RBS 2011 Annual Report Download - page 204

Download and view the complete annual report

Please find page 204 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

202 RBS Group 2011

Risk management: Credit risk continued

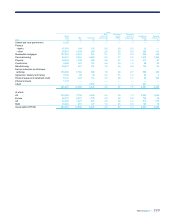

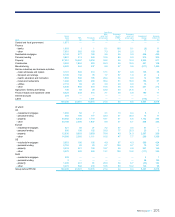

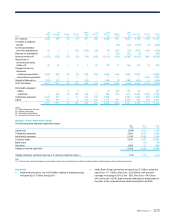

Balance sheet analysis: REIL, provisions and reserves continued

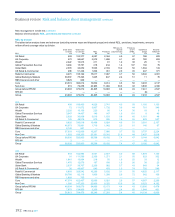

Non-Core

2009

Gross

loans

£m

REIL

£m

Provisions

£m

REIL

as a % of

gross loans

%

Provisions

as a %

of REIL

%

Provisions

as a % of

gross loans

%

Impairment

charge

£m

Amounts

written-off

£m

Central and local government 1,532 — — — — — — —

Finance

-banks 1,360 38 22 2.8 58 1.6 22 —

- other 9,713 501 160 5.2 32 1.6 630 579

Residential mortgages 12,932 614 210 4.7 34 1.6 604 496

Personal lending 6,358 596 366 9.4 61 5.8 701 604

Property 50,372 12,552 2,954 24.9 24 5.9 2,879 613

Construction 5,258 1,775 388 33.8 22 7.4 421 257

Manufacturing 14,402 2,640 1,897 18.3 72 13.2 1,384 691

Service industries and business

activities 33,638 3,546 1,191 10.5 34 3.5 1,464 916

Agriculture, forestry and fishing 553 47 27 8.5 57 4.9 6 1

Finance leases and instalment credit 11,956 591 302 4.9 51 2.5 219 35

Interest accruals 549 — — — — — — —

Latent — — 735 — — — 193 —

148,623 22,900 8,252 15.4 36 5.6 8,523 4,192

of which:

UK 79,043 8,400 2,713 10.6 32 3.4 2,709 1,279

Europe 41,096 10,783 3,740 26.2 35 9.1 2,520 381

US 19,546 2,618 1,144 13.4 44 5.9 2,460 2,080

RoW 8,938 1,099 655 12.3 60 7.3 834 452

Group before RFS MI 148,623 22,900 8,252 15.4 36 5.6 8,523 4,192

Impairment loss provision methodology

Afinancial asset or portfolio of financial assets is impaired and an

impairment loss incurred if there is objective evidence that an event or

events since initial recognition of the asset have adversely affected the

amount or timing of future cash flows from the asset.

For retail loans, which are segmented into collective, homogenous

portfolios, time-based measures, such as days past due, are typically

used as evidence of impairment. For these portfolios, the Group

recognises an impairment at 90 days past due.

For corporate portfolios, given their complexity and nature, the Group

relies not only on time-based measures but also on management

judgement to identify evidence of impairment. Other factors considered

may include: significant financial difficulty of the borrower; a breach of

contract; a loan restructuring; a probable bankruptcy; and any observable

data indicating a measurable decrease in estimated future cash flows.

Depending on various factors as explained below, the Group uses one of

the following three different methods to assess the amount of provision

required: individual; collective; and latent.

xIndividually assessed provisions: provisions required for individually

significant impaired assets are assessed on a case-by-case basis. If

there is objective evidence that an impairment loss has been

incurred, the amount of the loss is measured as the difference

between the assets carrying amount and the present value of the

estimated future cash flows discounted at the financial asset’s

original effective interest rate. Future cash flows are estimated

through a case-by-case analysis of individually assessed assets.

This assessment takes into account the benefit of any guarantee or

other collateral held. The value and timing of cash flow receipts are

based on available estimates in conjunction with facts available at

that time. Timings and amounts of cash flows are reviewed on

subsequent assessment dates, as new information becomes

available. The asset continues to be assessed on an individual basis

until it is repaid in full, transferred to the performing portfolio or

written-off.

Business review Risk and balance sheet management continued