RBS 2011 Annual Report Download - page 139

Download and view the complete annual report

Please find page 139 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

RBS Group 2011 137

At 31 December 2011, exposure to customers reported as Watchlist Red

and managed within the divisions totalled £4.9 billion.

Strategies that are available within divisions include granting the

customer various types of concessions. Any decision to approve a

concession will be a function of the division’s specific country and sector

appetite, the key credit metrics of the customer, the market environment

and the loan structure/security. Only those concessions deemed to be

outside current market norms are reported as restructurings in the

discussions below.

Other potential outcomes of the review of the relationship are to: take the

customer off Watchlist and return it to the mainstream loan book; offer

further lending and maintain ongoing review; transfer the relationship to

the GRG for those customers requiring such stewardship; or exit the

relationship altogether.

Global Restructuring Group

In cases where the Group’s exposure to the customer exceeds £1 million,

the relationship may be transferred to the GRG following consultation

with the originating division. The GRG’s primary function is active

management of the exposures to minimise loss for the Group and where

feasible return the exposure to the Group’s mainstream loan book

following an assessment by the GRG that no further losses are expected.

At 31 December 2011, credit risk assets relating to exposures under

GRG management (excluding those placed under GRG stewardship for

operational reasons rather than concerns over credit quality and those in

the AQ10 internal asset quality (AQ) band) totalled £22 billion. Credit risk

assets are defined on page 144. The internal asset quality bands are

defined on page 145.

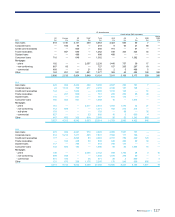

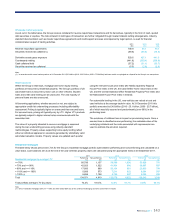

The following table shows a sector breakdown of these exposures:

Watchlist Red credit risk assets under GRG management Core

£m

Non-Core

£m

Total

£m

2011

Property 6,561 6,011 12,572

Transport 1,159 2,252 3,411

Retail and leisure 1,528 669 2,197

Services 808 141 949

Other 1,952 916 2,868

Total 12,008 9,989 21,997

Types of wholesale restructurings

Anumber of options are available to the Group when corrective action is

deemed necessary. The Group may offer a temporary covenant waiver, a

recalibration of covenants and/or an amendment of restrictive covenants

to mitigate a potential or actual covenant breach. Such relief is usually

granted in exchange for fees, increased margin, additional security, or a

reduction in maturity profile of the original loan. Such covenant-related

concessions are not included in the quantitative loan restructuring

disclosures below.

The reported restructurings comprise the following types of concessions:

xVariation in margin - the contractual margin may be amended to

bolster the customer’s day-to-day liquidity, with the aim of helping to

sustain the customer’s business as a going concern. This would

normally be seen as a short-term solution and is typically

accompanied by the Group receiving an exit payment, a payment in

kind or a deferred fee.

xPayment holidays and loan rescheduling - payment holidays or

changes to the contracted amortisation profile including extensions

in contracted maturity or roll-overs may be granted to improve the

customer’s liquidity. Such concessions often depend on the

expectation that the customer’s liquidity will recover when market

conditions improve or will benefit from access to alternative sources

of liquidity, e.g. an issue of equity capital. Recently, these types of

concessions have become more common in commercial real estate

transactions, particularly where a shortage of market liquidity rules

out immediate refinancing and makes short-term forced collateral

sales unattractive.

xForgiveness of all or part of the outstanding debt - debt may be

forgiven or exchanged for equity in cases where a fundamental shift

in the customer’s business or economic environment means that the

customer is incapable of servicing current debt obligations and other

forms of restructuring are unlikely to succeed in isolation. Debt

forgiveness is often an element in leveraged finance transactions,

which are typically structured on the basis of projected cash flows

from operational activities, rather than underlying tangible asset

values. Provided that the underlying business model and strategy

are considered viable, maintaining the business as a going concern

with a sustainable level of debt is the preferred option, rather than

realising the value of the underlying assets.

The vast majority of the restructurings reported by the Group take place

within the GRG. Forgiveness of debt and exchange for equity is only

available to customers in the GRG.