RBS 2011 Annual Report Download - page 141

Download and view the complete annual report

Please find page 141 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

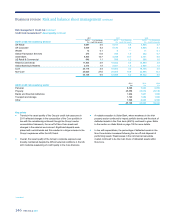

RBS Group 2011 139

Recoveries and active insolvency management

The ultimate outcome of a restructuring strategy is unknown at the time of

execution. It is highly dependent on the cooperation of the borrower and

the continued existence of a viable business. The following are generally

considered to be options of last resort:

xEnforcement of security or otherwise taking control of assets - where

the Group holds collateral or other security interest and is entitled to

enforce its rights, it may take ownership or control of the assets. The

Group’s preferred strategy is to consider other possible options prior

to exercising these rights.

xInsolvency - where there is no suitable restructuring option or the

business is no longer regarded as sustainable, insolvency will be

considered. Insolvency may be the only option that ensures that the

assets of the business are properly and efficiently distributed to

relevant creditors.

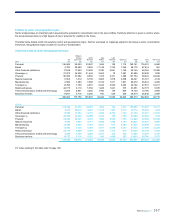

Retail customers

Early problem recognition and collections

There are collections functions in each of the retail businesses. Their role

is to provide support and assistance to customers who are experiencing

difficulties in meeting their financial obligations to the Group. Evidence of

such difficulties includes, for example, a missed payment on their loan, or

abalance that is in excess of the agreed credit limit. Additionally, in UK

Retail and Ulster Bank, a dedicated support team aims to identify and

help customers who may be facing financial difficulty but who are current

with their payments.

Within collections, a range of tools is deployed to initiate contact with the

customer, establish the cause of their financial difficulty and, where

possible, return the customer to a satisfactory position using, where

appropriate, forbearance strategies. If these strategies are unsuccessful,

the customer is transferred to the recoveries team.

Recoveries

The goal of the recoveries function is to collect the total amount

outstanding and reduce the loss to the Group by maximising the level of

cash recovery whilst treating customers fairly. A range of treatment

options are available within recoveries, including litigation procedures for

secured assets. In UK Retail and Ulster Bank, no repossession

procedures are initiated until at least six months following the emergence

of arrears. Additionally, certain forbearance options are made available to

customers within recoveries.

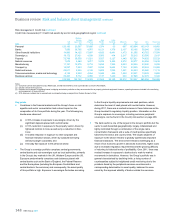

Forbearance

Within the Group’s retail businesses, forbearance generally occurs when

the business, for reasons relating to the actual or potential financial stress

of a borrower, grants a permanent or temporary concession to that

borrower. Forbearance is granted following an assessment of the

customer’s ability to pay. It is granted principally to customers with

mortgages. Granting of forbearance to unsecured customers is less

extensive.

Identification of forbearance

Mortgages are identified for forbearance treatment following initial contact

from the customer, in the event of payment arrears or when the customer

is transferred to collections or recoveries.

Types of retail forbearance

Anumber of forbearance options are utilised by the Group’s retail

businesses. These include, but are not limited to, reduced repayments,

payment holidays, capitalisations of arrears, term extensions and

conversions to interest only. Within UK Retail, interest only conversions

are generally made available only to those customers who are current on

payments and have a defined repayment source.

The principal types of forbearance granted in RBS Citizens’ mortgage

portfolio are the US government mandated HAMP (Home Affordable

Modification Program) and Citizens’ proprietary modification programme.

Both programmes typically feature a combination of term extensions,

capitalisations of arrears, temporary interest rate reductions and

conversions from interest only to amortising. These tend to be permanent

changes to contractual terms. Borrowers seeking a modification must

meet government specified qualifications for HAMP and internal

qualifications for Citizens’ modification programme. Both are designed to

evidence that the borrower is in financial difficulty as well as

demonstrating willingness to pay.

For those loans classified as non-performing, the Group’s objective in

granting forbearance is to minimise the loss on these accounts and

wherever possible, return the customer to the performing book. For those

loans that are performing, the aim is to enable the customers to continue

to service the loan.

The mortgage forbearance population is reviewed regularly to ensure that

customers are meeting the agreed terms of the arrangement. Key metrics

have been developed to record the proportion of customers who fail to

meet the agreed terms over time as well as the proportion of customers

who return to a performing state with no arrears.