Philips 2012 Annual Report Download - page 138

Download and view the complete annual report

Please find page 138 of the 2012 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

|

|

12 Group financial statements 12.10 - 12.10

138 Annual Report 2012

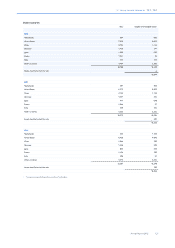

Investing category. In the consolidated statements of cash flows,

prior years have been adjusted as shown in the table below to reflect

appropriate presentation:

2010 2011

Statements of cash flows

Operating: Depreciation and amortization (14) (2)

Operating: Other items 14 2

Operating: Decrease (increase) in inventories (47) (68)

Investing: Capital expenditures on property,

plant and equipment 49 71

Financing: Proceeds from issuance of long-

term debts (2) (3)

IFRS accounting standards adopted as from 2013 and onwards

The following standards and amendments to existing standards have

been published and are mandatory for the Company beginning on or

after January 1, 2013 or later periods, and the Company has not yet

early adopted them.

IAS 1 Presentation of financial statements (2011 amendment)

The new amendment requires separation of items presented in other

comprehensive income into two groups, based on whether or not they

can be recycled into the Statement of income in the future. Items that

will not be recycled in the future are presented separately from items

that may be recycled in the future. The amendment will be adopted on

January 1, 2013 and will be applied retrospectively. The amendment

was endorsed by the EU. The application of this amendment impacts

presentation and disclosures only.

IAS 19 Employee benefits

The revisions to IAS 19 are effective for annual periods beginning on

or after January 1, 2013, and have been endorsed by the EU. In general,

the amendment no longer allows for deferral of actuarial gains and

losses or cost of plan changes and it introduces significant changes to

the recognition and measurement of defined-benefit pension expenses

and their presentation in the Statement of income. Additional

disclosure requirements have been added for risks and plan objectives

and the distinction between short-term and other long-term benefits

has been revised. The revisions further clarify the classification of

various costs involved in benefit plans like expenses and taxes.

The amendment will have a material impact on income from operations

and net income of the Company, resulting from the changes in

measurement and reporting of expected returns on plan assets (and

interest costs), which is currently reported under income from

operations. The revised standard requires interest income or expense

to be calculated on the net balance recognized, with the rate used to

discount the defined-benefit obligations.

There is no impact on the cash flow statement and the balance sheet,

since the Company already applies immediate recognition of actuarial

gains and losses in other comprehensive income. The Company also

has some unrecognized past-service cost gains and losses which must

be recognized. The net impact lowers our balance sheet liabilities with

EUR 10 million.

The new standard no longer allows for accrual of future pension

administration costs as part of the DBO. Such costs should be expensed

as incurred. Under the current standard, the Company in the Dutch

plan includes a surcharge for pension administration costs as part of the

service costs into the DBO. With the adoption of the new standard

this accrual needs to be eliminated resulting in an exclusion of EUR 200

million from the DBO, thereby improving the funded status. This

funded status improvement is offset by the impact of the asset ceiling

test regarding the Dutch plan’s surplus, and hence there is no further

impact on the Company’s balance sheet figures.

The expected negative impact of IAS 19 Revised for post employment

defined-benefit plans on Income from Operations and Income before

tax for 2013 (as compared to current IAS 19) is:

Income from operations EUR (280) million

Financial income and expenses EUR (75) million

Income before taxes EUR (355) million

As from January 1, 2013 the Company will present net interest expense

as part of Financial income and expenses. Comparative figures will be

restated accordingly.

The standard also enhances the definition of termination benefits and

what constitutes a benefit for future service. In many cases these

clarifications are reinforcing the current guidance; therefore this is not

expected to materially impact the Consolidated financial statements.

IFRS 9 Financial Instruments

The standard introduces certain new requirements for classifying and

measuring financial assets and liabilities. IFRS 9 divides all financial assets

that are currently in the scope of IAS 39 into two classifications, those

measured at amortized cost and those measured at fair value. The

standard along with proposed expansion of IFRS 9 for classifying and

measuring financial liabilities, derecognition of financial instruments,

impairment, and hedge accounting will be applicable from January 1,

2015, although entities are permitted to adopt earlier. This standard

has not yet been endorsed by the EU. The new standard will primarily

impact the accounting for the available-for-sale securities within Philips

and will, accordingly, change the timing and placement (profit or loss

versus other comprehensive income) of changes in the respective fair

value. The actual impact in the year it is applied cannot be estimated

on a reasonable basis.

IFRS 10 Consolidated Financial Statements, IFRS 11 Joint

Arrangements and IFRS 12 Disclosure of Interests in Other

Entities (2011)

IFRS 10 introduces a single control model to determine whether an

investee should be consolidated. The new standard includes guidance

on control with less than half of the voting rights (‘de facto’ control),

participating and protective voting rights and agent/principal

relationships. The Company does not expect that the adoption will have

a significant impact on the Company’s Consolidated financial

statements.

Under IFRS 11, the structure of the joint arrangement, although still an

important consideration, is no longer the main factor in determining

the type of joint arrangement and therefore the subsequent accounting.

Instead:

• The Company’s interest in a joint operation, which is an arrangement

in which the parties have rights to the assets and obligations for the

liabilities, will be accounted for on the basis of the Company’s

interest in those assets and liabilities.

• The Company’s interest in a joint venture, which is an arrangement

in which the parties have rights to the net assets, will be equity-

accounted.

The currently applied accounting policy by the Company already means

that jointly controlled entities are being accounted for using the equity

method. The adoption therefore does not have a material impact on

the Company’s Consolidated financial statements.

IFRS 12 brings together into a single standard all the disclosure

requirements about an entity’s interests in subsidiaries, joint

arrangements, associates and unconsolidated structured entities. IFRS

12 requires the disclosure of information about the nature, risks and

financial effects of these interests. The Company is currently assessing

the disclosure requirements for interests in subsidiaries, interests in

joint arrangements and associates and unconsolidated structured

entities in comparison with the existing disclosures.

These standards are effective for annual periods beginning on or after

January 1, 2013 with early adoption permitted.