BB&T 2015 Annual Report Download - page 153

Download and view the complete annual report

Please find page 153 of the 2015 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

|

|

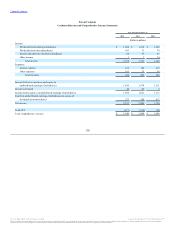

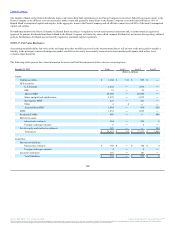

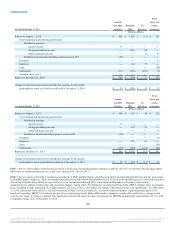

TableofContents

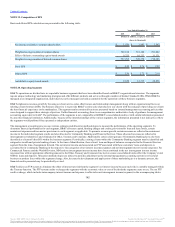

The following table provides a summary of derivative strategies and the related accounting treatment:

Risk exposure Variability in cash flows of

interest payments on floating rate

business loans, overnight funding

and various LIBOR funding

instruments.

Losses in value on fixed rate

long-term debt, CDs, FHLB

advances, loans and state and

political subdivision securities

due to changes in interest rates.

Risk associated with an asset or liability,

including mortgage banking operations and

MSRs, or for client needs. Includes exposure

to changes in market rates and conditions

subsequent to the interest rate lock and

funding date for mortgage loans originated

for sale.

Risk management objective Hedge the variability in the

interest payments and receipts on

future cash flows for forecasted

transactions related to the first

unhedged payments and receipts

of variable interest.

Convert the fixed rate paid or

received to a floating rate,

primarily through the use of

swaps.

For interest rate lock commitment

derivatives and LHFS, use mortgage-based

derivatives such as forward commitments

and options to mitigate market risk. For

MSRs, mitigate the income statement effect

of changes in the fair value of the MSRs.

Treatment for portion that is highly

effective Recognized in AOCI until the

related cash flows from the

hedged item are recognized in

earnings.

Recognized in current period

income along with the

corresponding changes in the fair

value of the designated hedged

item attributable to the risk being

hedged.

Entire change in fair value recognized in

current period income.

Treatment for portion that is ineffective Recognized in current period

income. Recognized in current period

income. Not applicable

Treatment if hedge ceases to be highly

effective or is terminated Hedge is dedesignated. Effective

changes in value that are recorded

in AOCI before dedesignation are

amortized to yield over the period

the forecasted hedged

transactions impact earnings.

If hedged item remains

outstanding, termination proceeds

are included in cash flows from

financing activities and effective

changes in value are reflected as

part of the carrying value of the

financial instrument and

amortized to earnings over its

estimated remaining life.

Not applicable

Treatment if transaction is no longer

probable of occurring during forecast

period or within a short period

thereafter

Hedge accounting is ceased and

any gain or loss in AOCI is

reported in earnings immediately.

Not applicable Not applicable

140

Source: BB&T CORP, 10-K, February 25, 2016 Powered by Morningstar® Document Research℠

The information contained herein may not be copied, adapted or distributed and is not warranted to be accurate, complete or timely. The user assumes all risks for any damages or losses arising from any use of this information,

except to the extent such damages or losses cannot be limited or excluded by applicable law. Past financial performance is no guarantee of future results.