RBS 2011 Annual Report Download - page 151

Download and view the complete annual report

Please find page 151 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

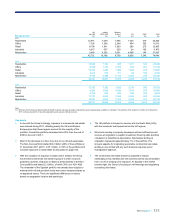

RBS Group 2011 149

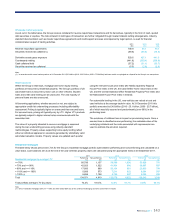

xThe other financial institutions sector comprises traded and non-

traded products and is spread across a wide range of financial

companies including insurance companies, securitisation vehicles,

financial intermediaries including central counterparties (CCPs),

financial guarantors - monolines and credit derivative product

companies (CDPCs) - and unleveraged, hedge and leveraged funds.

The size and asset quality of this portfolio are stable and have not

changed materially since 2010. However, entities in this sector

remain vulnerable to market shocks or contagion from the banking

sector crisis. Credit risk for these sectors is managed through both

the sector concentration and asset and product class frameworks,

with specific sector and product caps introduced where there is a

perception of heightened credit risk, such as with leveraged funds

and insurance holding companies. Additionally, policies were

tightened for riskier products to entities in this portfolio, such as

committed lending, to reduce risks from a customer default. During

the year, a comprehensive securitisation framework was established

to cap the securitisation portfolio and to control concentrations to the

underlying asset classes and originators. The Group is currently

reassessing its risk appetite framework for CCPs to reflect increases

in activity with these entities, as a result of regulatory requirements

for derivatives to be cleared through CCPs. In 2011, the Group

continued to manage down its exposures to monolines and CDPCs

and was successful in commuting trades with entities in this portfolio.

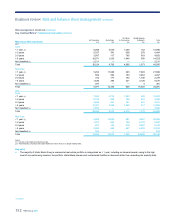

xThe Group’s exposure to the property sector totals £102 billion (a

reduction of 10% during the year), the majority of which is

commercial real estate (refer to page 150 for further detail). The

remainder comprises lending to construction companies, housing

associations and building material companies. The majority of

property exposure (with the exception of Non-Core) is within UK

Corporate (63%). Asset quality in other property sub-sectors

remained stable during the year and whilst there are some material

single name concentrations in the construction sector due to

industry consolidation, overall appetite remains controlled through

the sector concentration limits framework.

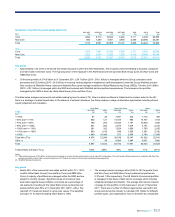

xThe exposure to the retail sector attracts heightened scrutiny due to

its cyclical nature. Stress testing has confirmed that the retail sector

has an above average vulnerability to a high UK inflation and

interest rate scenario. Certain sub-sectors have proven less

vulnerable to macroeconomic volatilities (e.g. food and beverage) as

have larger retailers with well established brands and multiple

channel offerings. Total exposure declined 6% during 2011. Despite

recent high profile failures of UK high street retailers, loss

experience on the RBS retail portfolio over 2011 was low, following

the earlier exit from some parts of the portfolio. The portfolio is

generally well diversified by geography and by counterparty.

xThe leisure sector displays weaker credit metrics than the wider

corporate portfolio, in line with the industry trend. Default experience

in hotels and restaurants is particularly high. The Group’s risk

appetite towards the sector is driven by the importance of the leisure

sector to the UK franchise, especially for the UK Corporate division,

but is mitigated through tighter origination policies and guidelines

and a reduction in exposure to high risk sub-sectors. The gaming

sub-sector is subject to specific controls due to its inherent high

credit and reputational risk profile.

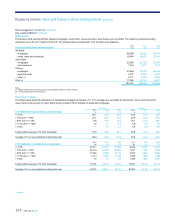

xThe Group’s transport sector includes £11.7 billion of asset-backed

exposure to ocean-going vessels. The downturn observed in the

shipping sector since 2008 continued during 2011, with further

pressure on second-hand values and deliveries of new build vessels

into poor markets. A key protection for the Group is the minimum

security covenant. This covenant is tested each quarter on an

individual vessel basis to ensure that prompt remedial action is

taken if values fall significantly below agreed loan coverage ratios.

At 31 December 2011, 1% of the Group’s exposure to this sector

was in Watchlist Red.

xExposure to the healthcare and education sectors is included in the

business services sector and totalled £13.4 billion at year-end. It is

mostly UK focused and is heavily biased towards the health sector,

which represents 74% of the exposure. The sector has performed

well despite the difficult economic conditions but there are

continuing uncertainties over the impact of Government spending

reductions. Key concerns remain over the nursing home sub-sector,

where the lower end of the elderly care home book saw an

increased rate of customers being placed on Watchlist and higher

defaults over 2011. Actions were taken to rebalance the portfolio

towards the stronger operators.