BB&T 2015 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2015 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

|

|

TableofContents

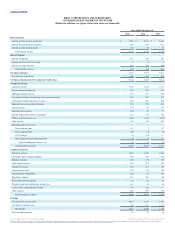

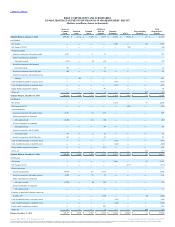

Use of Estimates in the Preparation of Financial Statements

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of

assets and liabilities and disclosure of contingent assets and liabilities as of the date of the financial statements and the reported amounts of revenues and

expenses during the reporting periods. Actual results could differ from those estimates. Material estimates that are particularly susceptible to significant

change include the determination of the ACL, determination of fair value for financial instruments, valuation of goodwill, intangible assets and other

purchase accounting related adjustments, benefit plan obligations and expenses, and tax assets, liabilities and expense.

Business Combinations

BB&T accounts for business combinations using the acquisition method of accounting. The accounts of an acquired entity are included as of the date of

acquisition, and any excess of purchase price over the fair value of the net assets acquired is capitalized as goodwill.

BB&T typically issues common stock and/or pays cash for an acquisition, depending on the terms of the acquisition agreement. The value of common shares

issued is determined based on the market price of the stock as of the closing of the acquisition.

Cash and Cash Equivalents

Cash and cash equivalents include cash and due from banks, interest-bearing deposits with banks and Federal funds sold and securities purchased under

resale agreements or similar arrangements. Cash and cash equivalents have maturities of three months or less. Accordingly, the carrying amount of such

instruments is considered a reasonable estimate of fair value.

Restricted Cash

Restricted cash represents amounts posted as collateral for derivatives in a loss position.

Securities

BB&T classifies marketable investment securities as HTM, AFS or trading. Interest income and dividends on securities are recognized in income on an

accrual basis. Premiums and discounts on debt securities are amortized as an adjustment to interest income using the interest method.

Debt securities are classified as HTM where BB&T has both the intent and ability to hold the securities to maturity. These securities are reported at amortized

cost.

Debt securities, which may be sold to meet liquidity needs arising from unanticipated deposit and loan fluctuations, changes in regulatory capital

requirements, or unforeseen changes in market conditions, are classified as AFS. AFS securities are reported at estimated fair value, with unrealized gains and

losses reported in AOCI, net of deferred income taxes, in the shareholders’ equity section of the Consolidated Balance Sheets. Gains or losses realized from

the sale of AFS securities are determined by specific identification and are included in noninterest income.

Each HTM and AFS security in a loss position is evaluated for OTTI. BB&T considers such factors as the length of time and the extent to which the fair value

has been below amortized cost, long term expectations and recent experience regarding principal and interest payments, BB&T’s intent to sell and whether it

is more likely than not that the Company would be required to sell those securities before the anticipated recovery of the amortized cost basis. The credit

component of an OTTI loss is recognized in earnings and the non-credit component is recognized in AOCI in situations where BB&T does not intend to sell

the security and it is more-likely-than-not that BB&T will not be required to sell the security prior to recovery. Subsequent to recognition of OTTI, an

increase in expected cash flows is recognized as a yield adjustment over the remaining expected life of the security based on an evaluation of the nature of

the increase.

Trading account securities, which include both debt and equity securities, are reported at fair value and included in other assets in the Consolidated Balance

Sheets. Unrealized fair value adjustments, fees, and realized gains or losses from trading account activities (determined by specific identification) are

included in noninterest income. Interest income on trading account securities is included in interest on other earning assets.

88

Source: BB&T CORP, 10-K, February 25, 2016 Powered by Morningstar® Document Research℠

The information contained herein may not be copied, adapted or distributed and is not warranted to be accurate, complete or timely. The user assumes all risks for any damages or losses arising from any use of this information,

except to the extent such damages or losses cannot be limited or excluded by applicable law. Past financial performance is no guarantee of future results.