RBS 2011 Annual Report Download - page 374

Download and view the complete annual report

Please find page 374 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

364 -

365

365 -

366

366 -

367

367 -

368

368 -

369

369 -

370

370 -

371

371 -

372

372 -

373

373 -

374

374 -

375

375 -

376

376 -

377

377 -

378

378 -

379

379 -

380

380 -

381

381 -

382

382 -

383

383 -

384

384 -

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

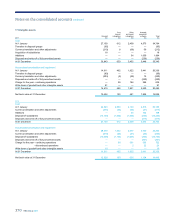

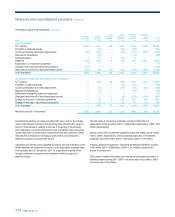

372 RBS Group 2011

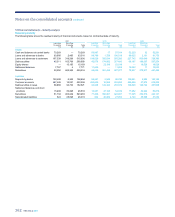

17 Intangible assets continued

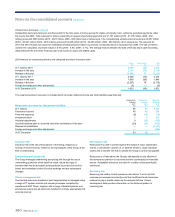

Impairment testing involves the comparison of the carrying value of a

CGU or group of CGUs with its recoverable amount. The recoverable

amount is the higher of the unit's fair value and its value in use. Value in

use is the present value of expected future cash flows from the CGU or

group of CGUs. Fair value is the amount obtainable from the sale of the

CGU in an arm's length transaction between knowledgeable, willing

parties.

Impairment testing inherently involves a number of judgmental areas: the

preparation of cash flow forecasts for periods that are beyond the normal

requirements of management reporting; the assessment of the discount

rate appropriate to the business; estimation of the fair value of CGUs;

and the valuation of the separable assets of each business whose

goodwill is being reviewed. Sensitivity to the more significant variables in

each assessment are presented below.

The recoverable amounts for all CGUs at 30 September 2011 were

based on the value in use test, using management's latest five-year

forecasts. The long-term growth rates have been based on respective

country GDP rates adjusted for inflation. The risk discount rates are

based on observable market long-term government bond yields and

average industry betas adjusted for an appropriate risk premium based

on independent analysis.

The recoverable amount of UK Retail, based on a 3% (2010 - 3%; 2009 -

4%) terminal growth rate and a 14.0% (2010 - 15.7%; 2009 - 14.6%) pre

tax discount rate, exceeded the carrying amount by £5.5 billion (2010 -

£6.9 billion; 2009 - £0.7 billion). A 1% change in the discount rate or

terminal growth rate would change the recoverable amount by

approximately £1.1 billion (2010 - £1.5 billion; 2009 - £0.9 billion) and

£0.6 billion (2010 - £0.9 billion; 2009 - £0.5 billion) respectively. In

addition, a 5% change in forecast pre tax earnings would change the

recoverable amount by approximately £0.8 billion (2010 - £0.9 billion;

2009 - £0.4 billion).

The recoverable amount of UK Corporate, based on a 3% (2010 - 3%;

2009 - 4%) terminal growth rate and a 14.1% (2010 - 15.6%; 2009 -

15.1%) pre tax discount rate, exceeded its carrying value by £2.1 billion

(2010 - £5.3 billion; 2009 - £6.1 billion). A 1% change in the discount rate

or terminal growth rate would change the recoverable amount by

approximately £1.1 billion (2010 - £1.6 billion; 2009 - £1.4 billion) and

£0.5 billion (2010 and 2009 - £0.9 billion) respectively. In addition, a 5%

change in forecast pre tax earnings would change the recoverable

amount by approximately £0.8 billion (2010 - £1.0 billion; 2009 - £0.8

billion).

The recoverable amount of Wealth, based on a 3% (2010 - 3%; 2009 -

4%) terminal growth rate and an 11.0% (2010 - 12.0%; 2009 - 15.3%) pre

tax discount rate, exceeded its carrying value by more than 100% and

was insensitive to a reasonably possible change in key assumptions.

The recoverable amount of Global Transaction Services, based on a 3%

(2010 and 2009 - 3%) terminal growth rate and an 11.4% (2010 - 12.8%;

2009 - 16.7%) pre tax discount rate, exceeded its carrying value by more

than 100% (2010 and 2009 - 100%) and was insensitive to a reasonably

possible change in key assumptions.

The recoverable amount of US Retail & Commercial, based on a 5%

(2010 and 2009 - 5%) terminal growth rate and a 14.4% (2010 - 14.9%;

2009 - 14.8%) pre tax discount rate, exceeded its carrying value by £0.2

billion (2010 - £1.6 billion; 2009 - £2.1 billion). A 1% change in the

discount rate or terminal growth rate would change the recoverable

amount by approximately £1.1 billion (2010 - £1.6 billion; 2009 - £1.0

billion) and £0.5 billion (2010 and 2009 - £0.8 billion) respectively. In

addition, a 5% change in forecast pre tax earnings would change the

recoverable amount by approximately £0.6 billion (2010 and 2009 - £0.7

billion).

The recoverable amount of RBS Insurance, based on a 3% (2010 and

2009 - 3%) terminal growth rate and a 12.3% (2010 - 13.1%; 2009 -

13.9%) pre tax discount rate, exceeded the carrying amount by £0.8

billion (2010 - £2.4 billion; 2009 - £3.0 billion). A 1% change in the

discount rate or terminal growth rate would change the recoverable

amount by approximately £0.5 billion and £0.2 billion respectively. In

addition, a 5% change in forecast pre tax earnings would change the

recoverable amount by approximately £0.3 billion.

Notes on the consolidated accounts continued