RBS 2011 Annual Report Download - page 349

Download and view the complete annual report

Please find page 349 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

339 -

340

340 -

341

341 -

342

342 -

343

343 -

344

344 -

345

345 -

346

346 -

347

347 -

348

348 -

349

349 -

350

350 -

351

351 -

352

352 -

353

353 -

354

354 -

355

355 -

356

356 -

357

357 -

358

358 -

359

359 -

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

RBS Group 2011 347

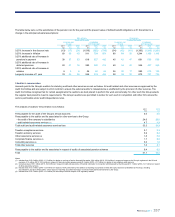

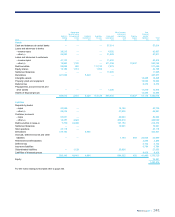

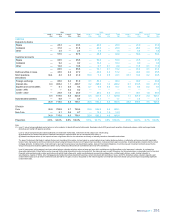

Valuation reserves

When valuing financial instruments in the trading book, adjustments are made to mid-market valuations to cover bid-offer spread, liquidity and credit

risk. The following table shows the valuation reserves and adjustments.

2011

£m

2010

£m

2009

£m

Credit valuation adjustments

Monoline insurers 1,198 2,443 3,796

Credit derivative product companies 1,034 490 499

Other counterparties 2,254 1,714 1,588

4,486 4,647 5,883

Bid-offer, liquidity and other reserves 2,704 2,797 2,814

7,190 7,444 8,697

Key points

xThe exposure to monolines reduced primarily due to the

restructuring of some exposures, partially offset by lower prices of

underlying reference instruments. The credit valuation adjustments

decreased due to the reduction in exposure partially offset by wider

credit spreads.

xThe exposure to credit derivative product companies has increased,

primarily driven by wider credit spreads of the underlying reference

loans and bonds. The credit valuation adjustments increased in line

with the increase in exposure.

Credit valuation adjustments (CVA)

Credit valuation adjustments represent an estimate of the adjustment to

fair value that a market participant would make to incorporate the credit

risk inherent in counterparty derivative exposures.

Monoline insurers

The Group has purchased protection from monoline insurers

(“monolines”), mainly against specific Asset-backed securities. Monolines

specialise in providing credit protection against the principal and interest

cash flows due to the holders of debt instruments in the event of default

by the debt instrument counterparty. This protection is typically held in the

form of derivatives such as credit default swaps (CDSs) referencing

underlying exposures held directly or synthetically by the Group.

The gross mark-to-market of the monoline protection depends on the

value of the instruments against which protection has been bought. A

positive fair value, or a valuation gain, in the protection is recognised if

the fair value of the instrument it references decreases. For the majority

of trades the gross mark-to-market of the monoline protection is

determined directly from the fair value price of the underlying reference

instrument However, for the remainder of the trades the gross mark-to-

market is determined using industry standard models.

The methodology employed to calculate the monoline CVA uses market

implied probability of defaults and internally assessed recovery levels to

determine the level of expected loss on monoline exposures of different

maturities. The probability of default is calculated with reference to

market observable credit spreads and recovery levels. CVA is calculated

at a trade level by applying the expected loss corresponding to each

trade’s expected maturity, to the gross mark-to-market of the monoline

protection. The expected maturity of each trade reflects the scheduled

notional amortisation of the underlying reference instruments and

whether payments due from the monoline are received at the point of

default or over the life of the underlying reference instruments.

Credit derivative product companies (CDPC)

ACDPC is a company that sells protection on credit derivatives. CDPCs

are similar to monoline insurers however, they are not regulated as

insurers.

The Group has purchased credit protection from CDPCs through

tranched and single name credit derivatives. The Group's exposure to

CDPCs is predominantly due to tranched credit derivatives (“tranches”). A

tranche references a portfolio of loans and bonds and provides protection

against total portfolio default losses exceeding a certain percentage of

the portfolio notional (the attachment point) up to another percentage (the

detachment point).

The Group has predominantly traded senior tranches with CDPCs, the

average attachment and detachment points are 13% and 47%

respectively (2010 - 13% and 49%; 2009 - 15% and 51%), and the

majority of the loans and bonds in the reference portfolios are investment

grade.

The gross mark-to-market of the CDPC protection is determined using

industry standard models. The methodology employed to calculate the

CDPC CVA is different to that outlined above for monolines, as there are

no market observable credit spreads and recovery levels for these

entities. The level of expected loss on CDPC exposures is estimated with

reference to recent market events impacting CDPCs (including

communication activity); risk mitigation strategies (including analysing the

underlying trades and the cost of hedging expected default losses in

excess of the available capital); and the total notional of trades transacted

by each CDPC together with the level of resources available to settle

default payments.

.