RBS 2011 Annual Report Download - page 150

Download and view the complete annual report

Please find page 150 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

148 RBS Group 2011

Risk management: Credit risk continued

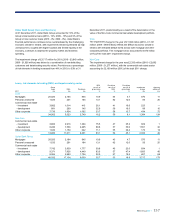

Credit risk measurement*: Credit risk assets by sector and geographical region continued

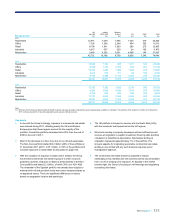

2009

UK

£m

Western

Europe

(excl. UK)

£m

North

America

£m

Asia

Pacific

£m

Latin

America

£m

Other (1)

£m

Total

£m

Core

£m

Non-Core

£m

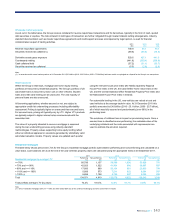

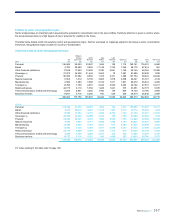

Personal 120,193 23,597 37,680 1,374 63 897 183,804 165,143 18,661

Banks 7,850 36,705 4,975 9,121 1,378 2,137 62,166 58,246 3,920

Other financial institutions 14,800 14,125 17,697 4,820 8,441 1,473 61,356 43,762 17,594

Sovereign (2) 18,172 27,421 4,038 3,950 414 2,217 56,212 53,595 2,617

Property 72,768 35,558 11,221 3,507 3,127 1,440 127,621 74,892 52,729

Natural resources 7,876 9,460 9,817 3,029 3,523 4,972 38,677 26,058 12,619

Manufacturing 11,197 14,875 8,718 3,695 1,306 2,633 42,424 33,400 9,024

Transport (3) 14,097 7,033 7,287 5,294 2,604 7,140 43,455 28,362 15,093

Retail and leisure 25,811 8,236 6,148 3,602 1,205 1,691 46,693 35,580 11,113

Telecommunications, media and technology 6,128 8,340 4,854 2,040 680 1,409 23,451 13,645 9,806

Business services 20,497 6,772 6,950 1,137 1,439 903 37,698 32,375 5,323

319,389 192,122 119,385 41,569 24,180 26,912 723,557 565,058 158,499

Notes:

(1) Comprises Central and Eastern Europe, Middle East, Central Asia and Africa, and supranationals such as the World Bank.

(2) Includes central bank exposures.

(3) Excludes net investment in operating leases in shipping and aviation portfolios as they are accounted for as property, plant and equipment. However, operating leases are included in the monitoring

and management of these portfolios.

(4) 2010 data were restated due to supranational counterparties being re-mapped from Western Europe to Other.

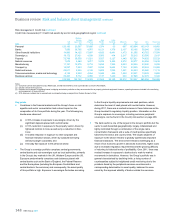

Key points

xConditions in the financial markets and the Group’s focus on risk

appetite and sector concentration had a direct impact on the

composition of its Core portfolio during the year. The following key

trends were observed:

(i) A 35% increase in exposure to sovereigns, driven by the

significant deposits placed with central banks;

(ii) A 10% reduction in exposure to the property sector, driven by

tightened controls in Core as well as by a reduction in Non-

Core;

(iii) A modest reduction in exposure to other corporate and

financial institution sectors, driven by subdued borrowing

activity by larger corporates; and

(iv) A broadly flat exposure to the personal sector.

xThe Group’s sovereign portfolio comprises central governments,

central banks and sub-sovereigns such as local authorities, primarily

in the Group’s key markets in the UK, Western Europe and the US.

Exposure predominantly comprises cash balances placed with

central banks such as the Bank of England, the Federal Reserve

and the Eurosystem (including the European Central Bank and

central banks in the eurozone) and consequently, the asset quality

of this portfolio is high. Exposure to sovereigns fluctuates according

to the Group’s liquidity requirements and cash positions, which

determine the level of cash placed with central banks. However,

during 2011, there was a marked increase in these balances as the

Group boosted its regulatory liquidity position. Information on the

Group’s exposure to sovereigns, including eurozone peripheral

sovereigns, can be found in the Country risk section on page 208.

xThe bank sector is one of the largest in the Group’s portfolio but the

sector is well diversified geographically, largely collateralised and

tightly controlled through a combination of the single name

concentration framework and a suite of credit policies specifically

tailored to the sector and country limits. The largest segment of

exposure to the sector remains to globally systemically important

financial institutions. The environment remains challenging as a

result of low economic growth in advanced economies, higher costs

due to increased regulatory requirements and the growing difficulty

of returning to historical levels of profitability. Over 2011, there was

modest increase in exposure to banks due to mark-to-market

movements in derivatives. However, the Group’s portfolio was in

general characterised by declining limits, a rising number of

counterparties subject to heightened credit monitoring due to the

problems faced by the peripheral eurozone countries and a

corresponding deterioration in asset quality, balanced to some

extent by the improved stability of banks outside the eurozone.

Business review Risk and balance sheet management continued