RBS 2011 Annual Report Download - page 112

Download and view the complete annual report

Please find page 112 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

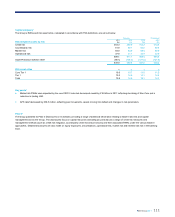

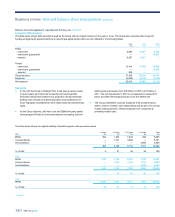

110 RBS Group 2011

Business review Risk and balance sheet management continued

Balance sheet management

All disclosures in this section (pages 110 to 133) are audited unless

otherwise indicated by an asterisk (*).

Two of the Group’s four key strategic risk objectives relate to the

maintenance of capital adequacy and ensuring stable and efficient

access to liquidity and funding. This section on balance sheet

management explains how the Group is performing on achieving these

objectives.

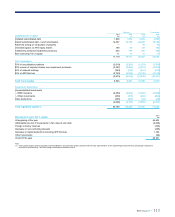

Capital management

Introduction*

The Group aims to maintain an appropriate level of capital to meet its

business needs and regulatory requirements as capital adequacy and

risk management are closely aligned. The Group operates within an

agreed risk appetite whilst optimising the use of shareholders’ funds to

deliver sustainable returns.

The appropriate level of capital is determined based on the dual aims of:

(i) meeting minimum regulatory capital requirements; and (ii) ensuring the

Group maintains sufficient capital to uphold investor and rating agency

confidence in the organisation, thereby supporting the business franchise

and funding capacity.

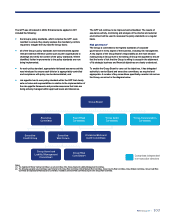

Governance*

The Group Asset and Liability Management Committee (GALCO) is

responsible for ensuring the Group maintains adequate capital at all

times. The newly established Capital and Stress Testing Committee

(CAST) is a cross-functional body driving and directing integrated risk

capital activities including stress testing economic capital and capital

allocation. These activities have linkages to capital planning, risk appetite

and regulatory change. CAST reports through GALCO and comprises

senior representatives from Risk Management, Group Finance and

Group Treasury.

Determining appropriate capital*

The minimum regulatory capital requirements are identified by the Group

through the Internal Capital Adequacy Assessment Process and then

agreed between the Group Board and the appropriate supervisory

authority.

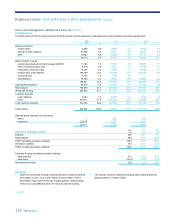

The Group’s own determination of how much capital is sufficient is

derived from the desired credit rating level and the application of both

internally and externally defined stress tests that identify potential

changes in capital ratios over time.

Monitoring and maintenance*

Based on these determinations, which are continually reassessed, the

Group aims to maintain capital adequacy both at Group level and in each

regulated entity.

The Group operates a rigorous capital planning process aimed at

ensuring the capital position is controlled within the agreed parameters.

This incorporates regular re-forecasts of the capital positions of the

regulated entities and the overall Group. In the event that the projected

position deteriorates beyond acceptable levels, the Group would issue

further capital and/or revise business plans accordingly.

Stress testing approaches are used to determine the level of capital

required to ensure the Group remains adequately capitalised.

Capital allocation*

Capital resourcesare allocated to the Group’s businesses based on key

performance parameters agreed by the Group Board in the annual

strategic planning process. Principal among these is a profitability metric

which assesses the effective use of the capital allocated to the business.

Projected and actual return on equity is assessed against target returns

set by the Group Board. The allocations also reflect strategic priorities

and balance sheet and funding metrics.

Economic profit is also planned and measured for each division during

the annual planning process. It is calculated by deducting the cost of

equity utilised in the particular business from its operating profit and

measures the value added over and above the cost of equity.

The Group aims to deliver sustainable returns across the portfolio of

businesses with projected business returns stressed to test key

vulnerabilities.

The divisions use return on capital metrics when making pricing decisions

on products and transactions with a view to ensuring customer activity is

appropriately aligned with Group and divisional targets and allocations.

The FSA uses the risk asset ratio as a measure of capital adequacy in

the UK banking sector, comparing a bank’s capital resources with its

RWAs (the assets and off-balance sheet exposures are weighted to

reflect the inherent credit and other risks); by international agreement the

risk asset ratios should not be less than 8% with a Tier 1 component of

not less than 4%.

*unaudited