RBS 2011 Annual Report Download - page 119

Download and view the complete annual report

Please find page 119 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

RBS Group 2011 117

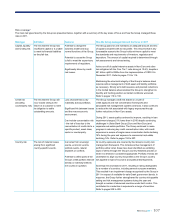

Stress testing

The strength of a bank’s liquidity risk management can only be evaluated

based on its ability to survive under stress. The Group evaluates the

survivability of the major legal entities and legal entity groups when

subjected to simulated stress conditions.

Simulated liquidity stress testing is periodically performed for each

business as well as the major operating subsidiaries. A variety of firm-

specific and market-related scenarios are used at the consolidated level

and in individual countries. These scenarios include assumptions about

significant changes in key funding sources, credit ratings, contingent uses

of funding, and political and economic conditions in certain countries.

The Group’s actual experiences from the 2008 and 2009 period factor

heavily into the liquidity analysis. This systemic and name-specific crisis

provides important data points in estimating stress severity.

Stress scenarios are applied to both on-balance sheet and off-balance

sheet commitments, to provide a comprehensive view of potential cash

flows.

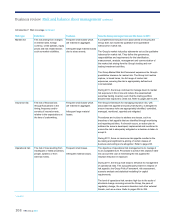

Contingency planning

The Group has a Contingency Funding Plan (CFP), which is updated as

the balance sheet evolves. The CFP is linked to stress test results and

forms the foundation for liquidity risk limits. Limits in the business-as-

usual environment are bounded by capacity to satisfy the Group’s

liquidity needs in the stress environments. The CFP provides a detailed

description of the availability, size and timing of all sources of contingent

liquidity available to the Group in a stress event. These are ranked in

order of economic impact and effectiveness to meet the anticipated

stress requirement. The CFP includes documented procedures and sign-

offs for actions that may require businesses to provide access to

customer assets for collateralised borrowing, securitisation or sale. Roles

and responsibilities for the effective implementation of the CFP are also

documented.

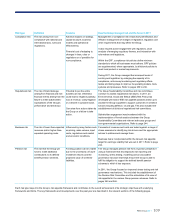

Liquidity reserves

The Group maintains liquidity reserves sufficient to satisfy cash

requirements, in the event of a severe disruption in its access to funding

sources. The reserves consist of cash held on deposit at central banks,

high quality unencumbered government securities and other

unencumbered collateral. Government securities vary by type and

jurisdiction based on local regulatory considerations. The currency mix of

the reserves reflects the underlying balance sheet composition.

Regulatory oversight

The Group operates in multiple jurisdictions and is subject to a number of

regulatory regimes.

The Group’s lead regulator is the UK Financial Services Authority (FSA).

The FSA implemented a new liquidity regime on 1 June 2010. The new

rules provide a standardised approach applied to all UK banks. At RBS

Group, the rules focus on the UK Defined Liquidity Group (a subset

comprising the Group’s five UK banks, The Royal Bank of Scotland plc,

National Westminster Bank Plc, Ulster Bank Limited, Coutts & Co and

Adam & Co) and cover adequacy of liquidity resources, controls, stress

testing and the Individual Liquidity Adequacy Assessment (ILAA). The

ILAA informs the Group Board and the FSA of the assessment and

quantification of the Group’s liquidity risks and their mitigation, and how

much current and future liquidity is required.

In the US, the Group’s operations must meet liquidity requirements set

out by the US Federal Reserve Bank, the Office of the Comptroller of the

Currency, the Federal Deposit Insurance Corporation and the Financial

Industry Regulatory Authority. In the Netherlands, the Group is subject to

the De Nederlandsche Bank liquidity oversight regime.

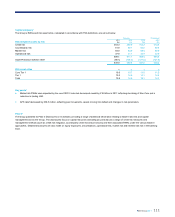

Regulatory developments*

There have been a number of significant developments in the regulation

of liquidity risk.

In December 2010, the Basel Committee on Banking Supervision issued

the ‘International framework for liquidity risk measurement, standards and

monitoring’ which confirmed the introduction of two liquidity ratios: the

liquidity coverage ratio (LCR) and the net stable funding ratio (NSFR).

The introduction of both of these ratios will be subject to an observation

period, which includes review clauses to identify and address any

unintended consequences.

After an observation period beginning in 2011, the LCR, including any

revisions, will be introduced on 1 January 2015. The NSFR, including any

revisions, will move to a minimum standard by 1 January 2018.