BB&T 2015 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2015 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

|

|

TableofContents

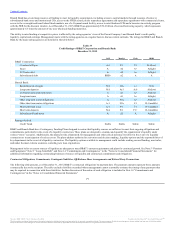

For collectively evaluated loans, the ALLL is determined by multiplying the loan exposure by the loss frequency and loss severity factors. For individually

evaluated loans, the ALLL is determined through review of data specific to the borrower. For TDRs, default expectations and estimated slower prepayment

speeds that are specific to each of the restructured loan populations are incorporated in the determination of the ALLL. Also included in management’s

estimates for loan and lease losses are considerations with respect to the impact of current economic events, the outcomes of which are uncertain. These

events may include, but are not limited to, fluctuations in overall interest rates, political conditions, legislation that may directly or indirectly affect the

banking industry and economic conditions affecting specific geographical areas and industries in which BB&T conducts business.

The methodology used to determine an estimate for the RUFC is inherently similar to the methodology used in calculating the ALLL adjusted for factors

specific to binding commitments, including the probability of funding and exposure at the time of funding. A detailed discussion of the methodology used in

determining the ALLL and the RUFC is included in Note 1 “Summary of Significant Accounting Policies” in the “Notes to Consolidated Financial

Statements.”

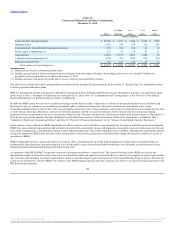

Fair Value of Financial Instruments

The vast majority of assets and liabilities carried at fair value are based on either quoted market prices or market prices for similar instruments. See Note 17

“Fair Value Disclosures” in the “Notes to Consolidated Financial Statements” herein for additional disclosures regarding the fair value of financial

instruments.

Securities

BB&T generally utilizes a third-party pricing service in determining the fair value of its AFS and trading securities. Fair value measurements are derived from

market-based pricing matrices that were developed using observable inputs that include benchmark yields, benchmark securities, reported trades, offers, bids,

issuer spreads and broker quotes. Management performs various procedures to evaluate the accuracy of the fair values provided by the third-party service

provider. These procedures, which are performed independent of the responsible LOB, include comparison of pricing information received from the third

party pricing service to other third party pricing sources, review of additional information provided by the third party pricing service and other third party

sources for selected securities and back-testing to compare the price realized on any security sales to the daily pricing information received from the third

party pricing service. The IPV committee, which provides oversight to BB&T’s enterprise-wide IPV function, is responsible for oversight of the comparison of

pricing information received from the third party pricing service to other third party pricing sources, approving tolerance limits determined by IPV for price

comparison exceptions, reviewing significant changes to pricing and valuation policies and reviewing and approving the pricing decisions made on any

illiquid and hard-to-price securities. When market observable data is not available, which generally occurs due to the lack of liquidity for certain securities,

the valuation of the security is subjective and may involve substantial judgment by management.

BB&T periodically reviews AFS securities with an unrealized loss. An unrealized loss exists when the current fair value of an individual security is less than

its amortized cost basis. The purpose of the review is to consider the length of time and the extent to which the market value of a security has been below its

amortized cost. The primary factors BB&T considers in determining whether an impairment is other-than-temporary are long-term expectations and recent

experience regarding principal and interest payments and BB&T’s intent to sell and whether it is more likely than not that the Company would be required to

sell those securities before the anticipated recovery of the amortized cost basis.

MSRs

BB&T has a significant mortgage loan servicing portfolio with two classes of MSRs for which it separately manages the economic risk: residential and

commercial. Residential MSRs are primarily carried at fair value with changes in fair value recorded as a component of mortgage banking income. BB&T

uses various derivative instruments to mitigate the income statement effect of changes in fair value due to changes in valuation inputs and assumptions of its

residential MSRs. MSRs do not trade in an active, open market with readily observable prices. While sales of MSRs do occur, the precise terms and

conditions typically are not readily available. Accordingly, BB&T estimates the fair value of residential MSRs using an OAS valuation model to project

MSR cash flows over multiple interest rate scenarios, which are then discounted at risk-adjusted rates. The OAS model considers portfolio characteristics,

contractually specified servicing fees, prepayment assumptions, delinquency rates, late charges, other ancillary revenue, costs to service and other economic

factors. BB&T reassesses and periodically adjusts the underlying inputs and assumptions in the OAS model to reflect market conditions and assumptions that

a market participant would consider in valuing the MSR asset.

77

Source: BB&T CORP, 10-K, February 25, 2016 Powered by Morningstar® Document Research℠

The information contained herein may not be copied, adapted or distributed and is not warranted to be accurate, complete or timely. The user assumes all risks for any damages or losses arising from any use of this information,

except to the extent such damages or losses cannot be limited or excluded by applicable law. Past financial performance is no guarantee of future results.