RBS 2011 Annual Report Download - page 212

Download and view the complete annual report

Please find page 212 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

210 RBS Group 2011

Risk management: Country risk continued

Monitoring, management and mitigation* continued

Going forward, the Group continues to extend country limit control to

other countries within and outside the eurozone and will continue to

manage medium-term exposure closer to its medium-term benchmark

ratios. In addition, work is continuing on the determination of actual

appetite per country, on the country risk reporting systems and their

integration with credit, treasury and finance systems, on the

representation of country risk aspects in rating models, economic capital

models and integrated stress testing, and on the combination with actual

and expected returns. All of this should help RBS determine and steer its

risk profile and further optimise the Group’s global portfolio management.

Credit default swap (CDS) contracts are used for a number of purposes

such as hedging of the credit trading portfolio, management of

counterparty credit exposure and the mitigation of wrong-way risk. The

Group generally uses CDS contracts to manage exposure on a portfolio

rather than specific exposures. This may give rise to maturity mismatches

between the underlying exposure and the CDS contract as well as

between bought and sold CDS contracts on the same reference entity.

The terms of the Group’s CDS contracts are covered by standard ISDA

documentation, which determines if a contract is triggered due to a credit

event. Such events may include bankruptcy or restructuring of the

reference entity or a failure of the reference entity to repay its debt or

interest. Under the terms of a CDS contract, one of the regional ISDA

Credit Derivatives Determinations Committees is empowered to decide

whether or not a credit event has occurred.

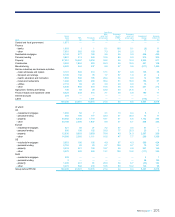

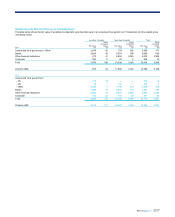

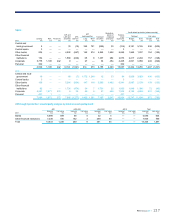

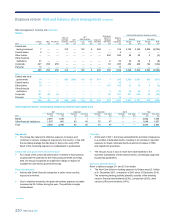

Country risk analysis

All the data tables and related definitions in this section are audited.

The following tables show the Group’s exposure by country of

incorporation of the counterparty at 31 December 2011. Countries shown

are those where the Group’s balance sheet exposure to counterparties

incorporated in the country exceeded £1 billion and the country had an

external rating of A+ or below from S&P, Moody’s or Fitch at 31

December 2011, as well as selected eurozone countries. The numbers

are stated before taking into account the impact of mitigating action, such

as collateral, insurance or guarantees that may have been taken to

reduce or eliminate exposure to country risk events. Exposures relating to

ocean-going vessels are not included due to their multinational nature.

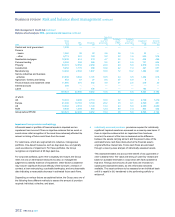

The following definitions apply to the tables and key points on pages 211

to 228:

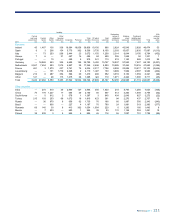

Lending comprises gross loans and advances to: central and local

governments; central banks, including cash balances; other banks and

financial institutions, incorporating overdraft and other short-term credit

lines; corporations, in large part loans and leases; and individuals,

comprising mortgages, personal loans and credit card balances. Lending

includes impaired loans and loans where an impairment event has taken

place, but the impairment provision is recognised.

Debt securities comprise securities classified as available-for-sale (AFS),

loans and receivables (LAR), held-for-trading (HFT) and designated as at

fair value through profit or loss (DFV). All debt securities other than LAR

securities are carried at fair value with LAR debt securities are carried at

amortised cost less impairment. HFT debt securities are presented as

gross long positions (including DFV securities) and short positions per

country. Impairment losses and exchange differences relating to AFS

debt securities, together with interest, are recognised in the income

statement; other changes in the fair value of AFS securities are reported

within AFS reserves, which are presented gross of tax.

Derivatives comprise the mark-to-market (mtm) value of such contracts

after the effect of enforceable netting agreements, but gross of collateral.

Reverse repurchase agreements (repos) comprise the mtm value of

counterparty exposure arising from repo transactions net of collateral.

Balance sheet exposures comprise lending exposures, debt securities

and derivatives, and repo exposures.

Contingent liabilities and commitments comprise contingent liabilities,

including guarantees and committed undrawn facilities.

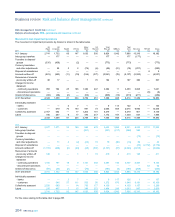

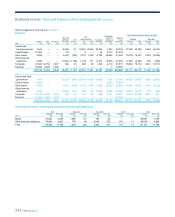

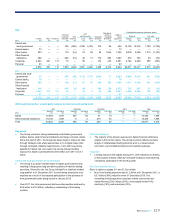

Credit default swap (CDS) under CDS contract the credit risk on the

reference entity is transferred from the buyer to the seller. The fair value,

or mtm, represents the balance sheet carrying value. The mtm value of

CDSs is included within derivatives against the counterparty of the trade,

as opposed to the reference entity. The notional is the par amount of the

credit protection bought or sold and is included against the reference

entity of the CDS contract.

The column CDS notional less fair value represents the notional less fair

value amounts arising from sold positions netted against those arising

from bought positions, and represents the net change in exposure for a

given reference entity should the CDS contract be triggered by a credit

event, assuming there is a zero recovery rate. However, in most cases,

the Group expects the recovery rate to be greater than zero and the

exposure change to be less than this amount.

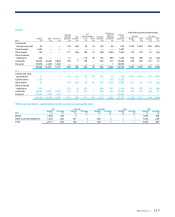

The Group primarily transacts CDS contracts with investment-grade

global financial institutions who are active participants in the CDS market.

These transactions are subject to regular margining. For European

peripheral sovereigns, credit protection has been purchased from a

number of major European banks, predominantly outside the country of

the reference entity. In a few cases where protection was bought from

banks in the country of the reference entity, giving rise to wrong-way risk,

this risk is mitigated through specific collateralisation. Due to their

bespoke nature, exposures relating to CDPCs and related hedges have

not been included, as they cannot be meaningfully attributed to a

particular country or a reference entity. Exposures to CDPCs are

disclosed on page 190.

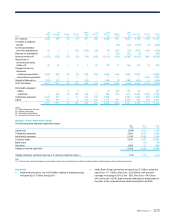

The Group used CDS contracts throughout 2011 to manage both

eurozone country and counterparty exposures. As shown in the individual

country tables, this resulted in increases in both gross notional bought

and sold eurozone CDS contracts, mainly on Italy, France and the

Netherlands. The magnitude of the fair value of bought and sold CDS

contracts increased over 2011 in line with the widening of eurozone CDS

spreads.

‘Other eurozone’ comprises Austria, Cyprus, Estonia, Finland, Malta,

Slovakia and Slovenia.

*unaudited

Business review Risk and balance sheet management continued