RBS 2011 Annual Report Download - page 478

Download and view the complete annual report

Please find page 478 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

468 -

469

469 -

470

470 -

471

471 -

472

472 -

473

473 -

474

474 -

475

475 -

476

476 -

477

477 -

478

478 -

479

479 -

480

480 -

481

481 -

482

482 -

483

483 -

484

484 -

485

485 -

486

486 -

487

487 -

488

488 -

489

-

490

|

|

476 RBS Group 2011

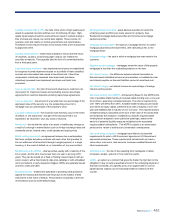

Glossary of terms

Adjustable rate mortgage (ARM) - in the US, a variable-rate mortgage.

ARMs include: hybrid ARMs which typically have a fixed-rate period

followed by an adjustable-rate period; interest-only ARMs where interest

only is payable for a specified number of years, typically for three to ten

years; and payment-option ARMs that allow the borrower to choose

periodically between various payment options.

Alt-A (Alternative A-paper) - a US description for mortgage loans with a

higher credit quality than sub-prime loans but with features that disqualify

the borrower from a traditional prime loan. Alt-A lending characteristics

include limited documentation; high loan-to-value ratio; secured on non-

owner occupied properties; and debt-to-income ratio above normal limits.

Arrears - the aggregate of contractual payments due on a debt that have

not been met by the borrower. A loan or other financial asset is said to be

'in arrears' when payments have not been made. When a customer is in

arrears, the entire outstanding balance is said to be delinquent (see

Delinquency).

Asset-backed commercial paper (ABCP) - a form of asset-backed

security generally issued by a commercial paper conduit.

Asset-backed securities (ABS) - securities that represent interests in

specific portfolios of assets. They are issued by a special purpose entity

following a securitisation. The underlying portfolios commonly comprise

residential or commercial mortgages but can include any class of asset

that yields predictable cash flows. Payments on the securities depend

primarily on the cash flows generated by the assets in the underlying pool

and other rights designed to assure timely payment, such as guarantees

or other credit enhancements. Collateralised bond obligations,

collateralised debt obligations, collateralised loan obligations, commercial

mortgage backed securities and residential mortgage backed securities

are all types of ABS.

Asset protection scheme credit default swap - in 2009, the Group became

party to the Asset Protection Scheme under which it purchased credit

protection over a portfolio of specified assets and exposures (“covered

assets”) from Her Majesty’s Treasury acting on behalf of the UK

Government. The contract is accounted for as a derivative financial

instrument. It is recognised at fair value and included in Derivatives on

the balance sheet. Changes in its fair value are recognised in profit or

loss within Income from trading activities.

Assets under management - assets managed by the Group on behalf of

clients.

Bank levy - a levy that applies to certain UK banks, building societies and

the UK operations of foreign banks from 1 January 2011. The levy is

payable based on a percentage of the chargeable equity and liabilities of

the bank as at the balance sheet date.

Basel II -the capital adequacy framework issued by the Basel Committee

on Banking Supervision in June 2006 in the form of the ‘International

Convergence of Capital Measurement and Capital Standards’.

Basel III - in December 2010, the Basel Committee on Banking

Supervision issued final rules: ‘Basel III: A global regulatory framework

for more resilient banks and banking systems’ and ‘Basel III: International

framework for liquidity risk measurement, standards and monitoring’.

These strengthened global regulatory standards on bank capital

adequacy and liquidity and will be phased in from 2013 with full

implementation by 1 January 2019.

Basis point - one hundredth of a per cent i.e. 0.01 per cent. 100 basis

points is 1 per cent. Used when quoting movements in interest rates or

yields on securities.

Certificates of deposit (CDs) - bearer negotiable instruments

acknowledging the receipt of a fixed term deposit at a specified interest

rate.

Collateralised bond obligations (CBOs) - asset-backed securities for

which the underlying asset portfolios are bonds, some of which may be

sub-investment grade.

Collateralised debt obligations (CDOs) - asset-backed securities for

which the underlying asset portfolios are debt obligations: either bonds

(collateralised bond obligations) or loans (collateralised loan obligations)

or both. The credit exposure underlying synthetic CDOs derives from

credit default swaps. The CDOs issued by an individual vehicle are

usually divided in different tranches: senior tranches (rated AAA),

mezzanine tranches (AA to BB), and equity tranches (unrated). Losses

are borne first by the equity securities, next by the junior securities, and

finally by the senior securities; junior tranches offer higher coupons

(interest payments) to compensate for their increased risk.

Collateralised debt obligation squared (CDO-squared) - a type of

collateralised debt obligation where the underlying asset portfolio

includes tranches of other CDOs.

Collateralised loan obligations (CLOs) - asset-backed securities for which

the underlying asset portfolios are loans, often leveraged loans.

Collectively assessed loan impairment provisions - impairment loss

provisions in respect of impaired loans, such as credit cards or personal

loans, that are below individual assessment thresholds. Such provisions

are established on a portfolio basis, taking account of the level of arrears,

security, past loss experience, credit scores and defaults based on

portfolio trends.

Commercial mortgage backed securities (CMBS) -asset-backed

securities for which the underlying asset portfolios are loans secured on

commercial real estate.

Commercial paper (CP) - unsecured obligations issued by a corporate or

abank directly or secured obligations (asset-backed CP), often issued

through a commercial paper conduit, to fund working capital. Maturities

typically range from two to 270 days. However, the depth and reliability of

some CP markets means that issuers can repeatedly roll over CP

issuance and effectively achieve longer term funding. CP is issued in a

wide range of denominations and can be either discounted or interest-

bearing.

Shareholder information continued