RBS 2011 Annual Report Download - page 145

Download and view the complete annual report

Please find page 145 of the 2011 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

|

|

RBS Group 2011 143

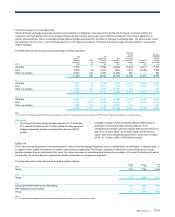

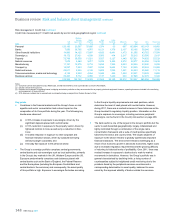

Wholesale market exposures

As set out in the table below, the Group receives collateral for reverse repurchase transactions and for derivatives, typically in the form of cash, quoted

debt securities or equities. The risks inherent in both types of transaction are further mitigated through master bilateral netting arrangements. Industry

standard documentation such as master repurchase agreements and credit support annexes accompanied by legal opinion, is used for financial

collateral taken as part of trading activities.

2011 2010 2009

£bn £bn £bn

Reverse repurchase agreements 100.9 95.1 76.1

Securities received as collateral (1) (98.9) (94.3) (74.0)

Derivative assets gross exposure 529.6 427.1 441.5

Counterparty netting (441.6) (330.4) (358.9)

Cash collateral held (37.2) (31.1) (33.7)

Securities received as collateral (5.3) (2.9) (3.6)

Note:

(1) In accordance with normal market practice, at 31 December 2011 £95.4 billion (2010 - £93.5 billion; 2009 - £73.0 billion) had been resold or re-pledged as collateral for the Group’s own transactions.

Retail exposures

Within the Group’s retail book, mortgage and home equity lending

portfolios are secured by residential property. The Group’s portfolio of US

automobile loans is secured by motor cars or other vehicles. Student

loans and credit card lending are all unsecured. The vast majority of

personal loans are also unsecured.

All borrowing applications, whether secured or not, are subject to

appropriate credit risk underwriting processes including affordability

assessment. Pricing is typically higher on unsecured than secured loans.

For secured loans, pricing will typically vary by LTV. Higher LTV products

are typically subject to higher interest rates commensurate with the

associated risk.

The value of a property intended to secure a mortgage is assessed

during the loan underwriting process using industry-standard

methodologies. Property values supporting home equity lending reflect

either an individual appraisal or valuations generated by statistically valid

automated valuation models. Property values are updated each quarter

using the relevant house price index (the Halifax Quarterly Regional

House Price Index in the UK, the Case-Shiller Home Value Index in the

US, and the Central Statistics Office Residential Property Price Index and

the Nationwide House Price Index in Ireland).

For automobile lending in the US, new vehicles are valued at cost and

used vehicles at the average trade-in value. At 31 December 2011 this

portfolio amounted to £4.8 billion (2010 - £5.1 billion; 2009 - £5.7 billion),

all of which was fully secured and predominantly (over 99%) in the

performing book.

The existence of collateral has an impact on provisioning levels. Once a

secured loan is classified as non-performing, the realisable value of the

underlying collateral and the costs associated with repossession are

used to estimate the provision required.

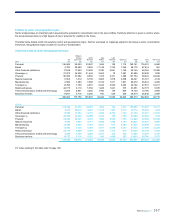

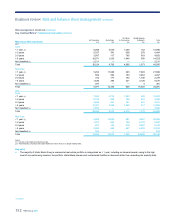

Residential mortgages

The table belowshows period end LTVs for the Group’s residential mortgage portfolio split between performing and non-performing and calculated on a

value basis. Loan balances are as at the end of the year whereas property values are calculated using the appropriate index at 30 September 2011.

2011 2010 2009

Residential mortgages by average LTV Performing

£m

Non-performing

£m

Performing

£m

Non-performing

£m

Performing

£m

Non-performing

£m

<= 70% 60,799 1,137 59,598 1,036 55,920 791

>70% and <= 90% 42,923 1,022 41,964 906 38,807 697

>90% and <= 110% 17,856 990 20,104 951 23,853 754

>110% and <= 130% 5,809 573 7,211 622 8,604 507

> 130% (1) 6,684 1,188 3,793 507 3,059 269

Total 134,071 4,910 132,670 4,022 130,243 3,018

Total portfolio average LTV (by value) 73.2% 101.4% 72.4% 91.7% 73.5% 90.1%

Note:

(1) 83% of residential mortgages with LTV > 130% are within Ulster Bank due to the continued challenging economic environment in Ireland.