RBS 2011 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

12 RBS Group 2011

Why have you made changes to your

wholesale businesses? Will you be

making further changes, including

selling businesses?

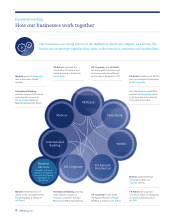

RBS wholesale businesses are a vital part of

the Group. They are important contributors in

their own right. They are linked with our other

banking businesses closely in a way that helps

us to serve all our customers better, makes us

more profitable as a whole and gives greater

stability and resilience to the Group.

Market conditions and regulatory changes,

including the Independent Commission on

Banking, adversely affected the outlook for

our wholesale business as it was structured.

As a result, we announced in January 2012

that we will exit from business areas that are

unprofitable and where we have weaker

customer positions. We are also scaling

back resources in areas where market

developments threaten our ability to fund

ourselves sustainably and profitably.

We are restructuring our pre-existing GBM and

GTS businesses. The result will be:

•a Markets business serving the clients of

all Group businesses;

•an International Banking unit which will

incorporate the existing GBM corporate

banking business with the international

elements of the existing GTS business; and

•the domestic corporate customers,

previously served by GTS, will be managed

by our domestic corporate banking

businesses in the UK, Ireland and the US.

What conditions are necessary

for you to return to profitability?

It remains the Group's ambition to get back to

being a safe, normal company. Our intention is

to do so as soon as practicable. Economic

headwinds currently point to a slower recovery

with interest rates low for longer than previously

expected. This, together with stringent

regulatory changes, means that it could take

longer to reach some of our strategic plan

targets than we had previously expected.

We remain confident of unlocking the

performance potential in our underlying

franchises and earning a return for our

shareholders above the cost of capital in

the medium-term.

When will I receive

a dividend?

RBS is subject to dividend restrictions

imposed by the European Commission that

prevent us from paying dividends on ordinary

shares, B shares and hybrid securities, unless

we have a legal obligation to pay. Once this

restriction has passed, the Board will be free

to declare dividends as it deems appropriate

and subject to normal market practice.

Further consideration should be given to the

Dividend Access Share held by the UK

Government. This commands a dividend on

the B shares it owns at the higher of 7%, or

2.5 times the ordinary dividend. This could

be a barrier to resuming ordinary dividends

in the near-term and could be subject to a

discussion with the Government at some time

in future.

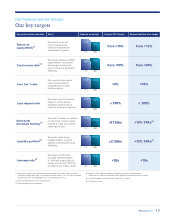

What is the trend in your

impairment charge?

The level of Group impairments, excluding

Greek sovereign debt impairment, fell by 20%

in 2011, reflecting our risk reduction efforts

and steady underlying improvements in the

economic environment. Clearly challenges

remain across the economies we serve. As a

consequence we remain cautious on future

improvements in impairment trends.

What is the trend

in your margins?

The net interest margin in our Retail &

Commercial businesses increased by seven

basis points in 2011. The expansion was

supported by a recovery in asset margins

across a number of our businesses.

Countering this, liability margins have

remained under pressure, reflecting the

increasing cost of wholesale funding and

strong competition for customer deposits.

What is your exposure to

European sovereign debt?

We have focused on actively managing down

our exposure to sovereign bonds of southern

peripheral European countries (Greece, Italy,

Portugal and Spain), which we had acquired

from ABN AMRO in 2007. In 2011, we reduced

our exposure by over 90%. Our outstanding

exposure is low at £0.3 billion, equivalent to

less than 0.1 percentage points of our Core

Tier 1 capital ratio. Reflecting our conservatism,

we have written down the value of our Greek

bond holdings by £1.1 billion, marking our

position to 21% of its original value.

We clearly have significant exposure to the

Republic of Ireland’s economy through Ulster

Bank where total lending was £48.5 billion at

31 December 2011. We remain committed to

our core Ulster Bank franchise but have placed

£14 billion of loans in our Non-Core division.

We are managing this portfolio down over time

and, where assets are currently non-

performing, they are being appropriately

provisioned.

When we speak to our investors, some questions are asked more often than others.

Below we provide a selection of those frequently asked questions and answers.

Q Q

Our business and our strategy

Q&As on progress

Q

Q

Q

Q