RBS 2011 Annual Report Download - page 210

Download and view the complete annual report

Please find page 210 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

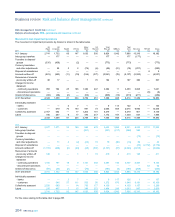

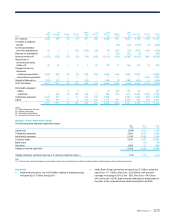

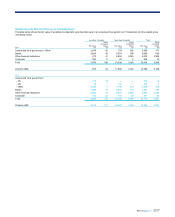

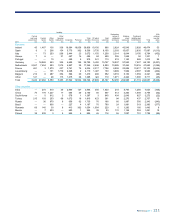

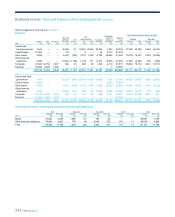

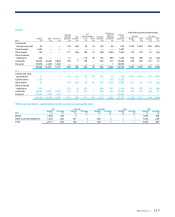

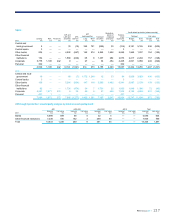

208 RBS Group 2011

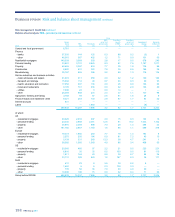

Risk management: Country risk

Introduction*

Country risk is the risk of material losses arising from significant country-

specific events such as sovereign events (default or restructuring);

economic events (contagion of sovereign default to other parts of the

economy, cyclical economic shock); political events (transfer or

convertibility restrictions and expropriation or nationalisation); and natural

disaster or conflict. Such events have the potential to affect elements of

the Group’s credit portfolio that are directly or indirectly linked to the

country in question and can also give rise to market, liquidity, operational

and franchise risk related losses.

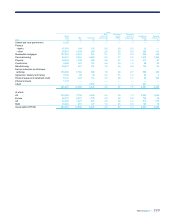

External risk environment*

2011 was another year of heightened country risks. However, trends

were divergent, with conditions deteriorating among vulnerable eurozone

countries facing growth impediments and higher public debt burdens,

while many emerging markets continued to enjoy relative stability, seeing

net inflows of capital for the full year and lower spreads despite some risk

aversion in the second half. In the US, notwithstanding a more

challenging political environment and a sovereign downgrade from a

rating agency, a deal was secured to increase the sovereign debt ceiling,

and yields on government debt remain low.

Eurozone risks

Europe was at the centre of rising global risks, owing to a combination of

slower growth among some of its major economies and a further

deepening of the ongoing sovereign crisis, which in turn harmed financial

sector health. Risks in Greece rose as a deeper than expected

contraction in GDP impacted the fiscal adjustment programme and hit

debt sustainability. Negotiations on a voluntary restructuring of public

debt held by the private sector commenced in the first half and a deal

was eventually reached in February 2012, with more punitive write-offs

for private investors than previously envisaged. This in turn led to an

agreement by eurozone leaders on a further borrowing programme for

the Greek government.

In May 2011, Portugal’s new government agreed a borrowing programme

with the European Union and International Monetary Fund (EU-IMF) after

a sharp deterioration in sovereign liquidity. Ireland's performance under

its EU-IMF programme was good and the announcement of a bank

restructuring deal without defaults on senior debt obligations helped

improve market confidence. This was reflected in a compression in bond

spreads in the second half of the year.

Despite the announcement of significant new support proposals by

eurozone leaders in July 2011, investor worries over risks to their

implementation rose and market conditions worsened markedly as a

result. Risk aversion towards Spanish and Italian assets picked up and

despite a policy response by both countries, yields remained elevated,

prompting the ECB to intervene to support their bonds in secondary

markets for the first time. Contagion affected bank stocks and asset

prices.

*unaudited

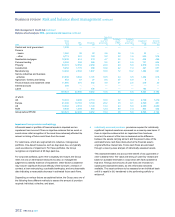

Eurozone leaders responded by stepping up anti-crisis efforts, focusing

largely on agreeing fiscal reform, bolstering bank capital and

strengthening capacity to offer financing support to sovereigns losing

market access. The ECB continued to buy sovereign debt in the

secondary market and increased liquidity support to banks with the

introduction of an emergency three-year long-term refinancing operation

in December. This helped ease interbank funding tensions somewhat and

may have contributed to some relief in sovereign debt markets late in the

year, as yields on new issuance by Spain and Italy dropped.

Emerging markets

Emerging markets continued to perform relatively well. In Asia, despite

slowing growth, China and India continued to post strong overall

expansion, while generally large external savings levels reinforced

balance of payments stability. In China specifically, measures to curb

house price growth began to have a more noticeable impact, with real

estate prices falling in many cities. Efforts are underway to address some

bank asset quality concerns linked to rapid lending growth in 2009.

In emerging Europe, Russia experienced some contagion into asset

markets from weaker commodity prospects and a challenging investment

climate, but the sovereign balance sheet remained quite robust. Foreign

exchange debts remained a risk factor in a number of Eastern European

economies. Elsewhere, Turkey’s economy cooled in the second half of

2011, helping to narrow the current account deficit sharply, though

external vulnerabilities persisted.

The Middle East and North Africa witnessed political instability in a

number of the relatively lower-income countries. The path of any

transition has yet to become fully clear in most cases. Excluding Bahrain,

pressures for change were more contained in the Gulf Co-Operation

Council countries.

Latin America remained characterised by relative stability owing to

balance sheet repair by a number of countries following crises in previous

decades. Capital inflows contributed to currency appreciation, but

overheating pressures have so far proven contained, including in Brazil

where credit growth slowed from high levels.

Outlook

Overall, the outlook for 2012 remains challenging with risks likely to

remain elevated but divergent. Much will depend on the success of EU

efforts to contain contagion from the sovereign crisis (where downside

risks are high) and whether growth headwinds in larger advanced

economies persist. Emerging market balance sheet risks remain lower,

despite ongoing structural and political constraints, but these economies

will continue to be affected by events elsewhere through financial

markets and trade channels.

Business review Risk and balance sheet management continued