RBS 2011 Annual Report Download - page 117

Download and view the complete annual report

Please find page 117 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

RBS Group 2011 115

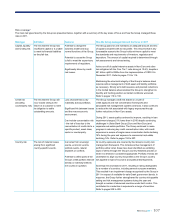

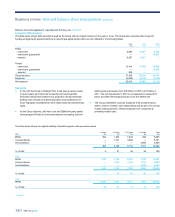

Regulatory capital impact of the APS*

Methodology

The regulatory capital requirements for assets covered by the Scheme

are calculated using the securitisation framework under the FSA

prudential rules. The calculation is as follows (the output is known as ‘the

uncapped amount’):

xFirst loss - the residual first loss, after impairments and write-downs,

to date, is deducted from available capital split equally between

Core Tier 1 and Tier 2 capital;

xHM Treasury share of covered losses - after the first loss has been

deducted, 90% of assets covered by HM Treasury are risk-weighted

at nil; and

xRBS share of covered losses - the remaining 10% share of loss is

borne by RBS and is risk-weighted in the normal way.

Should the uncapped amount be higher than the capital requirements for

the underlying assets calculated as normal, ignoring the Scheme, the

capital requirements for the Scheme are capped at the level of the

requirements for the underlying assets (‘capped amount’). Where

capped, the Group apportions the capped amount up to the level of the

first loss as calculated above; any unused capped amount after the first

loss capital deduction will be taken as RWAs for the Group’s share of

covered losses.

Adjustments to the regulatory capital calculation can be made for either

currency or maturity mismatches. These occur where there is a difference

between the currency or maturity of the protection and that of the

underlying asset. These mismatches will have an impact upon the timing

of the removal of the cap and level of regulatory capital benefit on the

uncapped amount, but this effect is not material.

Impact

The Group calculates its capital requirements in accordance with the

capped basis. Accordingly, the APS has no impact on the Pillar 1

regulatory capital requirement in respect of the assets covered by the

APS. It does, however, improve the Core Tier 1 capital ratio of the Group.

The protection afforded by the APS assists the Group in satisfying the

forward-looking stress testing framework applied by the FSA.

Future regulatory capital effects

As impairments or write-downs on the pool of assets are recognised, they

reduce Core Tier 1 capital in the normal way. This will reduce the first

loss deduction for the Scheme, potentially leading to a position where the

capital requirement on the uncapped basis would no longer, for the

assets covered by the APS, exceed the non-APS requirement and as a

result, the Group would expect to start reporting the regulatory capital

treatment on the uncapped basis.

For further information on the assets covered by APS see pages 247 to

249.

Basel III*

The rules issued by the Basel Committee on Banking Supervision

(BCBS), commonly referred to as Basel III, are a comprehensive set of

reforms designed to strengthen the regulation, supervision, risk and

liquidity management of the banking sector. In the EU they will be

enacted through a revised Capital Requirements Directive referred to as

CRD IV.

In December 2010, the BCBS issued the final text of the Basel III rules,

providing details of the global standards agreed by the Group of

Governors and Heads of Supervision, the oversight body of the BCBS

and endorsed by the G20 leaders at their November 2010 Seoul summit.

There are transition arrangements proposed for implementing these new

standards as follows:

xNational implementation of increased capital requirements will begin

on 1 January 2013;

xThere will be a phased five year implementation of new deductions

and regulatory adjustments to Core Tier 1 capital commencing on 1

January 2014;

xThe de-recognition of non-qualifying non-common Tier 1 and Tier 2

capital instruments will be phased in over 10 years from 1 January

2013; and

xRequirements for changes to minimum capital ratios, including

conservation and countercyclical buffers, as well as additional

requirements for Global Systemically Important Banks, will be

phased in from 2013 to 2019.

The Group, in conjunction with the FSA, regularly evaluates its models for

the assessment of RWAs ascribed to credit risk across various classes.

This, together with the changes introduced by CRD IV relating primarily to

counterparty risk, is expected to increase RWA requirements by the end

of 2013 by £50 billion to £65 billion. These estimates are still subject to

change; a degree of uncertainty remains around implementation details

as the guidelines are not finalised and must still be enacted into EU law.

There could be other future changes and associated impacts from these

model reviews.

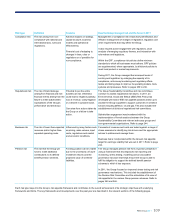

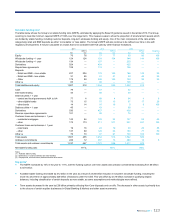

Other regulatory capital changes*

The Group is in the process of implementing changes to the RWA

requirements for commercial real estate portfolios consistent with revised

industry guidance from the FSA. This is projected to increase RWA

requirements by circa £20 billion by the end of 2013, of which circa £10

billion will apply in 2012.

The Group is managing the changes to capital requirements from new

regulation and model changes and the resulting impact on the common

equity Tier 1 ratio, focusing on risk reduction and deleveraging. This is

principally being achieved through the continued run-off and disposal of

Non-Core assets and deleveraging in GBM as the business focuses on

the most productive returns on capital.

The major categories of new deductions and regulatory adjustments

which are being phased in over a five year period from 1 January 2014

include:

xExpected loss net of provisions;

xDeferred tax assets not relating to timing differences;

xUnrealised losses on available-for-sale securities; and

xSignificant investments in non-consolidated financial institutions.

The net impact of these changes is expected to be manageable as the

aggregation of these drivers is projected to be lower by 2014 and

declining during the phase-in period.