Philips 2015 Annual Report Download - page 122

Download and view the complete annual report

Please find page 122 of the 2015 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

|

|

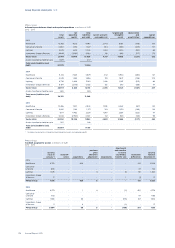

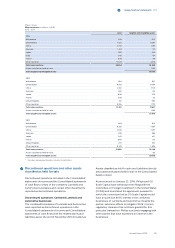

Group nancial statements 12.9

122 Annual Report 2015

relevant to the Company are set out below. Changes to

other standards, following from amendments and the

annual improvement cycles, are not expected to have

a material impact on the Company’s nancial

statements.

IFRS 9 Financial Instruments

IFRS 9 Financial Instruments brings together the

classication and measurement, impairment and hedge

accounting phases of the IASB’s project to replace IAS

39 Financial Instruments: Recognition and

Measurement.

IFRS 9 adds a new expected loss impairment model

and amendments to classication and measurement

for nancial assets. The impairment model is based on

the concept of providing for expected losses at

inception of a contract, except in the case of purchased

or originated credit-impaired nancial assets, where

expected credit losses are incorporated into the

eective interest rate.

The standard supersedes all previous versions of IFRS

9 and is eective for periods beginning on or after

January 1, 2018. It is not yet endorsed by the EU. The

Company is currently in the process of assessing the

impact of the new Standard.

IFRS 15 Revenue from Contracts with Customers

IFRS 15 species how and when revenue is recognized

as well as describes more informative and relevant

disclosures. The standard supersedes IAS 18 Revenue,

IAS 11 Construction Contracts and a number of revenue-

related interpretations.

The new standard provides a single, principles based

ve-step model to be applied to all contracts with

customers. Furthermore, it provides new guidance on

whether revenue should be recognized at a point in

time or over time. The standard also introduces new

guidance on costs of fullling and obtaining a contract,

specifying the circumstances in which such costs

should be capitalized. Costs that do not meet the

criteria must be expensed when incurred.

IFRS 15 must be applied for periods beginning on or

after January 1, 2018. It is not yet endorsed by the EU.

The Company is currently assessing the impact of the

new standard.

IFRS 16 Leases

For lessees, IFRS 16 (issued on January 13, 2016)

requires most leases to be recognized on-balance

(under a single model), eliminating the distinction

between operating and nance leases. Lessor

accounting however remains largely unchanged and

the distinction between operating and nance leases is

retained. IFRS 16 supersedes IAS 17 Leases and related

interpretations.

Under IFRS 16 a lessee recognizes a right-of-use asset

and a lease liability. The right-of-use asset is treated

similarly to other non-nancial assets and is

depreciated accordingly. The lease liability is initially

measured at the present value of the lease payments

payable over the lease term, discounted at the rate

implicit in the lease if that can be readily determined,

and the liability accrues interest. As with current IAS 17,

under IFRS 16 lessors classify leases as operating or

nance in nature.

IFRS 16 must be applied for periods beginning on or

after January 1, 2019, with earlier adoption permitted if

abovementioned IFRS 15 has also been applied. IFRS

16 is not yet endorsed by the EU. The Company is

currently assessing the impact of the new standard.