RBS 2011 Annual Report Download - page 136

Download and view the complete annual report

Please find page 136 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

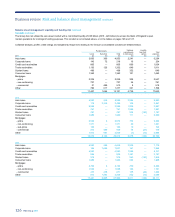

134 RBS Group 2011

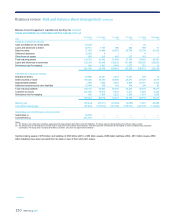

Business review Risk and balance sheet management continued

Risk management

Introduction

This section focuses on each of the key types of risk that RBS Group

faces - explaining how the Group manages these risks and highlighting

the enhancements made as a result of progress under the Group’s

ongoing initiatives to strengthen its approach to risk management.

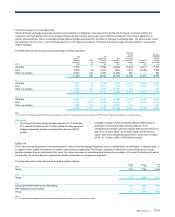

Credit risk

All the disclosures in this section (pages 134 to 160) are audited unless

otherwise indicated by an asterisk (*).

Credit risk is the risk of financial loss owing to the failure of a customer to

meet its obligation to settle outstanding amounts. The quantum and

nature of credit risk assumed across the Group’s different businesses

vary considerably, while the overall credit risk outcome usually exhibits a

high degree of correlation with the macroeconomic environment.

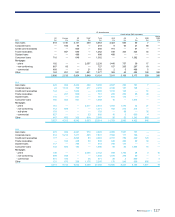

Organisation

The existence of a strong credit risk management function is vital to

support the ongoing profitability of the Group. The potential for loss

through economic cycles is mitigated through the embedding of a robust

credit risk culture within the business units and through a focus on the

importance of sustainable lending practices. The role of the credit risk

management function is to own the credit approval, concentration and

credit risk control frameworks and to act as the ultimate authority for the

approval of credit. This, together with strong independent oversight and

challenge, enables the business to maintain a sound lending environment

within risk appetite.

Responsibility for development of Group-wide policies, credit risk

frameworks, Group-wide portfolio management and assessment of

provision adequacy, sits within the Group Credit Risk (GCR) function

under the management of the Group Chief Credit Officer. Execution of

these policies and frameworks is the responsibility of the risk

management functions, located within the Group’s business divisions.

These divisional credit risk functions work together with GCR to ensure

that the Group Board’s expressed risk appetite is met, within a clearly

defined and managed control environment. The credit risk function within

each division is managed by a Chief Credit Officer, who reports jointly to

adivisional Chief Risk Officer and to the Group Chief Credit Officer.

Divisional activities within credit risk include credit approval, transaction

and portfolio analysis, early problem recognition and ongoing credit risk

stewardship.

GCR is additionally responsible for verifying compliance by the divisions

with all Group credit policies.

In the final quarter of 2011, the Executive Risk Forum (ERF) approved a

change to the management of the credit portfolio, delegating greater

authority to the Group Chief Credit Officer as chair of the functional credit

committees that analyse and recommend the limits to the ERF. With

effect from October 2011, the Group Chief Credit Officer chairs a single

Credit Risk Committee, with the authority to approve limits for the majority

of portfolios across the Group. The ERF retains its strategic role as the

most senior risk committee outside the Group Board and will continue to

approve material portfolio concentrations and higher risk portfolios such

as commercial real estate. This change strengthens individual

accountability across the risk organisation and encourages the

engagement of business leaders in first line of defence risk activity.

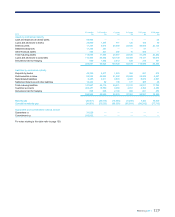

Risk appetite

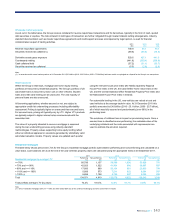

Credit concentration risk is managed and controlled through a series of

frameworks designed to limit concentration by product/asset class,

sector, single name and country. These are supported by a suite of

Group-wide and divisional policies, setting out the risk parameters within

which business units may operate. Information on the Group’s credit

portfolios is reported to the Group Board by way of the divisional and

Group-level risk committees.

Throughout 2011, GCR’s emphasis was on embedding the new risk

management frameworks introduced in 2009 and 2010 and on ensuring

alignment with the strategic risk objectives being pursued across the

Group. Risk appetite has been expressed by the Group Board by

reference to earnings volatility and stable capital and these principles

underpin the frameworks that GCR has established, and is continuing to

refine, to manage the Group’s concentration risks in the Core balance

sheet, by product/asset class, sector, single name and country.

In the two years since the new concentration framework was rolled out

across the Group, the ERF has reviewed all material industry and product

portfolios and agreed a risk appetite commensurate with the franchises

represented in these reviews. In particular, limits have been reviewed and

re-sized, to refine the Group’s risk appetite in areas where it faces

significant balance sheet concentrations or franchise challenges. The

product/asset class, sector, single name and country limits are now firmly

embedded in the risk management processes of the Group and form a

pivotal part of the Risk function’s engagement with the businesses on the

appropriateness of risk appetite choices.

The new sector and asset class limits have been informed by the work

undertaken to stress the portfolios and historical loss experience. In

addition, they factor in the future consequences for risk and return in

asset classes likely to be affected by the introduction of new regulatory

capital rules under Basel III.

*unaudited