RBS 2011 Annual Report Download - page 356

Download and view the complete annual report

Please find page 356 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

346 -

347

347 -

348

348 -

349

349 -

350

350 -

351

351 -

352

352 -

353

353 -

354

354 -

355

355 -

356

356 -

357

357 -

358

358 -

359

359 -

360

360 -

361

361 -

362

362 -

363

363 -

364

364 -

365

365 -

366

366 -

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

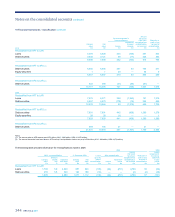

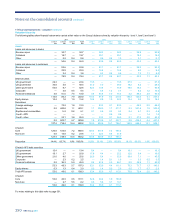

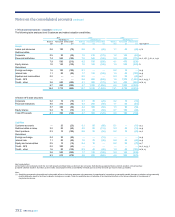

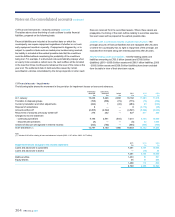

354 RBS Group 2011

11 Financial instruments - valuation continued

Modelled products

For modelled products the market convention is to quote these trades

through the model inputs or parameters as opposed to a cash price

equivalent. A mark-to-market is derived from the use of the independent

market inputs calculated using the Group’s model.

The decision to classify a modelled asset as level 2 or 3 will be

dependent upon the product/model combination, the currency, the

maturity, the observability of input parameters and other factors. All these

need to be assessed to classify the asset.

An assessment is made of each input into a model. There may be

multiple inputs into a model and each is assessed in turn for observability

and quality. If an input fails the observability or quality tests then the

instrument is considered to be in level 3 unless the input can be shown to

have an insignificant effect on the overall valuation of the product.

The majority of derivative instruments are classified as level 2 as they are

vanilla products valued using observable inputs. The valuation

uncertainty on these is considered to be low and both input and output

testing may be available. Examples of these products would be vanilla

interest rate swaps, foreign exchange swaps and liquid single name

credit derivatives.

Non-modelled products

Non-modelled products are generally quoted on a price basis and can

therefore be considered for each of the 3 levels. This is determined by

the liquidity and valuation uncertainty of the instruments which is in turn

measured from the availability of independent data used by the IPV

process.

The availability and quality of independent pricing information is

considered during the classification process. An assessment is made

regarding the quality of the independent information. For example where

consensus prices are used for non-modelled products, a key assessment

of the quality of a price is the depth of the number of prices used to

provide the consensus price. If the depth of contributors falls below a set

hurdle rate, the instrument is considered to be level 3. This hurdle rate is

consistent with the rate used in the IPV process to determine whether or

not the data is of sufficient quality to adjust the instrument’s valuations.

However, where an instrument is generally considered to be illiquid, but

regular quotes from market participants exist, these instruments may be

classified as level 2 depending on frequency of quotes, other available

pricing and whether the quotes are used as part of the IPV process or

not.

For some instruments with a wide number of available price sources,

there may be differing quality of available information and there may be a

wide range of prices from different sources. In these situations an

assessment is made as to which source is the highest quality and this will

be used to determine the classification of the asset. For example, a

tradable quote would be considered a better source than a consensus

price.

Instruments that cross levels

Some instruments will predominantly be in one level or the other, but

others may cross between levels. For example, a cross currency swap

may be between very liquid currency pairs where pricing is readily

observed in the market and will therefore be classified as level 2. The

cross currency swap may also be between two illiquid currency pairs in

which case the swap would be placed into level 3. Defining the difference

between liquid and illiquid may be based upon the number of consensus

providers the consensus price is made up from and whether the

consensus price can be supplemented by other sources.

Level 3 portfolios and sensitivity methodologies

For each of the portfolio categories shown in the tables above, there

follows a description of the types of products that comprise the portfolio

and the valuation techniques that are applied in determining fair value,

including a description of valuation techniques used for levels 2 and 3

and inputs to those models and techniques. Where reasonably possible

alternative assumptions of unobservable inputs used in models would

change the fair value of the portfolio significantly, the alternative inputs

are indicated. Where there have been significant changes to valuation

techniques during the year a discussion of the reasons for this are also

included.

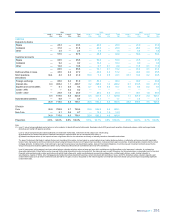

Loans and advances to customers

Loans in level 3 primarily comprise loans to emerging market

counterparties, structured loans and legacy commercial mortgages.

Commercial mortgages

These senior and mezzanine commercial mortgages are loans secured

on commercial land and buildings that were originated or acquired by the

Group for securitisation. Senior commercial mortgages carry a variable

interest rate and mezzanine or more junior commercial mortgages may

carry a fixed or variable interest rate. Factors affecting the value of these

loans may include, but are not limited to, loan type, underlying property

type and geographic location, loan interest rate, loan to value ratios, debt

service coverage ratios, prepayment rates, cumulative loan loss

information, yields, investor demand, market volatility since the last

securitisation andcredit enhancement. Where observable market prices

for a particular loan are not available, the fair value will typically be

determined with reference to observable market transactions in other

loans or credit related products including debt securities and credit

derivatives. Assumptions are made about the relationship between the

loan and the available benchmark data.

Notes on the consolidated accounts continued