RBS 2011 Annual Report Download - page 140

Download and view the complete annual report

Please find page 140 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

138 RBS Group 2011

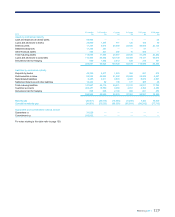

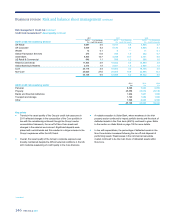

Risk management: Credit risk continued

Problem debt management continued

The wholesale restructured loan data presented in the tables below include only those arrangements that achieved legal completion during 2011 and

that individually exceed respective thresholds set at divisional level, which range from nil to £10 million. This population captures approximately 71% of

that proportion of the wholesale portfolio that is either on Watchlist or under GRG stewardship. Within this population, restructurings amounting to £8.6

billion achieved legal completion during 2011. A further £14.7 billion was in the process of being completed at year end (these loans are not included in

the tables below). Of the loans that were subject to restructuring during 2011 by the divisions, 82% remained in the performing book at 31 December

2011. Of those restructured within the GRG during the year, 17% had been returned to satisfactory by year end.

The asset quality of the restructured loans, the sectors affected and provision coverage are as follows:

Wholesale restructurings by sector AQ1-AQ9 (1)

£m

AQ10 (2)

£m

AQ10 (2)

provision

coverage

%

2011

Property 1,980 2,600 18

Transport 686 694 11

Non-bank financial institutions 228 420 65

Retail and leisure 503 148 24

Other 1,078 251 28

Total 4,475 4,113 22

Notes:

(1) Probability of default less than 100%.

(2) Probability of default is 100%.

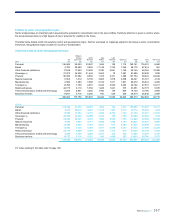

The incidence of the main types of restructuring is analysed below:

Wholesale restructurings by type of arrangement Loans by value

%

2011

Variation in margin 12

Payment holidays and loan rescheduling 87

Forgiveness of all or part of the outstanding debt 31

Other 8

Note:

(1) The total above exceeds 100% as an individual case can involve more than one type of arrangement.

Provisioning for impaired loans

Any one of the above types of restructuring may result in the value of the

outstanding debt exceeding the present value of the estimated future

cash flows from the restructured loan resulting in the recognition of an

impairment loss. Restructurings that include forgiveness of all or part of

the outstanding debt account for the majority of such cases.

The customer’s financial position, anticipated prospects and the likely

effect of the restructuring, including any concessions granted, are

considered in order to establish whether an impairment provision is

required.

Provisions on exposures greater than £1 million are individually assessed

by the GRG. Exposures smaller than £1 million are deemed not to be

individually significant and are assessed collectively by the originating

division.

In the case of non-performing loans that are restructured, the loan

impairment provision assessment (based on management’s best

estimate of the incurred loss) almost invariably takes place prior to the

restructuring. The quantum of the loan impairment provision may change

once the terms of the restructuring are known, resulting in an additional

provision charge or a release of the provision in the period the

restructuring takes place.

Refer to Impairment loss provision methodology on pages 202 and 203.

Business review Risk and balance sheet management continued