BB&T 2015 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2015 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

|

|

TableofContents

·systems conversion and related charges, which represent costs to integrate the acquired entity’s information technology systems; and

·other merger-related and restructuring charges or credits, which include expenses necessary to convert and combine the acquired branches and

operations of merged companies, direct media advertising related to the acquisitions, asset and supply inventory write-offs, and other similar

charges.

Merger-related and restructuring accruals are established when the costs are incurred or once all requirements for a plan to dispose of certain business

functions have been approved by management. In general, a major portion of accrued costs are utilized in conjunction with or immediately following the

systems conversion, when most of the duplicate positions are eliminated and the terminated employees begin to receive severance. Other accruals are utilized

over time based on the sale, closing or disposal of duplicate facilities or equipment or the expiration of lease contracts. Merger and restructuring accruals are

re-evaluated periodically and adjusted as necessary. The remaining accruals at December 31, 2015 are generally expected to be utilized within one year,

unless they relate to specific contracts that expire later.

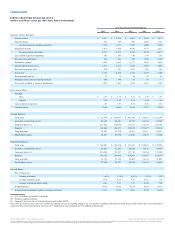

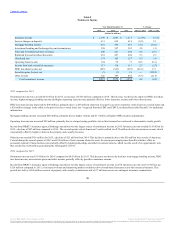

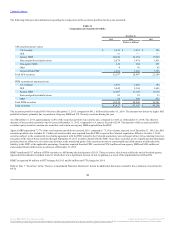

The following table presents a summary of activity with respect to merger-related and restructuring accruals:

Severance and personnel-related $ 2 $ 60 $ (36) $ 26

Occupancy and equipment 7 16 (12) 11

Professional services 17 34 (38) 13

Systems conversion and related charges ― 25 (25) ―

Other adjustments 5 30 (33) 2

Total $ 31 $ 165 $ (144) $ 52

Provision for Income Taxes

BB&T’s provision for income taxes totaled $794 million, $921 million and $1.6 billion for 2015, 2014 and 2013, respectively. BB&T’s effective tax rates for

the years ended 2015, 2014 and 2013 were 27.2%, 29.5% and 47.3%, respectively. The changes in the effective tax rates during 2015, 2014 and 2013 were

primarily due to adjustments for uncertain tax positions as discussed below.

During 2010, BB&T received an IRS statutory notice of deficiency for tax years 2002-2007 asserting a liability for taxes, penalties and interest of

approximately $892 million related to the disallowance of foreign tax credits and other deductions claimed by a subsidiary in connection with a financing

transaction. BB&T paid the disputed tax, penalties and interest during 2010 and filed a lawsuit seeking a refund in the U.S. Court of Federal Claims. During

2013, the court denied the refund claim, and BB&T recorded $516 million of income tax charges. BB&T appealed the decision to the U.S. Court of Appeals

for the Federal Circuit. On May 14, 2015, the appeals court overturned a portion of the earlier ruling, resulting in the recognition of income tax benefits of

$107 million during the second quarter of 2015. The remainder of the decision was affirmed. On September 29, 2015, BB&T filed a petition requesting the

case be heard by the U.S. Supreme Court, which has not rendered a decision on whether it will hear the case.

BB&T has extended credit to and invested in the obligations of states and municipalities and their agencies and has made other investments and loans that

produce tax-exempt income. The income generated from these investments, together with certain other transactions that have favorable tax treatment, have

reduced BB&T’s overall effective tax rate from the statutory rate in all periods presented.

Refer to Note 12 “Income Taxes” in the “Notes to Consolidated Financial Statements” for a reconciliation of the effective tax rate to the statutory tax rate and

a discussion of uncertain tax positions and other tax matters.

38

Source: BB&T CORP, 10-K, February 25, 2016 Powered by Morningstar® Document Research℠

The information contained herein may not be copied, adapted or distributed and is not warranted to be accurate, complete or timely. The user assumes all risks for any damages or losses arising from any use of this information,

except to the extent such damages or losses cannot be limited or excluded by applicable law. Past financial performance is no guarantee of future results.