RBS 2011 Annual Report Download - page 358

Download and view the complete annual report

Please find page 358 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

348 -

349

349 -

350

350 -

351

351 -

352

352 -

353

353 -

354

354 -

355

355 -

356

356 -

357

357 -

358

358 -

359

359 -

360

360 -

361

361 -

362

362 -

363

363 -

364

364 -

365

365 -

366

366 -

367

367 -

368

368 -

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

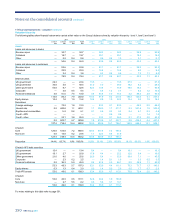

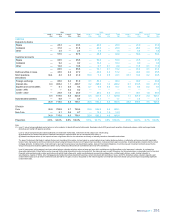

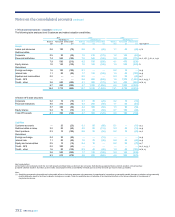

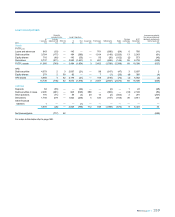

356 RBS Group 2011

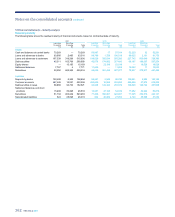

11 Financial instruments - valuation continued

Derivatives

Derivatives are priced using quoted prices for the same or similar

instruments where these are available. However, the majority of

derivatives are valued using pricing models. Inputs for these models are

usually observed directly in the market, or derived from observed prices.

However, it is not always possible to observe or corroborate all model

inputs. Unobservable inputs used are based on estimates taking into

account a range of available information including historic analysis,

historic traded levels, market practice, comparison to other relevant

benchmark observable data and consensus pricing data.

Credit derivatives - APS

The Group purchased credit protection over a portfolio of specified assets

and exposures (covered assets) from HM Treasury. The Group has a

right to terminate the APS at any time provided that the Financial

Services Authority has confirmed in writing to HM Treasury that it has no

objection to the proposed termination. On termination the Group must

pay HM Treasury the higher of the regulatory capital relief received and

£2.5 billion less premiums paid plus the aggregate of amounts received

from the UK Government under the APS. The Group has paid APS

premiums totalling £2,225 million (£125 million in 2011, £700 million in

2010 and £1,400 million in 2009). From 31 December 2011, premiums of

£125 million are payable quarterly until the earlier of 2099 and the date

the Group leaves the Scheme.

The APS is a single contract providing credit protection in respect of the

covered assets. Under IFRS, credit protection is treated either as a

financial guarantee contract or as a derivative financial instrument

depending on the terms of the agreement and the nature of the protected

assets and exposures. The Group has concluded, principally because the

covered portfolio includes significant exposure in the form of derivatives,

that the APS does not meet the criteria to be treated as a financial

guarantee contract. The contract has therefore been accounted for as a

derivative financial instrument. It was recognised initially and measured

subsequently at fair value with changes in fair value recognised in profit

or loss within income from trading activities. There is no change in the

recognition and measurement of the covered assets as a result of the

APS.

For the purpose of the APS, a loss is deemed to have arisen on a

covered asset when that asset has experienced a trigger event which

comprises of failure to pay subject to grace periods, bankruptcy and

restructuring.

Where protection is provided on a particular seniority of exposure, as is

the case with the APS, which requires initial losses to be taken by the

Group, it is termed ‘tranched’ protection. The model being used to value

the APS - a Gaussian Copula model with stochastic recoveries - is used

by the Group to value tranches traded by the exotic credit desk and is a

model that is currently used within the wider market.

The option to exit the APS is not usually present in such tranched trades

and consequently, there is no standard market practice for reflecting this

part of the trade within the standard model framework. The approach that

has been adopted assumes that the Group will not exit the trade before

the minimum level of fees have been paid and at this point it will be clear

whether it should exit the trade or not. The APS derivative is valued as

the payment of the minimum level of fees in return for protection receipts

which are in excess of both the first loss and the total future premiums.

The model primarily uses the following inputs in relation to each individual

non-triggered asset: notional, maturity, probability of default and expected

recovery rate given default. Other key inputs include: the correlation

between the underlying assets; the range of possible recovery rates on

the underlying assets (“alpha”); the size of the first loss. The size of the

first loss is adjusted to reflect both realised and expected losses on

triggered assets as well as the level of expected losses on covered

assets that have been sold, that can be treated as losses for the purpose

of the APS (“loss credits”).

During 2011, refinements were made to the treatment of expected losses

on certain triggered assets following a modification to the trigger events

that apply to some portfolios. The valuation refinement was made to

accurately reflect the impact of the changes. The expected losses arising

on assets that trigger under the modified rules now reflect a range of

possible recovery rates.

The APS protects a wide range of asset types, and hence, the correlation

between the underlying assets cannot be observed from market data. In

the absence of this, the Group determines a reasonable level for this

input. The expected recovery rate given default is based on internally

assessed levels. The probability of default is calculated with reference to

data observable in the market. Where possible, data is obtained for each

asset within the APS, but for most of the assets, such observable data

does not exist. In these cases, this important input is determined from

information available for similar entities by geography and rating. The

approach for doing this was refined during the year in order to accurately

reflect both changes in market conditions and the profile of the portfolio of

covered assets.

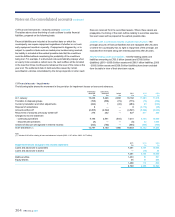

As the inputs into the valuation model are not all observable the APS

derivative is a level 3 instrument. The fair value of the credit protection at

31 December 2011 was £(0.2) billion (2010 - £0.6 billion; 2009 - £1.4

billion).

Notes on the consolidated accounts continued