BB&T 2015 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2015 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

|

|

TableofContents

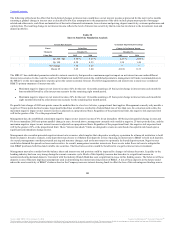

BB&T monitors the ability to meet customer demand for funds under both normal and stressed market conditions. In considering its liquidity position,

management evaluates BB&T’s funding mix based on client core funding, client rate-sensitive funding and non-client rate-sensitive funding. In addition,

management also evaluates exposure to rate-sensitive funding sources that mature in one year or less. Management also measures liquidity needs against 30

days of stressed cash outflows for Branch Bank. To ensure a strong liquidity position, management maintains a liquid asset buffer of cash on hand and highly

liquid unpledged securities. BB&T follows regulation YY for purposes of determining the liquid asset buffer. BB&T’s policy is to use the greater of 5% or a

range of projected net cash outflows over a 30 day period. As of December 31, 2015 and 2014, BB&T’s liquid asset buffer was 13.5% and 13.6%,

respectively, of total assets.

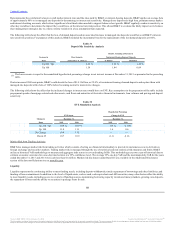

BB&T is considered to be a “modified LCR” holding company. BB&T would be subject to full LCR requirements if its operations were to fall under the

“internationally active” rules, which would generally be triggered if BB&T’s assets were to increase above $250 billion. BB&T produces LCR calculations

to effectively manage the position of High-Quality Liquid Assets and the balance sheet deposit mix to optimize BB&T’s liquidity position. BB&T’s LCR

was approximately 130% at December 31, 2015, compared to the regulatory minimum for such entities of 90%, which puts BB&T in full compliance with the

rule. The regulatory minimum will increase to 100% on January 1, 2017. As noted above, BB&T is currently subject to the modified LCR requirement.

BB&T routinely evaluates the impact of becoming subject to the full LCR requirement. This includes an evaluation of the changes to the balance sheet and

investment strategy that would be necessary to comply with the requirement. Management does not currently expect the required changes to have a material

impact on BB&T’s financial condition or results of operations.

Parent Company

The purpose of the Parent Company is to serve as the primary source of capital for the operating subsidiaries, with assets primarily consisting of cash on

deposit with Branch Bank, equity investments in subsidiaries, advances to subsidiaries, accounts receivable from subsidiaries, and other miscellaneous assets.

The principal obligations of the Parent Company are payments on long-term debt. The main sources of funds for the Parent Company are dividends and

management fees from subsidiaries, repayments of advances to subsidiaries, and proceeds from the issuance of equity and long-term debt. The primary uses of

funds by the Parent Company are for investments in subsidiaries, advances to subsidiaries, dividend payments to common and preferred shareholders,

retirement of common stock and payments on long-term debt.

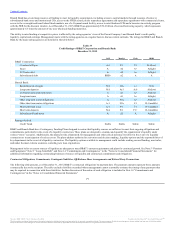

The primary source of funds used for Parent Company cash requirements was dividends received from subsidiaries. See Note 16 “Parent Company Financial

Statements” for additional information regarding dividends from subsidiaries. In addition, the Parent Company issued $1.0 billion of senior notes and repaid

$934 million of long-term debt. During periods that the Parent Company has funds raised through master note agreements with commercial clients, these

funds are placed in a note receivable at Branch Bank primarily for its use in meeting short-term funding needs and, to a lesser extent, to support the short-term

cash needs of the Parent Company. There were no master notes outstanding as of December 31, 2015 or 2014.

Liquidity at the Parent Company is more susceptible to market disruptions. BB&T prudently manages cash levels at the Parent Company to cover a minimum

of one year of projected contractual cash outflows which includes unfunded external commitments, debt service, preferred dividends and scheduled debt

maturities without the benefit of any new cash infusions. Generally, BB&T maintains a significant buffer above the projected one year of contractual cash

outflows. In determining the buffer, BB&T considers cash requirements for common and preferred dividends, unfunded commitments to affiliates, being a

source of strength to its banking subsidiaries and being able to withstand sustained market disruptions that could limit access to the capital markets. As of

December 31, 2015 and 2014, the Parent Company had 36 months and 31 months, respectively, of cash on hand to satisfy projected contractual cash

outflows as described above.

Branch Bank

BB&T carefully manages liquidity risk at Branch Bank. Branch Bank’s primary source of funding is customer deposits. Continued access to customer

deposits is highly dependent on the confidence the public has in the stability of the bank and its ability to return funds to the client when requested. BB&T

maintains a strong focus on its reputation in the market to ensure continued access to client deposits. BB&T integrates its risk appetite into its overall risk

management framework to ensure the bank does not exceed its risk tolerance through its lending and other risk taking functions and thus risk becoming

undercapitalized. BB&T believes that sufficient capital is paramount to maintaining the confidence of its depositors and other funds providers. BB&T has

extensive capital management processes in place to ensure it maintains sufficient capital to absorb losses and maintain a highly capitalized position that will

instill confidence in the bank and allow continued access to deposits and other funding sources. Branch Bank monitors many liquidity metrics at the bank

including funding concentrations, diversification, maturity distribution, contingent funding needs and ability to meet liquidity requirements under times of

stress.

70

Source: BB&T CORP, 10-K, February 25, 2016 Powered by Morningstar® Document Research℠

The information contained herein may not be copied, adapted or distributed and is not warranted to be accurate, complete or timely. The user assumes all risks for any damages or losses arising from any use of this information,

except to the extent such damages or losses cannot be limited or excluded by applicable law. Past financial performance is no guarantee of future results.