RBS 2011 Annual Report Download - page 205

Download and view the complete annual report

Please find page 205 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

RBS Group 2011 203

xCollectively assessed provisions: provisions on impaired credits

below an agreed threshold are assessed on a portfolio basis to

reflect the homogeneous nature of the assets. The Group segments

impaired credits in its collectively assessed portfolios according to

asset type, such as credit cards, personal loans, mortgages and

smaller homogenous wholesale portfolios, such as business or

commercial banking. A further distinction is made between those

impaired assets in collections and those in recoveries (refer to

Problem debt management on page 139 for a discussion of the

collections and recoveries functions).

The provision is determined based on a quantitative review of the

relevant portfolio, taking account of the level of arrears, the value of

any security, historical and projected cash recovery trends over the

recovery period. The provision also incorporates any adjustments

that may be deemed appropriate given current economic and credit

conditions. Such adjustments may be determined based on: a

review of the current cash collections profile performance against

historical trends; updates to metric inputs - including model

recalibrations; and monitoring of operational processes used in

managing exposures - including the time taken to process non-

performing exposures.

xLatent loss provisions: a separate approach is taken for provisions

held against impairments in the performing portfolio that have been

incurred as a result of events occurring before the balance sheet

date but which have not been identified at the balance sheet date.

The Group’s methodologies to estimate latent loss provisions reflect:

-the probability that the performing customer will default;

-historical loss experience, adjusted, where appropriate, given

current economic and credit conditions; and

- the emergence period, defined as the period between an

impairment event occurring and a loan being identified and

reported as impaired.

Emergence periods are estimated at a portfolio level and reflect the

portfolio product characteristics such as the repayment terms and

the duration of the loss mitigation and recovery processes. They are

based on internal systems and processes within the particular

portfolio and are reviewed regularly.

As with collectively assessed impaired portfolios, the Group

segments its performing portfolio according to asset type.

Provisions and AFS reserves

The Group's consumer portfolios, which consist of high volume, small

value credits, have highly efficient largely automated processes for

identifying problem credits and very short timescales, typically three

months, before resolution or adoption of various recovery methods.

Corporate portfolios consist of higher value, lower volume credits, which

tend to be structured to meet individual customer requirements.

Provisions are assessed on a case by case basis by experienced

specialists with input from professional valuers and accountants. The

Group operates a transparent provisions governance framework, setting

thresholds to trigger enhanced oversight and challenge.

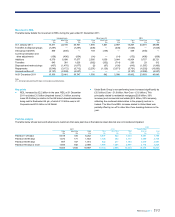

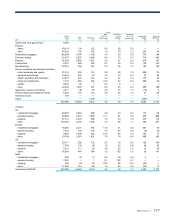

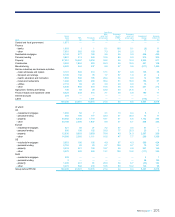

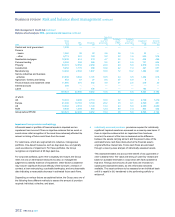

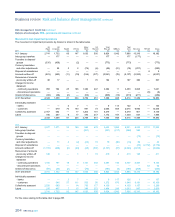

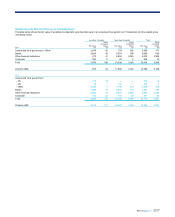

Analyses of provisions are set out on page 204 and 205.

Available-for-sale financial assets are initially recognised at fair value plus

directly related transaction costs and are subsequently measured at fair

value with changes in fair value reported in owners’ equity until disposal,

at which stage the cumulative gain or loss is recognised in profit or loss.

When there is objective evidence that an available-for-sale financial asset

is impaired, any decline in its fair value below original cost is removed

from equity and recognised in profit or loss.

The Group reviews its portfolios of available-for-sale financial assets for

evidence of impairment, which includes: default or delinquency in interest

or principal payments; significant financial difficulty of the issuer or

obligor; and it becoming probable that the issuer will enter bankruptcy or

other financial reorganisation. However, the disappearance of an active

market because an entity’s financial instruments are no longer publicly

traded is not evidence of impairment. Furthermore, a downgrade of an

entity’s credit rating is not, of itself, evidence of impairment, although it

may be evidence of impairment when considered with other available

information. A decline in the fair value of a financial asset below its cost

or amortised cost is not necessarily evidence of impairment. Determining

whether objective evidence of impairment exists requires the exercise of

management judgment. The unrecognised losses on the Group’s

available-for-sale debt securities are concentrated in its portfolios of

mortgage-backed securities. The losses reflect the widening of credit

spreads as a result of the reduced market liquidity in these securities and

the current uncertain macroeconomic outlook in the US and Europe. The

underlying securities remain unimpaired.

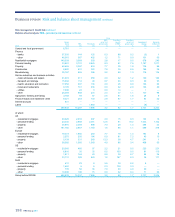

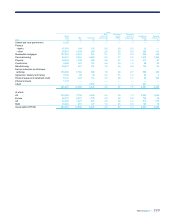

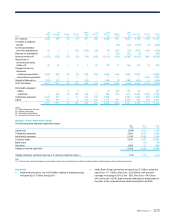

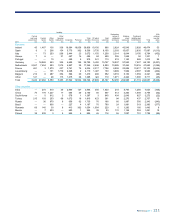

Analyses of AFS debt securities and related AFS reserves are set out on

page 206.