RBS 2011 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

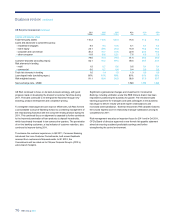

RBS Group 2011 67

2011 2010 2009

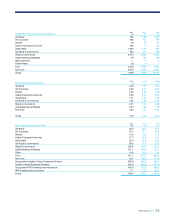

£bn £bn £bn

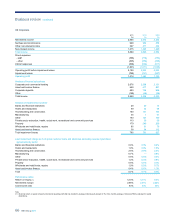

Capital and balance sheet

Total third party assets 111.8 114.6 114.9

Loans and advances to customers (gross) (1)

-banks and financial institutions 5.7 6.1 6.3

- hotels and restaurants 6.1 6.8 6.7

- housebuilding and construction 3.9 4.5 4.3

- manufacturing 4.6 5.3 5.9

- other 32.6 31.0 29.9

- private sector education, health, social work, recreational and community services 8.7 9.0 6.5

- property 28.2 29.5 33.0

- wholesale and retail trade, repairs 8.5 9.6 10.2

- asset and invoice finance 10.4 9.9 8.8

108.7 111.7 111.6

Customer deposits (1) 100.9 100.0 87.8

Risk elements in lending (1) 5.0 4.0 2.3

Loan:deposit ratio (excluding repos) 106% 110% 126%

Risk-weighted assets 76.1 81.4 90.2

Note:

(1) Includes disposal groups: loans and advances to customers - £12.2 billion; customer deposits - £21.8 billion; risk elements in lending - £1.0 billion.

In 2011, UK Corporate focused on supporting its customers through

challenging economic times. As a result of over 5,000 hours of customer

research, UK Corporate launched the ‘Ahead for Business’ promise to its

small and medium-sized enterprise (SME) customers.

To deliver on this, the division launched a number of initiatives to improve

the service it offers to customers. For example, the ‘Working with You’

initiative, has seen over 4,600 visits to customer businesses since its

launch in Q2 2011. Additionally, following the launch of the relationship

manager accreditation programme, also in Q2 2011, almost all

relationship managers have gained full accreditation in the initial phase.

UK Corporate continued to support new and existing businesses during

2011:

xlaunching its best ever fixed rate loan product for SMEs;

xreacting quickly after the August riots to give affected businesses

access to special interest rate and fee free lending products;

xanswering over 4,000 calls on the Start-up Hotline, offering free

advice and a complementary business plan review service; and

xsupporting more debt capital and loan market deals for larger

corporates than any other bank.

The division also took measures to reduce the risk retained in the

business allowing for quicker and more consistent decisions by

simplifying the credit underwriting process and improving automated

decision making.

2011 compared with 2010

Operating profit decreased 3% to £1,414 million, as lower income and

higher impairments were only partially offset by a decrease in expenses.

Net interest income remained broadly flat. Net interest margin improved

7basis points with benefits from re-pricing the lending portfolio and the

revision to income deferral assumptions in Q1 2011 partially offset by

increased funding costs together with continued pressure on deposit

margins. A 1% increase in deposit balances supported an improvement

in the loan:deposit ratio to 106%.

Non-interest income decreased by 4% as a result of lower GBM cross-

sales and fee income, partially offset by increased Invoice Finance and

Lombard income.

Excluding the £29 million OFT penalty in 2010, total costs increased by

1%, largely reflecting increased investment in the business and higher

costs of managing the non-performing book.

Impairments of £785 million were 3% higher due to increased specific

impairments and collectively assessed provisions, partially offset by lower

latent loss provisions.

2010 compared with 2009

Operating profit grew by £338 million, 30%, compared with 2009, driven

by strong income growth and significantly lower impairments, partially

offset by higher costs.

UK Corporate performed strongly in the deposit market, with customer

deposit balance growth of £12 billion contributing to a 16 percentage

point improvement in the loan:deposit ratio in 2010. While customer

lending increased only marginally (with gross lending largely offset by

customer deleveraging) net interest income rose by £280 million, 12%,

and net interest margin rose by 29 basis points driven primarily by the

good progress made on loan repricing.

Non-interest income increased 3% reflecting strong refinancing levels

and increased operating lease activity, partially offset by lower sales of

financial market products.

Total costs increased 9% (£141 million) or 5% excluding the OFT penalty

in 2010, legal recovery in 2009 and the normalisation of staff

compensation phasing.

Impairments were 18% lower, primarily as a result of higher charges

taken during the first half of 2009 to reflect potential losses in the portfolio

not yet specifically identified.

Return on equity increased from 9.4% to 12.1%, reflecting higher

operating profit and lower RWAs as a result of improved risk metrics.