RBS 2011 Annual Report Download - page 157

Download and view the complete annual report

Please find page 157 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

RBS Group 2011 155

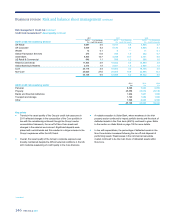

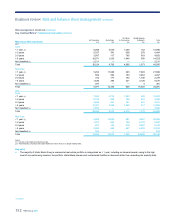

Residential mortgages which are three months or more in arrears (by volume) 2011

%

2010

%

2009

%

UK Retail (1) 1.6 1.7 1.6

Citizens 2.0 1.4 1.5

Note:

(1) The ‘One Account’ current account mortgage is excluded (£5.4 billion - 5.6% of assets) at 31 December 2011, 0.9% of these accounts were 90 days continually in excess of the limit (2010 - 0.8%).

Consistent with the way the Council of Mortgage Lenders publishes member arrears information, the 3+ months arrears rate now excludes accounts in repossession and cases with shortfalls post

property sale.

Key points

UK Retail

xThe UK Retail mortgage portfolio totalled £96.4 billion (98.6% in

Core) at 31 December 2011, an increase of 4.1% from 2010, due to

continued strong sales growth and lower redemption rates from

before the financial crisis.

xOf the total portfolio, 98.6% is designated as Core business,

primarily comprising mortgages branded the Royal Bank of Scotland,

NatWest, the One Account and First Active. Non-Core comprises

Direct Line Mortgages.

xThe assets are prime mortgages and include 7.2% (£6.9 billion) of

exposure to residential buy-to-let. There is a small legacy self-

certification book (0.3% of total assets). Self-certified mortgages

were withdrawn from sale in 2004.

xGross new mortgage lending in 2011 remained strong at £14.7

billion. The average LTV for new business during 2011 declined in

comparison to 2010 and the maximum LTV available to new

customers remained at 90%. Based on the Halifax House Price

index at September 2011, the book average indexed LTV improved

marginally when compared to December 2010, with the proportion of

balances with an LTV over 100% also lower. Refer to the table on

page 159, which details LTV information on a volume and value

basis.

xThe arrears rate (more than three payments in arrears, excluding

repossessions and shortfalls post property sale) has remained

broadly stable since late 2009 at 1.6%.

xThe number of properties repossessed in 2011 was 1,671, up from

1,392 in 2010.

xThe mortgage impairment charge was £187 million for 2011, an

increase of 2% from 2010. A significant part of the mortgage

impairment charge related to reduced expectations of cash recovery

on already defaulted debt. It also included an additional provision

charge for mortgage customers who received forbearance.

xDefault and arrears rates remain sensitive to economic

developments and are currently supported by the low interest rate

environment and strong book growth, with recent business yet to

fully mature.

Citizens

xCitizens’ residential mortgage portfolio totalled £23.8 billion at 31

December 2011, a reduction of 3% from 2010 (£24.6 billion).

xThe mortgage portfolio comprises £6.4 billion of residential

mortgages (99% in first lien position: Core - £5.8 billion; Non-Core -

£0.6 billion) and £17.4 billion of home equity loans and lines (41% in

first lien position: Core - £14.9 billion; Non-Core - £2.5 billion). Home

equity Core consists of 47% in first lien position.

xCitizens continues to focus on the ‘footprint’ states of New England,

Mid Atlantic and Mid West, targeting low risk products and

maintaining conservative risk policies. At 31 December 2011, the

portfolio consisted of £19.5 billion (82% of the total portfolio) within

footprint.

xLoan acceptance criteria were tightened during 2009 to address

deteriorating economic and market conditions.

xNon-Core comprises 13% of the residential mortgage portfolio. Its

largest component (74%) is the serviced by others (SBO) home

equity portfolio. The SBO portfolio consists of purchased pools of

home equity loans and lines, which resulted in an annualised

charge-off rate of 8.7% in 2011. It is characterised by out-of-footprint

geographies, high second lien concentration (95%) and high

average LTV (113% at 31 December 2011). The SBO book has

been closed to new purchases since the third quarter of 2007 and is

in run-off, with exposure down from £2.8 billion in 2010, to £2.3

billion at 31 December 2011. The arrears rate of the SBO portfolio

decreased from 3.0% in 2010, to 2.3% at 31 December 2011, as the

legacy of poorer assets receded, and account servicing and

collections became more effective following a servicer conversion in

2009.