dual reporting lines to both the divisional CEO (via the

divisional Chief Risk Officer) and to the Head of Group Credit

Risk.

GRM undertakes regular assessments of the effectiveness

of each divisional CRMF to ensure it complies with Group

standards and is appropriate for the business being

undertaken. GRC and the GEMC review reports on the Group’s

portfolio of credit risks on a monthly basis.

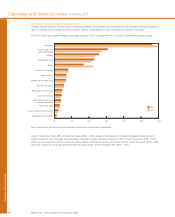

Credit approval process

Different credit approval processes exist for each customer

type in order to ensure appropriate skills and resources are

employed in credit assessment and approval whilst following

the key principles relating to credit approval.

Wholesale risk exposures are aggregated to determine the

appropriate level of credit approval required and to facilitate

consolidated credit risk management.

Credit authority is not extended to relationship managers:

•Assessments of corporate borrower and transaction risk are

undertaken using a range of credit risk models supplemented,

where appropriate, by management judgement. Specialist

internal credit risk departments independently oversee the

credit process and make credit decisions or

recommendations to the appropriate credit committee.

•Financial Markets counterparties are subject to similar

modelling techniques but are approved by a dedicated credit

function which specialises in traded market product risk.

Consumer lending and personal businesses employ best

practice credit scoring techniques to process small scale,

large volume credit decisions. Scores from such systems are

combined with management judgement to ensure an effective

ongoing process of approval, review and enhancement. Credit

decisions for loans above specified thresholds are individually

assessed.