RBS 2011 Annual Report Download - page 327

Download and view the complete annual report

Please find page 327 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

317 -

318

318 -

319

319 -

320

320 -

321

321 -

322

322 -

323

323 -

324

324 -

325

325 -

326

326 -

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

334 -

335

335 -

336

336 -

337

337 -

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

RBS Group 2011 325

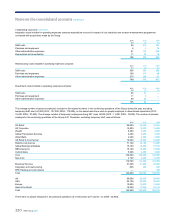

General insurance claims

The Group makes provision for the full cost of settling outstanding claims

arising from its general insurance business at the balance sheet date,

including claims estimated to have been incurred but not yet reported at

that date and claims handling expenses. General insurance claims

provisions amounted to £6,219 million at 31 December 2011 (2010 -

£6,726 million; 2009 - £5,802 million).

Provisions are determined by management based on experience of

claims settled and on statistical models which require certain

assumptions to be made regarding the incidence, timing and amount of

claims and any specific factors such as adverse weather conditions.

Management use the work of internal and external actuaries to assess

the level of gross and net outstanding claims provisions required to adopt

ameasurement basis of reserves which result in a provision in excess of

actuarial best estimates. In order to calculate the total provision required,

the historical development of claims is analysed using statistical

methodology to extrapolate, within acceptable probability parameters, the

value of outstanding claims at the balance sheet date. Also included in

the estimation of outstanding claims are other assumptions such as the

inflationary factor used for bodily injury claims which is based on

historical trends and, therefore, allows for some increase due to changes

in common law and statute; and the incidence of periodical payment

orders and the rate at which payments under them are discounted. Costs

for both direct and indirect claims handling expenses are also included.

Outward reinsurance recoveries are accounted for in the same

accounting period as the direct claims to which they relate. The

outstanding claims provision is based on information available to

management and the eventual outcome may vary from the original

assessment. Actual claims experience may differ from the historical

pattern on which the estimate is based and the cost of settling individual

claims may exceed that assumed.

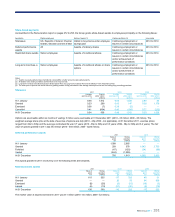

Deferred tax

The Group makes provision for deferred tax on temporary differences

where tax recognition occurs at a different time from accounting

recognition. Deferred tax assets of £3,878 million were recognised as at

31 December 2011 (2010 - £6,373 million; 2009 - £7,039 million).

The Group has recognised deferred tax assets in respect of losses,

principally in the UK, and temporary differences. Deferred tax assets are

recognised in respect of unused tax losses to the extent that it is probable

that there will be future taxable profits against which the losses can be

utilised. Business projections prepared for impairment reviews (see Note

17) indicate that sufficient future taxable income will be available against

which to offset these recognised deferred tax assets within six years

(2010 - eight years). The Group's cumulative losses are principally

attributable to the recent unparalleled market conditions. Deferred tax

assets of £3,246 million (2010 - £2,008 million; 2009 - £2,163 million)

have not been recognised in respect of tax losses carried forward in

jurisdictions where doubt exists over the availability of future taxable

profits.

Accounting developments

International Financial Reporting Standards

The IASB issued IFRS 9 ‘Financial Instruments’ in November 2009

simplifying the classification and measurement requirements in IAS 39 in

respect of financial assets. The standard reduces the measurement

categories for financial assets to two: fair value and amortised cost. A

financial asset is classified on the basis of the entity's business model for

managing the financial asset and the contractual cash flow characteristics

of the financial asset. Only assets with contractual terms that give rise to

cash flows on specified dates that are solely payments of principal and

interest on principal and which are held within a business model whose

objective is to hold assets in order to collect contractual cash flows are

classified as amortised cost. All other financial assets are measured at

fair value. Changes in the value of financial assets measured at fair value

are generally taken to profit or loss.

In October 2010, IFRS 9 was updated to include requirements in respect

of the classification and measurement of liabilities. These do not differ

markedly from those in IAS 39 except for the treatment of changes in the

fair value of financial liabilities that are designated as at fair value through

profit or loss attributable to own credit; these must be presented in other

comprehensive income.

In December 2010, the IASB issued amendments to IFRS 9 and to IFRS

7‘Financial Instruments: Disclosures’ delaying the effective date of IFRS

9 to annual periods beginning on or after 1 January 2015 and introducing

revised transitional arrangements including additional transition

disclosures. If an entity implements IFRS 9 in 2012 the amendments

permit it either to restate comparative periods or to provide the additional

disclosures. The additional transition disclosures must be given if

implementation takes place after 2012.

IFRS 9 makes major changes to the framework for the classification and

measurement of financial instruments and will have a significant effect on

the Group's financial statements. The Group is assessing the effect of

IFRS 9 which will depend on the outcome of the other phases of the

IASB's IAS 39 replacement project and on the outcome the IASB’s

tentative decision at its December 2011 meeting to reconsider the

following topics:

xadditional application guidance to clarify how the instrument

characteristics test was intended to be applied.

xbifurcation of financial assets, after considering any additional

guidance for the instrument characteristics test.

xexpanded use of other comprehensive income or a third business

model for some debt instruments.

‘Disclosures - Transfers of Financial Assets (Amendments to IFRS 7)’

was published by the IASB in October 2010. This replaces IFRS 7’s

existing derecognition disclosure requirements with disclosures about (a)

transferred assets that are not derecognised in their entirety and (b)

transferred assets that are derecognised in their entirety but where an

entity has continuing involvement in the transferred asset. The

amendments are effective for annual periods beginning on or after 1 July

2011.