RBS 2011 Annual Report Download - page 232

Download and view the complete annual report

Please find page 232 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

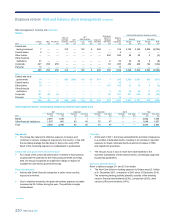

230 RBS Group 2011

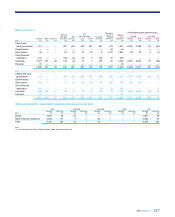

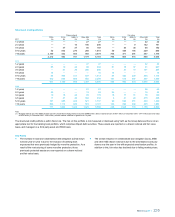

Risk management: Market risk continued

Quantitative risk appetite

The Executive Risk Forum (ERF) approves the quantitative market risk

appetite for trading and non-trading activities. The Global Head of Market

&Insurance Risk, under delegated authority from the ERF, sets and

populates a limit framework, which is cascaded down through legal entity,

division, business and desk level market risk limits.

At the Group level, the risk appetite is expressed in the form of a

combination of VaR, sensitivity and stress testing limits.

Adaily report summarises the Group’s market risk exposures against the

agreed limits. This daily report is sent to the Head of Restructuring &

Risk, Global Head of Market & Insurance Risk, business Chief Risk

Officers and appropriate business market risk managers.

Legal entities, divisions and lower levels in the business also have an

appropriate market risk framework of controls and limits in place to cover

all material market risk exposures.

The specific market risk metrics that are appropriate for controlling the

positions of a desk will be more granular than the Group level limits and

tailored to the particular business.

In line with the overall business strategy to reduce risk exposures, the

Group’s market risk limits were adjusted down during 2011.

The majority of the Group’s market risk exposure is in the GBM and Non-

Core divisions and Group Treasury. The Group is also exposed to market

risk through interest rate risk on its non-trading activities. There are

additional non-trading market risks in the retail and commercial

businesses of the Group, principally interest rate risk and foreign

exchange risk. These aspects are discussed in more detail in Balance

sheet management - Interest rate risk on pages 131 and 132 and

structural foreign currency exposures on page 133.

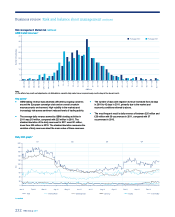

Risk models

VaR is a technique that produces estimates of the potential change in the

market value of a portfolio over a specified time horizon at a given

confidence level. For internal risk management purposes, the Group’s

VaR assumes a time horizon of one trading day and a confidence level of

99%. The Group's VaR model is based on a historical simulation model,

utilising data from the previous two years.

The VaR model has been approved by the FSA to calculate regulatory

capital for the trading book. The approval covers general market risk in

interest rate, foreign exchange, equity and specified commodity products

and specific risk in interest rate and equity products.

The VaR model is an important market risk measurement and control

tool. It is used for determining a significant component of the market risk

capital and, as such, it is regularly assessed. The main approach

employed is the technique known as back-testing, which counts the

number of days when a loss (as defined by the FSA) exceeds the

corresponding daily VaR estimate, measured at a 99% confidence level.

The FSA categorises a VaR model as green, amber or red. A green

model status is consistent with a good working model and is achieved for

models that have four or fewer back-testing exceptions in a 12-month

period. For the Group’s trading book, a green model status was

maintained throughout 2011.

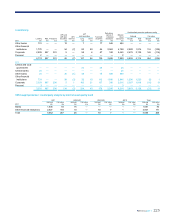

The Group’s VaR should be interpreted in light of the limitations of the

methodology used, as follows:

xHistorical simulation VaR may not provide the best estimate of future

market movements. It can only provide a prediction of the future

based on events that occurred in the two-year time series. Therefore,

events that are more severe than those in the historical data series

cannot be predicted.

xThe use of a 99% confidence level does not reflect the extent of

potential losses beyond that percentile.

xThe use of a one-day time horizon will not fully capture the profit and

loss implications of positions that cannot be liquidated or hedged

within one day.

xThe Group computes the VaR of trading portfolios at the close of

business. Positions may change substantially during the course of

the trading day and, if so, intra-day profit and losses will be incurred.

These limitations mean that the Group cannot guarantee that losses will

not exceed the VaR.

The RNIV framework has been developed to quantify those market risks

not adequately captured by the market standard VaR methodology.

Where risks are not included in the model, various non-VaR controls (for

example, portfolio size limits, sensitivity limits, triggers or stress limits) are

in place.

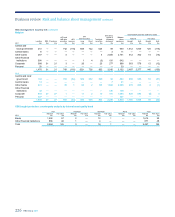

Risk models are developed both within business units and by Group

functions. Risk models are also subject to independent review and sign-

off to the same standard as pricing models. Meetings are held with the

FSA every quarter to discuss the traded market risk, including changes in

models, management, back-testing results, risks not included in the VaR

framework and other model performance statistics.

Anumber of VaR model and methodology enhancements were

introduced during 2011. The quality of the market data time series used

in the ABS mortgage trading business was improved, moving from

interpolated weekly data to daily observed time series. This change has

improved the accuracy of the correlation between the different time series

in the daily data. Additionally, the basis modelling between cash and

derivatives has been refined by introducing additional time series for the

sub-prime and subordinated residential bonds, reducing the over-reliance

on the commercial mortgage basis which was used as a conservative

proxy.

*unaudited

Business review Risk and balance sheet management continued