RBS 2011 Annual Report Download - page 144

Download and view the complete annual report

Please find page 144 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

142 RBS Group 2011

Risk management: Credit risk continued

Credit risk mitigation continued

Corporate exposures

The type of collateral taken by the Group’s commercial and corporate

businesses and the manner in which it is taken will vary according to the

activity and assets of the customer.

xPhysical assets - these include business assets such as stock, plant

and machinery, vehicles, ships and aircraft. In general, physical

assets qualify as collateral only if they can be unambiguously

identified, located or traced, and segregated from uncharged assets.

Assets are valued on a number of bases according to the type of

security that is granted.

xReal estate - the Group takes collateral in the form of real estate,

which includes residential and commercial properties. The loan

amount will typically exceed the market value of the collateral at

origination date. The market value is defined as the estimated

amount for which the asset could be sold in an arms length

transaction by a willing seller to a willing buyer.

xReceivables - when taking a charge over receivables, the Group

assesses their nature and quality and the borrower’s management

and collection processes. The value of the receivables offered as

collateral will typically be adjusted to exclude receivables that are

past their due dates.

The security charges may be floating or fixed, with the type of security

likely to impact (i) the credit decision; and (ii) the potential loss upon

default. In the case of a general charge such as a mortgage debenture,

balance sheet information may be used as a proxy for market value if the

information is deemed reliable.

The Group does not recognise certain asset classes as collateral: for

example, short leasehold property and equity shares of the borrowing

company. Collateral whose value is correlated to that of the obligor is

assessed on a case-by-case basis and, where necessary, over-

collateralisation may be required.

The Group uses industry-standard loan and security documentation

wherever possible. Non standard documentation is typically prepared by

external lawyers on a case-by-case basis. The Group’s business and

credit teams are supported by in-house specialist documentation teams.

The existence of collateral has an impact on provisioning. Where the

Group no longer expects to recover the principal and interest due on a

loan in full or in accordance with the original terms and conditions, it is

assessed for impairment. If exposures are secured, the current net

realisable value of the collateral will be taken into account when

assessing the need for a provision. No impairment provision is

recognised in cases where all amounts due are expected to be settled in

full on realisation of the security.

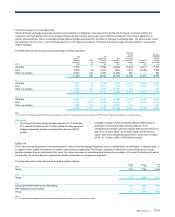

2011 2010

Corporate risk elements in lending and potential problem loans

(excluding commercial real estate) Loans

£m

Provisions

£m

Loans

£m

Provisions

£m

Secured 7,782 3,369 6,526 2,564

Unsecured 2,712 1,836 2,769 1,762

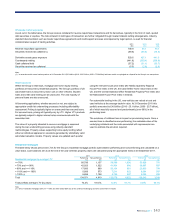

Commercial real estate

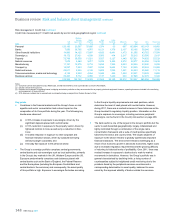

The table below analyses commercial real estate lending by loan-to-value (LTV). Due to market conditions in Ireland and to a lesser extent in the UK,

there is a shortage of market based data. In the absence of external valuations, the Group deploys a range of alternative approaches including internal

expert judgement and indexation.

Ulster Bank Rest of the Group Group

LTVs AQ1-AQ9

£m

AQ10

£m

AQ1-AQ9

£m

AQ10

£m

AQ1-AQ9

£m

AQ10

£m

2011

<= 50% 81 28 7,091 332 7,172 360

>50% and <= 70% 642 121 14,105 984 14,747 1,105

> 70% and <= 90% 788 293 10,042 1,191 10,830 1,484

>90% and <= 100% 541 483 2,616 1,679 3,157 2,162

>100% and <= 110% 261 322 1,524 1,928 1,785 2,250

> 110% and <= 130% 893 1,143 698 1,039 1,591 2,182

>130% 1,468 10,004 672 2,994 2,140 12,998

Total with LTVs 4,674 12,394 36,748 10,147 41,422 22,541

Other (1) 7 38 8,994 1,844 9,001 1,882

Total 4,681 12,432 45,742 11,991 50,423 24,423

Total portfolio average LTV (2) 140% 259% 69% 129% 77% 201%

Notes:

(1) Other performing loans of £9.0 billion include unsecured lending to commercial real estate clients, such as major UK homebuilders. The credit quality of these exposures is consistent with that of the

performing portfolio overall. Other non-performing loans of £1.9 billion are subject to the Group’s standard provisioning policies.

(2) Weighted average by exposure.

Business review Risk and balance sheet management continued