BB&T 2015 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2015 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

|

|

TableofContents

·If the estimated credit loss on a loan pool is reduced:

oIf the loan pool has an allowance, the allowance is first reduced to $0 (and, if applicable, 80% of this reduction decreases the FDIC loss share

asset) through income.

oIf the loan pool does not have an allowance (or it is first reduced to $0 and there remains additional expected cash flows), the excess of expected

cash flows is recognized as a yield adjustment over the remaining expected life of the loan.

oThe decrease in expected reimbursement from the FDIC is recognized in income prospectively using a level yield methodology over the

remaining life of the loss share agreements.

oThe increase in the amount expected to be paid to the FDIC as a result of the aggregate loss calculation is recognized prospectively in

proportion to expected loan income over the remaining life of the loss share agreements.

The accounting treatment for securities acquired from the FDIC is summarized below:

·Prior to the recognition of OTTI on a security acquired from the FDIC:

oThe purchase discount established at acquisition is accreted into income over the expected life of the underlying securities using a level yield

methodology.

oChanges to the expected life of the securities are recognized with a cumulative adjustment to the accretion recognized.

·Subsequent to recognition of OTTI, which is determined using the same methodology that is applied to securities that were not acquired from the

FDIC, an increase in expected cash flows is recognized as a yield adjustment over the remaining expected life of the security based on an evaluation

of the nature of the increase.

·The income statement effect of the above items is offset by the applicable loss share percentage in FDIC loss share income, net, which cumulatively

resulted in a liability of $265 million as of December 31, 2015. Subsequent to September 30, 2014, with the expiration of commercial loss sharing,

any OTTI will not be offset.

·Securities acquired from the FDIC are classified as AFS and carried at fair market value. The changes in unrealized gains/losses (down to the

contractually specified amount) are offset by the applicable loss share percentage in AOCI, which resulted in a liability of $271 million as of

December 31, 2015.

·BB&T would only owe these amounts to the FDIC if BB&T were to sell these securities prior to the end of the third quarter of 2017. BB&T has no

current intent to dispose of the securities.

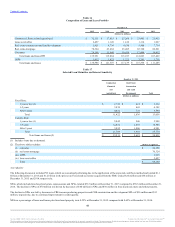

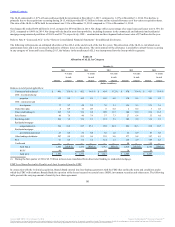

The following table provides information related to the components of the FDIC loss share receivable (payable):

Loans $ 285 $ 11 $ 534 $ 123

Securities (536) (518) (565) (535)

Aggregate loss calculation (149) (158) (132) (161)

Total $ (400) $ (665) $ (163) $ (573)

The decrease in the carrying amount attributable to loans acquired from the FDIC was due to the receipt of cash from the FDIC, negative accretion due to

credit loss improvement and the offset to the provision for loans acquired from the FDIC, which was a benefit for the current year. The change in the carrying

amount attributable to the aggregate loss calculation is primarily due to accretion of the expected payment. The fair values are based upon a discounted cash

flow methodology that is consistent with the acquisition date methodology. The fair value attributable to acquired loans and the aggregate loss calculation

changes over time due to the receipt of cash from the FDIC, updated credit loss assumptions and the passage of time. The fair value attributable to securities

acquired from the FDIC is based upon the timing and amount that would be payable to the FDIC should they settle at the current fair value at the conclusion

of the gain sharing period.

58

Source: BB&T CORP, 10-K, February 25, 2016 Powered by Morningstar® Document Research℠

The information contained herein may not be copied, adapted or distributed and is not warranted to be accurate, complete or timely. The user assumes all risks for any damages or losses arising from any use of this information,

except to the extent such damages or losses cannot be limited or excluded by applicable law. Past financial performance is no guarantee of future results.