RBS 2011 Annual Report Download - page 137

Download and view the complete annual report

Please find page 137 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

RBS Group 2011 135

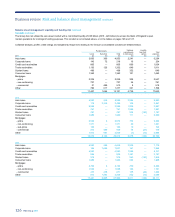

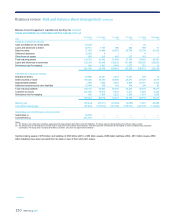

Product/asset class concentration framework

xRetail - a formal framework establishes Group-level statements and

thresholds that are cascaded through all retail franchises in the

Group and to granular business lines. These include measures that

relate both to aggregate portfolios and to asset quality at origination,

which are tracked frequently to ensure consistency with Group

standards and appetite. This appetite setting and tracking then

informs the processes and parameters employed in origination

activities, which require a large volume of small-scale credit

decisions, particularly those involving an application for a new

product or a change in facilities on an existing product. The majority

of these decisions are based upon automated strategies utilising

credit and behaviour scoring techniques. Scores and strategies are

typically segmented by product, brand and other significant drivers

of credit risk. These data driven strategies utilise a wide range of

credit information relating to a customer including, where

appropriate, information across customer holdings. A small number

of credit decisions are subject to additional manual underwriting by

authorised approvers in specialist units. These include higher-value,

more complex, small business and personal unsecured transactions

and some residential mortgage applications.

xWholesale - formal policies, specialised tools and expertise, tailored

monitoring and reporting and, in certain cases, specific limits and

thresholds are deployed to address certain lines of business across

the Group, where the nature of credit risk incurred could represent a

concentration or a specific/heightened risk in some other form. For

example, in response to volatile conditions in the syndicated loan,

fixed income and equities markets during 2011, the Group engaged

in only selective underwriting activity in these markets. In addition to

the limit structures the Group has in place to manage its overall

exposure to underwriting activity, market-linked controls were

introduced in the loan underwriting book in 2011, to align the risk

profile more closely to asset price movements. Those portfolios

identified as potentially representing a concentration or heightened

risk are subject to formal governance, including periodic review, at

either Group or divisional level, depending on materiality.

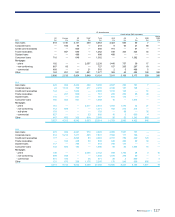

Sector concentration framework

Across wholesale portfolios, exposures are assigned to, and reviewed in

the context of, a defined set of industry sectors. Through this sector

framework, appetite and portfolio strategies are agreed and set at

aggregate and more granular levels where exposures have the potential

to represent excessive concentration or where trends in both external

factors and internal portfolio performance give cause for concern. Formal

periodic reviews are undertaken at Group or divisional level depending on

materiality. These may include an assessment of the Group’s franchise in

aparticular sector, an analysis of the outlook (including downside

outcomes), identification of key vulnerabilities and stress/scenario tests.

Specific reporting on trends in sector risk and on status versus agreed

appetite and portfolio strategies is provided to senior management and to

the Group Board.

As a result of the reviews carried out in 2011, the Group has reduced its

risk appetite in the higher-risk sectors of leisure, media, commercial real

estate, construction, automotive, and airlines and aerospace.

In response to the severe budgetary cuts mandated by the UK

Government in 2010, the UK and Northern Ireland teams conducted a full

review of the likely impact of the austerity measures on their corporate

and retail lending portfolios. Areas of specific focus, such as local

authority lending, where budgetary pressures will be hard felt, and

portfolios exposed to discretionary consumer spend, such as the retail

and leisure industries, were stressed using downside assumptions on

further house price deterioration and higher unemployment. The output of

these activities was reviewed by the Executive Risk Forum and actions

agreed in the event that these scenarios threaten to materialise.

The impact of the eurozone crisis has been felt most significantly in the

financial institutions sector, where widening credit spreads and regulatory

demand for increases in Tier 1 capital have exacerbated the risk

management challenges already posed by the sector’s continued

weakness, as provisions and write-downs remain elevated. A material

percentage of global banking activity in risk mitigation now passes

through the balance sheets of the top global players, increasing the

systemic risks to the sector. The Group’s exposures to these banks

continue to be closely managed. The increased use of central clearing

houses to reduce counterparty credit risk, including settlement risk,

among the larger banks is a welcome move but one that will bring its own

challenges. The weaker banks in the eurozone have also been the

subject of heightened scrutiny and the Group’s risk appetite for these

banks was adjusted continuously throughout 2011.

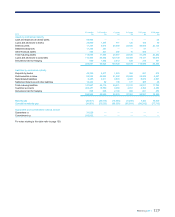

Single name concentration framework*

Within wholesale portfolios, much of the activity undertaken by the credit

risk function is organised around the assessment, approval and

management of the credit risk associated with a borrower or group of

related borrowers.

Aformal single name concentration framework addresses the risk of

outsized exposure to a borrower or borrower group. The framework

includes specific and elevated approval requirements, additional reporting

and monitoring, and the requirement to develop plans to address and

reduce excess exposures over an appropriate timeframe.

Credit approval authority is discharged by way of a framework of

individual delegated authorities, which requires at least two individuals to

approve each credit decision, one from the business and one from the

credit risk management function. Both parties must hold sufficient

delegated authority under the Group-wide authority grid. Whilst both

parties are accountable for the quality of each decision taken, the credit

risk management approver holds ultimate sanctioning authority. The level

of authority granted to individuals is dependent on their experience and

expertise, with only a small number of senior executives holding the

highest authority provided under the framework. Daily monitoring of

individual counterparty limits is undertaken.

At a minimum, credit relationships are reviewed and re-approved

annually. The renewal process addresses: borrower performance,

including reconfirmation or adjustment of risk parameter estimates; the

adequacy of security; and compliance with terms and conditions. For

certain counterparties, early warning indicators are also in place to detect

deteriorating trends in limit utilisation or account performance, and to

prompt additional oversight.