RBS 2011 Annual Report Download - page 138

Download and view the complete annual report

Please find page 138 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

136 RBS Group 2011

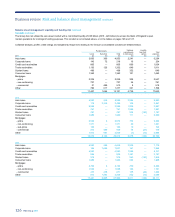

Risk management: Credit risk continued

Risk appetite continued

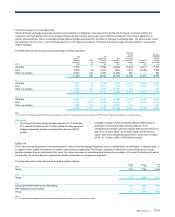

Since 2009, the Group has been managing its corporate exposures to

reduce concentrations and align its appetite for future business to the

Group’s broader strategies for its large corporate franchises. In the last

quarter of 2011, the Group announced further refinements to the single

name exposure management controls already in place, which brings

them more closely in line with market best practice and which allows the

Group to differentiate more consistently between the different risk types.

These changes are expected to be implemented during the first quarter of

2012. The Group is continually reviewing its single name concentration

framework to ensure that it remains appropriate for current economic

conditions and in line with improvements in the Group’s risk

measurement models.

Reducing the risk arising from concentrations to single names remains a

key focus of management attention. Continued progress was made in

2011 and credit exposures in excess of single name concentration limits

were reduced by over 15% during the year. The challenges posed by

continued market illiquidity and the impact of negative credit migration

caused by the current economic environment are expected to continue

throughout 2012.

Country

For information on how the Group manages credit risk by country, refer to

the Country risk section on page 208.

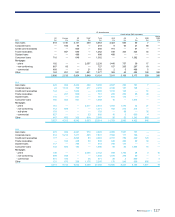

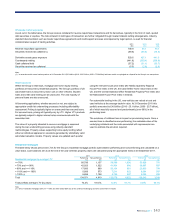

Controls and assurance*

Astrong independent assurance function is an important element of a

sound control environment. During 2011, the Group took the decision to

strengthen its credit quality assurance (CQA) activities and moved all

divisional CQA resources under the centralised management of Group

Credit Risk. The benefits of this action are already apparent in greater

consistency of standards and cross utilisation of resources. Reviews

planned for 2012 will benefit from the availability of subject matter experts

across all material products and classes and an improved ability to track

control breaches and strengthen processes.

Work began in the second half of 2011 on a major revision of the Group’s

key credit policies. This will ensure that the Group’s control environment

is appropriately aligned to the risk appetite that the Group Board has

approved and provide a sound basis for the Group’s independent audit

and assurance activities across the credit risk function. The work is

expected to be concluded by the end of the second quarter of 2012.

The Group Credit Risk function launched an assurance process to

provide the Group Chief Credit Officer with additional evidence of the

effectiveness of the controls in place across the Group to manage risk.

The results of these reviews will be provided to the Executive Risk Forum

and to the Board Risk Committee on a regular basis in support of the self-

certification that Group Credit Risk is obliged to complete under the

Group Policy Framework (refer to Operational risk on page 236 to 239).

*unaudited

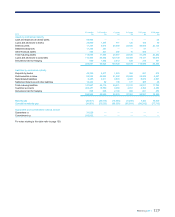

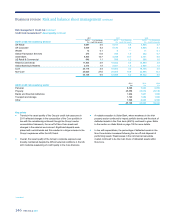

Problem debt management

The Group’s procedures for managing problem debts differ between

wholesale and retail customers, as discussed below.

Wholesale customers

The controls and processes for managing wholesale problem debts are

embedded within the divisions’ credit approval frameworks and form an

essential part of the ongoing credit assessment of customers. Any

necessary approvals will be required in accordance with the delegated

authority grid governing the extension of credit.

Early problem recognition

Each division has established Early Warning Indicators (EWIs) designed

to identify those performing exposures that require close attention due to

financial stress or heightened operational issues. Such identification may

also take place as part of the annual review cycle. EWIs vary from

division to division and comprise both internal parameters (e.g. account

level information) and external parameters (e.g. the share price of

publicly listed customers).

Customers identified through either the EWIs or annual review are

reviewed by portfolio management and/or credit officers within the

division, who determine whether or not the customer’s circumstances

warrant placing the exposure on the Watchlist process (detailed below).

Watchlist process*

There are three Watchlist ratings - amber, red and black - reflecting

progressively deteriorating conditions. Watchlist Amber loans are

performing loans where the counterparty or sector shows early signs of

potential stress or has other characteristics such that they warrant closer

monitoring. Watchlist Red loans are performing loans where indications

of the borrower’s declining creditworthiness are such that the exposure

requires active management, usually by the Global Restructuring Group

(GRG). Watchlist Black loans comprise risk elements in lending and

potential problem loans.

Once on the Watchlist process, customers come under heightened

scrutiny. The relationship strategy is reassessed by a forum of

experienced credit, portfolio management and remedial management

professionals within the division. In accordance with Group-wide policies,

anumber of mandatory actions will be taken, including a review of the

customer’s credit grade and facility security documentation. Other

appropriate corrective action is taken when circumstances emerge that

may affect the customer’s ability to service its debt. Such circumstances

include deteriorating trading performance, an imminent breach of

covenant, challenging macroeconomic conditions, a late payment or the

expectation of a missed payment.

For all Watchlist Red cases, the division is required to consult with the

GRG on whether the relationship should be transferred to the GRG (see

more on the GRG below). Relationships managed by the divisions tend to

be with companies operating in niche sectors such as airlines or products

such as securitisation special purpose vehicles. The divisions may also

manage those exposures when subject matter expertise is available in

the divisions rather than within the GRG.

Business review Risk and balance sheet management continued