Philips 2015 Annual Report Download - page 181

Download and view the complete annual report

Please find page 181 of the 2015 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

|

|

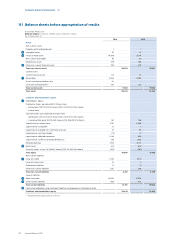

Company nancial statements 13.5

Annual Report 2015 181

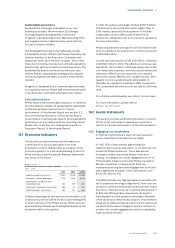

Valuation of goodwill

Key audit matter Under EU-IFRSs, the Company is required to test the amount of goodwill for impairment, both annually and if

there is a trigger for testing. The impairment tests were signicant to our audit due to the complexity of the

assessment process and signicant judgments and assumptions involved which are aected by expected future

market or economic conditions. At December 31, 2015, the goodwill amounted to EUR 8.5 billion.

Our response Our audit procedures included, amongst others, the involvement of a valuation expert to assist us in evaluating

the assumptions and methodologies used by the Company, in particular those relating to the compound sales

growth rate and pre-tax discount rate. The cash ow projections, mainly for Healthcare cash-generating units

(Respiratory Care & Sleep Management, Image-Guided Therapy, Patient Care & Monitoring Solutions and Home

Monitoring) and Lighting cash-generating units (Professional Lighting Solutions and Consumer Luminaires) have

been assessed and challenged by us, and includes an assessment of the historical accuracy of management’s

estimates and evaluation of business plans. We have also tested the eectiveness of the Company’s internal

controls around the valuation of goodwill.

We believe the assumptions used are within the acceptable range. Based on the impairment test, it was noted

that with regard to the headroom for cash-generating unit Consumer Luminaires, the estimated recoverable

amount approximates the carrying value of the cash-generating unit. Furthermore, we noted that the headroom

for the cash-generating units Professional Lighting Solutions and Home Monitoring is relatively limited. We also

assessed the adequacy of the disclosures in Section 12.9, Note 11 Goodwill relating to those assumptions to

which the outcome of the impairment test is most sensitive, that is, those that have the most signicant eect on

the determination of the recoverable amount of goodwill.

Accounting for income tax positions

Key audit matter Income tax was signicant to our audit because the assessment process is complex and the amounts involved

are material to the nancial statements as a whole. The Company has extensive international operations and in

the normal course of business makes judgments and estimates in relation to tax issues and exposures resulting

in the recognition of other tax liabilities. At December 31, 2015, the net deferred tax assets are valued at EUR 2.8

billion and the other tax liability related to tax uncertainties is valued at EUR 454 million.

Our response We have tested the completeness and accuracy of the amounts reported for current and deferred tax, including

the assessment of disputes with tax authorities, based on the developments in 2015 and the impact of the

scheduled separation of the Company. In this area our audit procedures included, amongst others, assessment

of correspondence with the relevant tax authorities, testing the eectiveness of the Company’s internal controls

around the recording and continuous re-assessment of the other tax liabilities, and the involvement of our local

component auditors including tax specialists in those components determined to be the regions with signicant

tax risk. In respect of deferred tax assets, we analyzed and tested management’s assumptions used to determine

the probability that deferred tax assets recognized in the balance sheet will be recovered through taxable

income in the countries where the deferred tax assets originated and during the periods when the deferred tax

assets become deductible. During our procedures, we use amongst others budgets, forecasts and tax laws and in

addition we assessed the historical accuracy of management’s assumptions. We believe the assumptions used

are within the acceptable range. We also assessed the adequacy of the Company’s disclosure included in

Section 12.9, Note 8 Income taxes in respect of income tax positions and uncertain tax positions.

Revenue recognition

Key audit matter Sales contracts for certain projects in the Healthcare and Lighting sectors typically involve multi-element

contracts, for example a single sales transaction that combines the delivery of goods and rendering of services,

and involve separately identiable components that are recognized based on relative fair value. This gives rise to

the risk that sales could be misstated due to the complexity of the multi-element contracts and the incorrect

valuation of the relative fair value elements. Other sales are generally recognized when the risks and rewards of

the underlying products have been transferred to the customer and tend not to have multiple deliverable

elements. There is a risk that sales may be deliberately overstated as a result of management override resulting

from the pressure management may feel to achieve planned results. The management of the Group focuses on

sales as a key performance measure which could create an incentive for sales to be recognized before the risks

and rewards have been transferred.

Our response Our audit procedures included, amongst others, assessing the appropriateness of the Company’s revenue

recognition accounting policies including those relating to multi-element contracts and assess compliance with

the policies in terms of EU-IFRS. We tested the eectiveness of the Company’s controls over calculation of

rebates, fair value determination of multi-element sales contracts, and the correct timing of revenue recognition.

We also assessed sales transactions taking place before and after year-end to ensure that revenue was

recognized in the correct period and assessed the accuracy of the sales recorded, based amongst others on

inspection of sales contracts, hand over certicates and installation hours reported after recognition of revenue.

We also assessed the adequacy of the sales disclosures contained in Section 12.9, Note 2 Information by sector

and main country and Note 6 Income from operations.