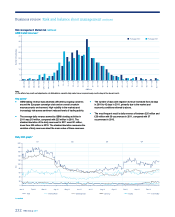

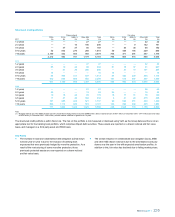

RBS 2011 Annual Report Download - page 243

Download and view the complete annual report

Please find page 243 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

RBS Group 2011 241

Prudential and related reforms

Akey focus during 2011 was work on amending the EU’s Capital

Requirements Directive (CRD): a key step in that process was the

publication of draft legislative text in September 2011, the CRD IV

package, which is expected to be finalised during 2012 and will

implement Basel III in the EU.

Another key area of work was the EU’s “crisis management” legislative

package, aimed at dealing with issues similar to those addressed by the

FSB work on G-SIFIs. An early 2011 EU Commission consultation

included proposals on enhanced supervision and early powers of

intervention; recovery and resolution planning; resolution frameworks;

resolution funds and debt write-down (but not capital surcharges). Draft

legislation to implement these measures was at the time of writing

expected to be issued in early 2012, after several postponements.

Other initiatives in the prudential space have included, notably, continued

work on developing the Solvency II framework for insurers; the

development of legislative proposals on corporate governance in financial

institutions; and the further development and UK implementation of the

EU’s common reporting framework (COREP) for banks.

Market and structural reforms

Key developments in this space included:

xEuropean Markets Infrastructure Regulation (EMIR) - negotiations

continued during 2011 on this draft Regulation on OTC derivatives,

central counterparties and trade repositories, which represents a

major element of the financial crisis regulatory response agenda.

Agreement was close to being reached in early 2012.

xMarkets in Financial Instruments Directive Review (MiFID2) - the EU

review of this directive, which sets the framework for investment

markets, culminated in the publication of draft legislative text in

October 2011.

xFinancial Transaction Tax (FTT) - the EU Commission published

proposals for an FTT, which would see trades in bonds and shares

taxed at 0.1% and complex derivatives taxed at 0.01%. However,

the proposal requires approval from all 27 EU members, but is

opposed by some, including notably the UK, which reduces the

likelihood of it being imposed.

xOther initiatives - these have included changes to the market abuse

regime and prospectus requirements, initiatives on short-selling,

further legislative developments impacting credit rating agencies and

changes to depositor and investor protection.

EU retail market reforms

Notwithstanding the focus on prudential and market reforms in response

to the financial crisis, the EU Commission during 2011 also continued to

work on a wide range of retail agenda initiatives. These included a draft

legislative proposal for a mortgage credit directive, with a focus on

responsible lending and borrowing; the development of proposals on

collective redress; and ongoing discussions with the banking industry to

improve the transparency and comparability of bank fees. The Group also

continued to work on implementing the requirements coming into force at

the end of 2011, contained in the EU Payment Services Directive.

UK regulatory developments

UK regulatory developments during 2011 continued to be extensively

determined by global and EU developments, with UK regulators working

to implement requirements coming into force, such as the CRD III

package of reforms, and actively participating in policy development at

the EU and global levels. In addition, there were a number of

developments specific to the UK.

Independent Commission on Banking (ICB)

The ICB was appointed by the UK Government in June 2010 to review

possible structural measures to reform the UK banking system in order to

promote, amongst other things, stability and competition. It published its

final report to the Cabinet Committee on Banking Reform on 12

September 2011 (the ‘Final Report’), which set out the ICB’s views on

possible reforms to improve stability and competition in UK banking.

The Final Report made a number of recommendations, including in

relation to: (i) the implementation of a ring-fence of retail banking

operations; (ii) increased loss-absorbency (including bail-in, i.e. the ability

to write-down debt or convert it into an issuer’s ordinary shares in certain

circumstances); and (iii) promotion of competition.

On 19 December 2011, the UK Government published its response to the

Final Report and indicated its support and intention to implement the

recommendations set out in the Final Report substantially as proposed.

The Government indicated that it would work towards putting in place the

necessary legislation by May 2015, requiring compliance as soon as

practicable thereafter and a final deadline for full implementation of 2019.

The Group will continue to participate in the debate and to consult with

the UK Government on the implementation of the recommendations set

out in the Final Report and in the Government’s response.

Regulatory architecture reforms

Work on the UK coalition government’s plans for reforming the UK’s

regulatory structure continued during 2011, with major consultations from

HM Treasury, a number of calls for evidence from parliamentary

committees and the publication of a draft Bill for pre-legislative scrutiny

purposes in June 2011. In addition, the FSA and Bank of England

published policy documents setting out initial high-level policy thinking on

the new regulatory bodies; and an interim version of the Financial Policy

Committee started to meet in advance of legislation being enacted.

However, the timescale for completing the legislative process and fully

implementing the new framework has been delayed until 2013 (from the

end of 2012).