BB&T 2015 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2015 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

|

|

TableofContents

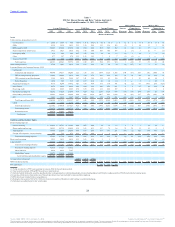

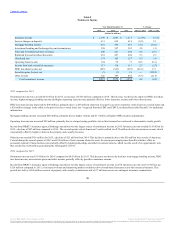

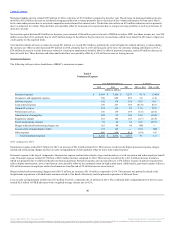

The allocated provision for credit losses was a benefit of $107 million in 2014, compared to expense of $12 million in 2013, reflecting the benefit of the

previously discussed sales of residential mortgage loans during 2014 and a decrease in loan balances consistent with the current strategy of selling

substantially all conforming mortgage loan production. Noninterest expense increased $141 million, which primarily reflects a $27 million charge in the

fourth quarter of 2014 related to the previously discussed ongoing review of mortgage processes, as well as adjustments in the second quarter of 2014

totaling $118 million related to the previously discussed FHA-insured loan exposures.

Dealer Financial Services

Dealer Financial Services net income was $183 million in 2014, a decrease of $21 million, or 10.3%, compared to 2013.

The allocated provision for credit losses increased $23 million primarily due to higher charge-offs in the nonprime automobile loan portfolio as credit trends

in that portfolio continue to normalize. Noninterest expense increased $8 million, driven by higher personnel expense, primarily related to Regional

Acceptance Corporation’s geographic expansion, and operating charge-offs.

Dealer Financial Services grew average loans by $1.1 billion, or 10.5%, compared to 2013 as a result of strong growth in both the prime and nonprime auto

lending businesses.

Specialized Lending

Specialized Lending net income was $257 million in 2014, a decrease of $16 million, or 5.9%, compared to 2013.

Segment net interest income decreased $120 million to $432 million, which primarily reflects the sale of a consumer lending subsidiary during the fourth

quarter of 2013 and lower credit spreads on loans earned during 2014. Noninterest income increased $10 million driven by higher operating lease income.

The sale of the specialized lending subsidiary also had a beneficial impact on the allocated provision for credit losses, which decreased $46 million.

Noninterest expense decreased $34 million driven by lower personnel, occupancy and equipment, loan processing and professional services expense.

Small ticket consumer finance, equipment finance, governmental finance and commercial mortgage experienced strong loan growth compared to 2013.

Insurance Services

Insurance Services net income was $233 million in 2014, an increase of $46 million, or 24.6%, compared to 2013.

Insurance Services’ noninterest income of $1.7 billion increased $128 million, primarily due to increased commissions on new and renewal property and

casualty business, higher performance-based commissions and an increase in employee benefit commissions. Noninterest expense increased $54 million

driven by higher salaries, performance-based incentives, operating charge-offs and business referral expense.

Financial Services

Financial Services net income was $282 million in 2014, a decrease of $23 million, or 7.5%, compared to 2013.

Noninterest income increased $22 million, primarily due to higher trust, investment advisory and investment banking income. Client invested assets totaled

$119.0 billion as of December 31, 2014, an increase of $7.8 billion, or 7.0%, compared to 2013.

The allocated provision for credit losses increased $7 million compared to the prior year as a result of growth in the Corporate Banking and BB&T Wealth

loan portfolios. Noninterest expense increased $30 million, primarily due to higher personnel expense, operating charge-offs, sub-advisory fees and

occupancy and equipment expense. Allocated corporate expenses increased $19 million, primarily driven by internal business initiatives and growth in the

segment.

Financial Services continued to generate significant loan growth through expanded lending strategies. Corporate Banking’s average loan balances increased

$1.7 billion, or 23.4%, compared to 2013, while BB&T Wealth’s average loan balances increased $229 million, or 25.6%. BB&T Wealth also grew

transaction account balances by $438 million, or 18.8%, and money market and savings balances by $534 million, or 8.6%, compared to 2013.

42

Source: BB&T CORP, 10-K, February 25, 2016 Powered by Morningstar® Document Research℠

The information contained herein may not be copied, adapted or distributed and is not warranted to be accurate, complete or timely. The user assumes all risks for any damages or losses arising from any use of this information,

except to the extent such damages or losses cannot be limited or excluded by applicable law. Past financial performance is no guarantee of future results.