BB&T 2015 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2015 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

|

|

TableofContents

Lending Activities

The primary goal of the BB&T lending function is to help clients achieve their financial goals by providing quality loan products that are fair to the client

and profitable to the Company. Management believes that this purpose can best be accomplished by building strong, profitable client relationships over

time, with BB&T becoming an important contributor to the prosperity and well-being of its clients. In addition to the importance placed on client knowledge

and continuous involvement with clients, BB&T’s lending process incorporates the standards of a consistent company-wide credit culture and an in-depth

local market knowledge. Furthermore, the Company employs strict underwriting criteria governing the degree of assumed risk and the diversity of the loan

portfolio in terms of type, industry and geographical concentration. In this context, BB&T strives to meet the credit needs of clients in its markets while

pursuing a balanced strategy of loan profitability, loan growth and loan quality.

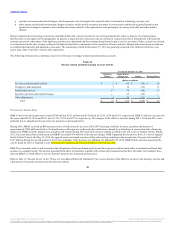

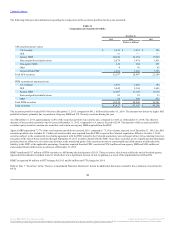

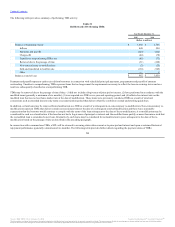

Commercial:

Commercial and industrial $ 48,047 $ 46,462 $ 42,541 $ 41,448 $ 40,383

CRE - income producing properties 13,264 12,514 10,730 10,680 10,681

CRE - construction and development 3,766 3,502 2,767 2,734 2,772

Dealer floor plan 1,164 1,056 1,010 1,040 1,053

Direct retail lending 10,896 9,926 8,449 8,191 8,085

Sales finance 10,533 10,386 9,507 9,458 9,194

Revolving credit 2,458 2,421 2,365 2,385 2,427

Residential mortgage 30,334 30,384 29,862 30,427 31,046

Other lending subsidiaries 13,281 12,837 11,701 11,318 11,351

PCI 1,070 1,052 1,055 1,156 1,309

Total average loans and leases HFI 134,813 130,540 119,987 118,837 118,301

LHFS 1,377 1,959 2,069 1,398 1,611

Total average loans and leases $ 136,190 $ 132,499 $ 122,056 $ 120,235 $ 119,912

Average loans held for investment for the fourth quarter of 2015 were $134.8 billion, up $4.3 billion compared to the third quarter of 2015. Excluding

acquisitions (which comprises Susquehanna, The Bank of Kentucky, both branch acquisitions in Texas and BankAtlantic), average loans held for investment

were up approximately 2.0% on an annualized basis.

Average commercial and industrial loans increased $1.6 billion during the fourth quarter of 2015. Approximately $740 million of the increase was the result

of acquisitions while the remaining increase primarily reflects continued growth in large corporate lending. Average commercial real estate – income

producing properties loans increased $750 million and average commercial real estate – construction and development loans increased $264 million, with

the majority of both of these increases being attributable to acquisitions. Dealer floor plan average loans, which were not significantly impacted by

acquisition activity, were up $108 million or 40.6% annualized, due to strong organic growth.

Direct retail lending average loans increased $970 million; approximately $735 million of the growth was due to acquisitions. Other lending subsidiaries

average loans increased $444 million, with approximately half of the increase due to acquisitions.

Excluding acquisition activity, average sales finance loans declined approximately $400 million, which is partially due to dealer pricing structure changes

implemented during the third quarter. Average residential mortgage loans decreased approximately $430 million excluding acquisitions, which reflects the

continued strategy to sell conforming residential mortgage loan production.

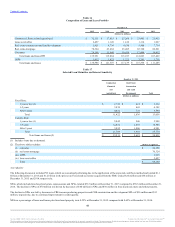

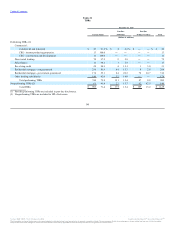

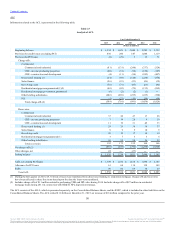

The following table excludes sales finance and retail other lending subsidiaries loans as the substantial majority of those loans have fixed interest rates:

46

Source: BB&T CORP, 10-K, February 25, 2016 Powered by Morningstar® Document Research℠

The information contained herein may not be copied, adapted or distributed and is not warranted to be accurate, complete or timely. The user assumes all risks for any damages or losses arising from any use of this information,

except to the extent such damages or losses cannot be limited or excluded by applicable law. Past financial performance is no guarantee of future results.