RBS 2011 Annual Report Download - page 247

Download and view the complete annual report

Please find page 247 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

RBS Group 2011 245

Pension risk*

The Group is exposed to risk from its defined benefit pension schemes to

the extent that the assets of the schemes do not fully match the timing

and amount of the schemes’ liabilities. Pension scheme liabilities vary

with changes to long-term interest rates, inflation, pensionable salaries

and the longevity of scheme members as well as changes in legislation.

The Group is exposed to the risk that the market value of the schemes’

assets, together with future returns and any additional future contributions

could be considered insufficient to meet the liabilities as they fall due. In

such circumstances, the Group could be obliged, or may choose, to make

additional contributions to the schemes.

The RBS Group Pension Fund (‘Main scheme’) is the largest of the

schemes and the main source of pension risk. The Main scheme

operates under a trust deed under which the corporate trustee, RBS

Pension Trustees Limited, is a wholly owned subsidiary of The Royal

Bank of Scotland plc and the trustee board comprises six directors

selected by the Group and four directors nominated by members.

The trustee is solely responsible for the investment of the Main scheme’s

assets which are held separately from the assets of the Group.

Significant changes to asset strategy are discussed with the Groups

Pension Risk Committee which was established in 2011. The Group and

the trustee must agree on the Main scheme funding plan.

In October 2006, the Main scheme was closed to new employees. In

November 2009, the Group confirmed that it was making changes to the

Main scheme and a number of other defined benefit schemes including

the introduction of a limit of 2% per annum (or the annual change in the

Consumer Price Index, if lower) to the amount of any salary increase that

will count for pensionable purposes.

Risk appetite and investment policy are agreed by the trustee with

quantitative and qualitative input from the scheme actuaries and

investment advisers. The trustee also consults with the Group to obtain

its view on the appropriate level of risk within the pension fund.

Risk management framework

From a sponsor perspective, the Group manages this risk using a

framework that encompasses risk reporting and monitoring, stress

testing, modelling and an associated governance structure that helps

ensure the Group is able to fulfil its obligation to support the defined

benefit pension schemes to which it has exposure.

Reporting and monitoring

The Group maintains an independent review of risk from a sponsor

perspective within its pension funds. It achieves this through underlying

regular pension risk reporting and monitoring to the Group Board, Group

Board Risk Committee and Group Risk Committee on the material

pension schemes that the Group has an obligation to support.

Stress testing and modelling

Throughout 2011, various pension risk stress testing initiatives were

undertaken, focused both on internally defined scenarios and on

scenarios undertaken to meet integrated EBA, IMF and FSA stress

testing requirements. On an annual basis, the Internal Capital Adequacy

Assessment Process is also modelled; this entails assessing changes in

pension asset and liability values over a 12-month horizon under various

stresses and scenarios.

Governance

Akey component of the pension risk framework is the Pension Risk

Committee, which was established in 2011 and has the authority to

articulate the Group’s view of risk appetite for the various RBS pension

schemes. The Pension Risk Committee also serves as a formal link

between the Group and the Trustee of the Group’s largest pension

schemes on risk management asset strategy and financing issues and,

during 2011, facilitated an agreement between the two on mechanisms

for reducing risk within the RBS Group Pension Fund.

Improvements in 2011 and next steps

As part of the continuing development of the pension risk management

framework within RBS Group, key achievements in 2011 focused on

improved stress testing and risk governance mechanisms. The

framework will continue to be developed in 2012 with improvements in

risk reporting and monitoring, modelling and stress testing capability

along with the embedding of the pension risk governance structure

implemented in 2011.

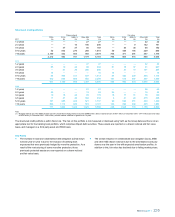

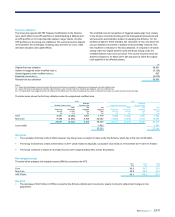

Main scheme

The most recent funding valuation, at 31 March 2010, was agreed during

2011. It showed that the value of liabilities exceeded the value of assets

by £3.5 billion at 31 March 2010, a ratio of assets to liabilities of 84%. In

order to eliminate this deficit, the Group has agreed to pay additional

contributions each year over the period 2011 to 2018. These

contributions started at £375 million per annum in 2011, increasing to

£400 million per annum in 2013 and from 2016 onwards will be further

increased in line with price inflation. Further details are given in Note 4 of

the consolidated accounts.

The assets of the Main scheme, which represent 84% of Group pension

plan assets at 31 December 2011, are invested in a diversified portfolio of

quoted and private equity, government and corporate fixed interest and

index-linked bonds, and other assets including property and hedge funds.

The trustee has taken measures to partially mitigate inflation and interest

rate risks both by investment in suitable physical assets and by entering

into inflation and interest rate swaps. The Main scheme also uses

derivatives within its portfolio to manage the allocation to asset classes

and to manage risk within asset classes.