BB&T 2015 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2015 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

|

|

TableofContents

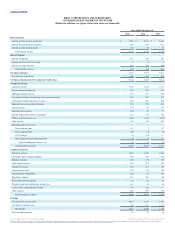

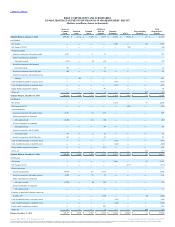

LHFS

BB&T accounts for new originations of prime residential and commercial mortgage LHFS at fair value. BB&T accounts for the derivatives used to

economically hedge the LHFS at fair value. The fair value of LHFS is primarily based on quoted market prices for securities collateralized by similar types of

loans. Direct loan origination fees and costs related to LHFS are not capitalized and are recorded as mortgage banking income in the case of the direct loan

origination fees and primarily personnel expense in the case of the direct loan origination costs. Gains and losses on sales of mortgage loans are included in

mortgage banking income. Gains and losses on sales of commercial LHFS are included in other noninterest income.

BB&T sells a significant portion of its fixed-rate commercial and conforming residential mortgage loan originations, which are typically converted into MBS

by FHLMC, FNMA and GNMA and subsequently sold to other third party investors. BB&T records these transactions as a sale when the transferred loans are

legally isolated from BB&T’s creditors and the other accounting criteria for a sale are met. Gains or losses recorded on these transactions are based in part on

the net carrying amount of the loans sold, which is allocated between the loans sold and retained interests based on their relative fair values at the date of

sale. BB&T generally retains the mortgage servicing on loans sold. Since quoted market prices are not typically available, BB&T estimates the fair value of

these retained interests using modeling techniques to determine the net present value of expected future cash flows. Such models incorporate management’s

best estimates of key variables, such as prepayment speeds, servicing costs and discount rates, that would be used by market participants based on the risks

involved.

Gains on residential mortgage loan sales, including marking LHFS to fair value and the impact of interest rate lock commitments, are recorded in noninterest

income as a component of mortgage banking income. For certain of these transactions, the loan servicing rights were retained, including the related MSRs

and on-going servicing fees.

BB&T also issues standard representations and warranties related to mortgage loan sales to GSEs. Although these agreements often do not specify limitations,

management does not believe that any payments related to these warranties would materially change the financial condition or results of operations of

BB&T.

Loans and Leases

The Company’s accounting methods for loans differ depending on whether the loans are originated or purchased, and if purchased, whether or not the loans

reflect credit deterioration since the date of origination such that it is probable at the date of acquisition that BB&T will be unable to collect all contractually

required payments.

Originated Loans and Leases

Loans and leases that management has the intent and ability to hold for the foreseeable future are reported at their outstanding principal balances net of any

unearned income, charge-offs, and unamortized fees and costs. The net amount of nonrefundable loan origination fees and certain direct costs associated with

the lending process are deferred and amortized to interest income over the contractual lives of the loans using methods that approximate the interest method.

BB&T classifies loans and leases as past due when the payment of principal and interest based upon contractual terms is greater than 30 days delinquent or if

one payment is past due. When commercial loans are placed on nonaccrual status as described below, a charge-off is recorded, as applicable, to decrease the

carrying value of such loans to the estimated recoverable amount. Retail loans are subject to mandatory charge-off at a specified delinquency date consistent

with regulatory guidelines. As such, retail loans are subject to collateral valuation and charge-off, as applicable, when they are moved to nonaccrual status as

described below.

Purchased Loans

Purchased loans are recorded at their fair value at the acquisition date. Credit discounts are included in the determination of fair value; therefore, an ALLL is

not recorded at the acquisition date.

89

Source: BB&T CORP, 10-K, February 25, 2016 Powered by Morningstar® Document Research℠

The information contained herein may not be copied, adapted or distributed and is not warranted to be accurate, complete or timely. The user assumes all risks for any damages or losses arising from any use of this information,

except to the extent such damages or losses cannot be limited or excluded by applicable law. Past financial performance is no guarantee of future results.